TYL - Roper Technologies Makes A Shrewd Purchase With Frontline Education

Summary

- Roper's M&A strategy has entered a new phase as the company announced a big purchase on Tuesday.

- This deal, particularly in light of last year's TransCore sale, should have a great result for shareholders.

- I remain bullish on Roper and see the share price heading to $570 over the next two years.

On Tuesday, Roper Technologies ( ROP ) announced that it will be acquiring education software company Frontline Education for $3.73 billion, or $3.38 billion after tax benefits. This will be the second-largest acquisition in Roper's history to-date and marks a new chapter in the company's growth strategy.

I've owned Roper stock for the past few years, highlighting it as an underappreciated Dividend Aristocrat with a strong M&A strategy. In many ways, it's the lower valuation version of Canada's exceptionally successful tech roll-up, Constellation Software ( OTCPK:CNSWF ).

In a previous article, I noted how Constellation decided that it would start going after larger acquisitions to keep its own growth strategy going. That, in turn, seemed like it might pose a competitive challenge to Roper, which has historically pursued larger software acquisitions than Constellation. Roper, for its own part, appears to be going into the even bigger deal space, as it has now made several billion-dollar or greater acquisitions instead of sticking to the $100mn-$1bn space it used to be known for.

With this context established, let's take a look at what this Frontline purchase means for Roper going forward.

What Is Roper Buying With Frontline?

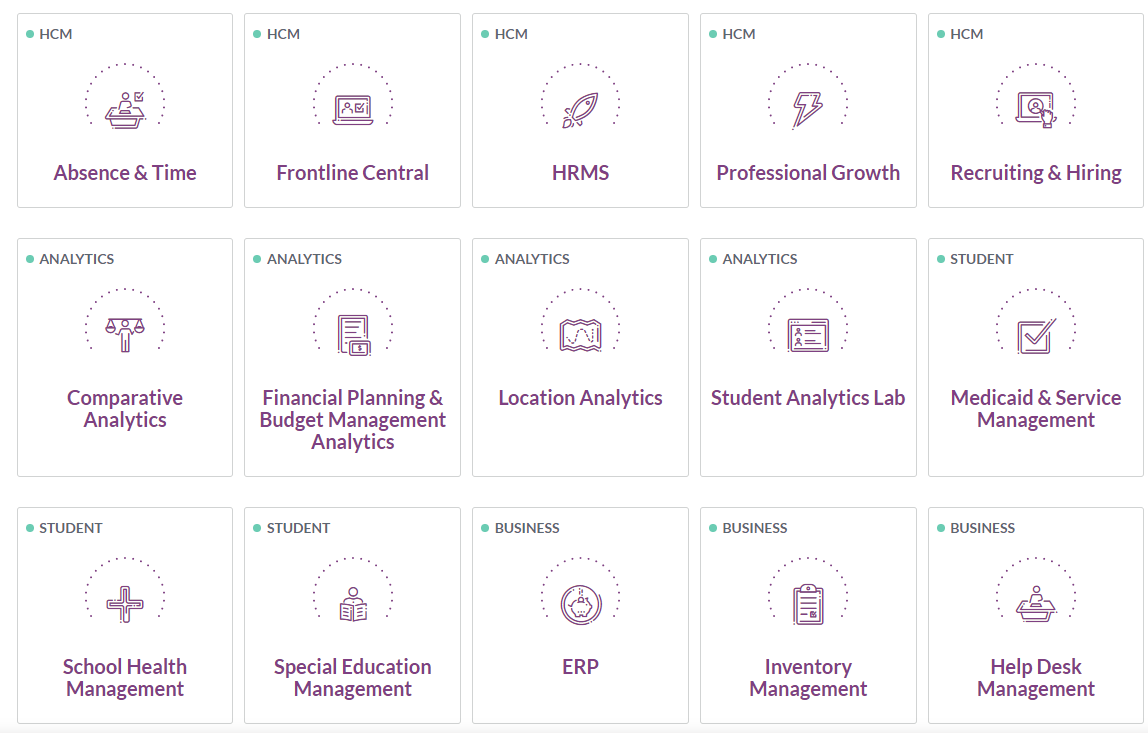

Frontline Education is a software platform designed for educational systems to manage various aspects of their workflows. From my understanding, Frontline was built on managing school attendance, time scheduling, and student analytics. Over the years, the company's focus has broadened, and it has made various acquisitions to get into more areas of school management:

{kind=link}

As you can see, Frontline now offers solutions for a variety of things including budgeting, hiring, health care services, and inventory management in addition to absence tracking.

Why is this attractive to Roper? Its business model over the years has transformed from owning various industrial companies to owning software companies which service primarily industrial and other non-tech clients. Roper has software for fields such as insurance, power plants, food service, supply chains and more. Often, software companies built for these sorts of niches are available at lower multiples than you'd see for SaaS businesses selling to more glamorous fields.

Against this backdrop, you can see how an education management platform would fit with Roper's broader collection of assets.

