ROP - Roper Technologies: Moving To Neutral Post The Recent Run-Up

2023-07-24 00:43:35 ET

Summary

- Roper Technologies is seeing strong demand in its end markets, supported by trends in AI and Generative AI, which should boost revenue growth.

- The company's Q2 FY2023 earnings exceeded expectations, with a 16.8% YoY increase in revenue and a 20% YoY growth in adjusted EPS.

- Despite positive growth prospects, ROP stock is currently trading at a premium, leading to a neutral due to the lack of a margin of safety.

Investment Thesis

Roper Technologies (ROP) is experiencing good demand in its end markets supported by secular trends from Artificial Intelligence [AI] and Generative AI. This should help the company's revenue growth moving forward. In addition, an improving business mix from good strength in recurring revenue base and ROP's bolt-on M&A strategy to acquire market-leading, high recurring revenue-based businesses in niche markets should also aid the top line in the near term as well as the longer term.

On the margin front, the company should benefit from operating leverage, easing supply chain challenges, improving business mix through the acquisition of high-margin businesses, and increasing productivity through automation and digitalization.

I previously covered Roper in May and the stock has seen ~9% in price since then. While I continue to like the business fundamentals, I can't say so regarding its stock price. The stock is currently trading at a premium to its historical levels based on FY23e EPS and, even on its FY24e EPS, it is trading almost in line with the historical levels, providing little margin of safety. I believe the company's growth prospects are already reflected in the stock, so, I am moving to the sideline and rating ROP neutral.

Q2 FY2023 Earnings

Recently, Roper Technologies Inc. reported better-than-expected results for the second quarter of 2023. The company's revenue increased by 16.8% YoY on a reported basis and 9% YoY organically to $1.53 billion, which exceeded the consensus estimate of $1.5 billion. Adjusted EPS grew by 20% YoY to $4.12 and was higher than the consensus EPS estimate of $3.99. The adjusted EBITDA margin increased 100 basis points (bps) YoY to 40.3%. The revenue growth was driven by good end-market demand and an increase in recurring revenue and good acquisition synergies. The adjusted EBITDA margin and adjusted EPS increased as a result of sales leverage and a high-margin business portfolio mix.

Revenue Analysis And Outlook

In my previous article , I wrote about the company's long-term growth prospects benefiting from its bolt-on M&A strategy, strong demand, and improved business portfolio. The company reported its earnings for the second quarter of 2023 last week and similar dynamics were seen there as well.