Here's Roper's CEO offering his justification for the purchase:

“Frontline is a terrific business with clear niche market leadership, a proven track record of strong organic and inorganic growth, excellent cash conversion, and an outstanding management team that will thrive as part of Roper,” said Neil Hunn, Roper’s President and CEO. “The acquisition of Frontline demonstrates Roper’s disciplined capital deployment strategy that focuses on identifying high-quality, market-leading technology businesses that will enhance Roper’s cash flow compounding. We are excited to welcome Frontline to the Roper family.”

Asset Recycling Is Paying Off

Last year, Roper sold one of its traditionally important assets, transportation business TransCore , for $2.68 billion in cash. I highlighted this as a big win for Roper at the time. You see, TransCore had significantly lower margins than Roper's newer software operations. And yet, Roper was able to sell off TransCore at the same EBITDA multiple that ROP stock was trading at in 2021.

This means that Roper was able to improve the quality of its business, on a profit margin basis, without giving up too much from a near-term profitability or cash flow generation standpoint.

It gets even better. That TransCore sale went off at 20x EBITDA for a business generating 24% EBITDA margins. Roper then got to use that $2.68 billion of cash for new purchases, which will largely be deployed into this Frontline deal.

By contrast, Roper is paying just 19x EBITDA for Frontline while getting nearly 50% EBITDA margins off its new business. Arguably, Frontline has better organic growth prospects than TransCore did as well. This is a home run for Roper. Sell a business with 24% margins to buy one at high 40s margins and a slightly lower valuation multiple. You can see the essence of Roper's whole M&A strategy and superior capital allocation in these two deals.

How This Affects Roper's Overall Valuation & Outlook

Education is a particularly valuable software vertical since it gets its funding from local governments and is a slow-to-change industry. Once a school system picks Frontline and trains its teachers on it, the motivation to switch software providers is likely to be limited.

Another tech software roll-up, Tyler Technologies ( TYL ), has made its bread and butter selling software to governments for applications such as courtroom management. Tyler has historically traded at a massive premium to Roper:

Acquisitions such as Frontline should help Roper close the gap with Tyler to some extent. Now, you could argue the difference will mostly be made up via Tyler's share price continuing to decline. I sold TYL stock back in 2020 saying its valuation had reached an untenable level. Regardless of how great the business model is, it's generally hard to make above average returns buying a stock above 50x EBITDA.

So, I'm not saying Roper necessarily needs to trade up to Tyler's historical valuation range. However, in a world where investors have often felt Tyler was worth at least 40x EBITDA, I suspect Roper's 22x multiple is a bit too cheap by comparison.

Turning from relative to absolute valuation, Roper is currently selling at just under 30x this year's projected earnings:

ROP earnings estimates (Seeking Alpha)

Historically, it's been generally advantageous to purchase Roper under 30 times earnings, whereas prices over that number have often marked relative peaks in the company's short-term share performance. So, today's valuation is right around the median level.

Roper is slightly cheaper than first glance, however. The big factor there is that most analysts covering the company do not model in any future acquisitions by Roper until they actually occur.

This is more important than it may first sound. After all, Roper's primary growth driver -- the thing that makes the business model hum -- is that it regularly makes new purchases to expand the company. Yet, analysts typically model the company as though there won't be any future acquisitions. That is understandable from the perspective that analysts want to be conservative. However, when Roper makes deals year in and year out, it makes sense to expect some upside from future dealmaking.

For example, this new Frontline deal will add $370 million of annual sales from day one, with incremental growth on top of that. Now, instead of $5.5 billion for Roper's FY '23 revenues, we're at $5.9 billion, which pushes the growth rate well into the double-digits next year. As Roper can traditionally grow earnings faster than revenues, things should look even better from an EPS perspective.

Analysts were projecting Roper at 25x 2024 earnings. But that assumption didn't have future dealmaking in it. Once you add in Frontline and other deals which will happen between now and then, there's a good chance Roper's real earnings are closer to $18 or $19 per share instead of the $16.53 analyst consensus.

A Roper with $19 per share of earnings and a double-digit top-line and bottom-line growth rate is probably worth 30x earnings, in line with its normal historical multiple. That gets us to a two-year price target of $570 against today's $405 price. Roper isn't the sort of stock that tends to move up dramatically at any given time, but it can reliably produce market-beating returns due to its steady and predictable execution of its core M&A strategy.

Finally, I would note that Roper is a Dividend Aristocrat and continues to offer dramatic dividend growth. It has hiked its dividend at an excellent 17%/year annualized rate over the past decade, taking the annual dividend from 56 cents to $2.48 per share since 2012. Critics will note that the dividend yield is only 0.6% today. However, at a 17% annualized growth rate, the future yield-on-cost builds up rather quickly. Also, the current dividend yield is above Roper's historical median, suggesting there is relative value at today's price.

For further details see:

Roper Technologies Makes A Shrewd Purchase With Frontline Education