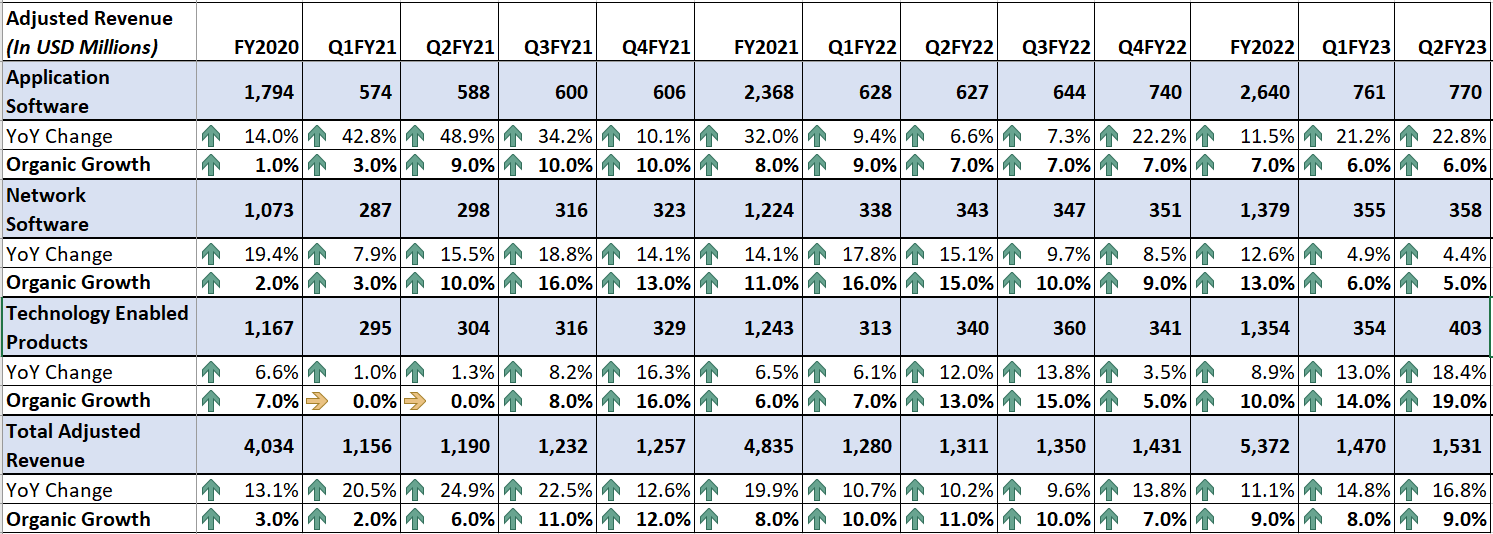

In the second quarter of 2023, ROP continued to benefit from its acquisition of Frontline Education (acquired in fiscal 2022) and other small tuck-ins. The company's revenue growth also benefited from good growth of recurring revenue and a high customer retention rate in its businesses due to continued healthy demand momentum in all of its end markets. This resulted in a 16.8% YoY growth in revenue to $1.53 billion, reflecting a benefit of 8 percentage points from acquisitions. Excluding the growth contribution from the acquisitions, the organic growth increased by 9% YoY. Organic growth was led by 8% YoY growth in software recurring revenue across the enterprise and outsized growth of 19% in the tech-enabled products segment.

ROP's Historical Revenue (Company Data, GS Analytics Research)

{kind=link}

Looking ahead, I believe Roper's revenue growth journey should keep benefiting from strong end-market demand driven by secular trends from Artificial Intelligence [AI] and generative AI, the non-cyclical nature of its portfolio, and strength in recurring revenue base, and strategic M&As.

Roper's software and products are in high demand because businesses across different industries are rapidly adopting digital processes. Many daily tasks are now automated, and artificial intelligence [AI] is becoming an increasing necessity. Such enhancements are vital for mitigating uncertainties in the broader operating environment and ensuring sustained profitability for industries. Roper's software solutions is benefiting from this growing trend.

While the adoption of AI is supporting the company's end markets, the company is also seeing emerging opportunities in the generative AI space. Generative AI enables businesses to enhance speed and creativity in various areas. This advancement is paving the way for a whole new level of efficiency in both back-end and front-end operations, leading to substantial increases in productivity. An increasing number of generative AI software and tools like ChatGPT and others are flowing into the software markets in order to increase efficiencies driven by automation and digitization, making the lives of individuals easy. According to a research article published at Bloomberg , the generative AI market is anticipated to grow at a CAGR of 42% over the next 10 years, giving a good long-term secular tailwind.

As I mentioned in my previous article , Roper's software tools are mission-critical and designed to meet a specific solution that is very specific to an industry, or to a particular person in the industry, and solves only a specific problem. The company is bringing its mission-critical abilities into the generative AI space as well, in order to capture the demand and opportunities arising from generative AI. For instance, in the second quarter of 2023, the company launched MADDI, Aderant's generative AI enabler that powers Onyx. Onyx is intended to address a major issue that all law firms face: how to navigate outside counsel guidelines and biller requirements imposed by clients. It's not unusual for a large law firm to have to deal with hundreds of thousands of unique client billing requirements. As a result, Onyx will extract contractual terms and convert them into business tools used in the time entry and billing processes using its generative AI technology. MADDI will be widely integrated across Aderant's product platforms over time, helping the company increase its exposure in the generative AI market. Further, Roper's DAT business is launching a Generative AI-enabled solution targeted to combat trade industry fraud. This is in addition to their existing set of Computational AI and data science-driven solutions like DATIQ.

Moreover, during the earning call of the second quarter, CEO Laurance Neil Hunn commented:

More broadly across Roper, we're excited about the potential of Generative AI and large language models. We believe, given our deeply verticalized and application-specific business model, that our businesses are structurally advantaged given that all AI, computational and generative, need context, specifically data and workflows in which to train or target the technology"

So, I believe Roper's ability to provide value to customers through its mission-critical or application-specific software along with the growing demand for both computational and generative AI-enabled technology should help it retain and acquire new customers moving forward and help the top line in many years to come. So, the end markets should continue to remain favorable for the company.

In addition, I also believe Roper's focus on strategically shifting its business portfolio from industrial-based to software-based over the past years is bearing fruits. Roper had industrial exposure prior to 2028 in markets such as pumps, valves, energy, and auto. In an effort to remove business cyclicality, the company divested its industrial businesses, which comprised 40% of its 2018 revenues, over the last few years. This has removed the cyclical nature of the business and the company also focused on increasing its recurring revenue base for the long-term growth of the business.

Currently, the company is 75% software and 25% technology-enabled products with 80% of its revenue recurring in nature. The company is continuously making efforts to cross-sell and up-sell its customer base from on-premise to the cloud through expanding its Software-as-a-Service [SaaS] offerings. The company's foundry business commenced the transition to a subscription pricing model for its core product - Nuke -at the beginning of the current year. Now, as of the second quarter, ~60% of Nuke's units sold were on a subscription basis and management estimates that by next year, 100% of Nuke's units should be sold on a subscription basis. This should further increase the recurring revenue for the company and help sales growth in the coming years.

So the company's organic sales have good long-term growth drivers from favorable end-market demand and increasing strength of the recurring revenue base. In addition, the inorganic sales growth drivers from its M&A strategy should also continue supporting the overall top-line growth momentum. The M&A strategy focuses on expanding the company's footprint in niche markets by acquiring assets-light businesses with high margins and recurring revenue. As these strategic acquisitions have leadership brands in their respective niche markets, this strategy is assisting the company in gaining market share.

In line with the M&A strategy, the company regularly makes small tuck-in acquisitions complemented with occasional large platform acquisitions, as it did with Vertafore in 2020 and Frontline Education in 2022. Roper continues to expand its portfolio of niche businesses. The company announced the acquisition of Replicone for Deltek in the second quarter, which is Roper's largest bolt-on. Replicon provides a market-leading timekeeping and workforce management SaaS solution focused on professional service firms. The business is expected to contribute $70 million in sales in the next year. This should further strengthen the company's market share position. For further strategic M&As, Roper's balance sheet continues to remain healthy with a leverage ratio of 2.2x at the end of the second quarter. So, the revenue growth should continue to see benefits from the bolt-in M&A strategy.

Management has increased the guidance for 2023, given the strength in the end markets. Organic revenue growth is now expected to come at 7%, at the upper end of the previously stated 6%-7%, while the overall revenue is expected to grow 13% YoY. I believe the guidance is achievable as the company should continue to benefit from favorable end-market growth trends, improved business portfolios, and M&As. Hence I remain optimistic about ROP's revenue growth prospects ahead.

Margin Analysis And Outlook

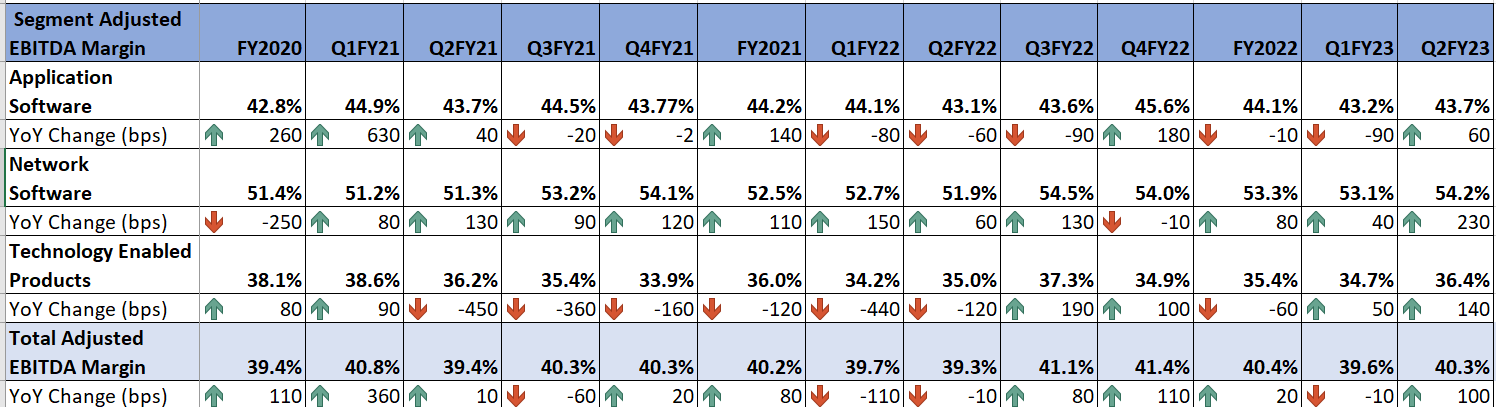

In the second quarter of 2023, Roper's margins benefited from good operating leverage driven by increased volume growth, easing supply chain headwinds, and a growing portfolio of high-margin businesses. These tailwinds helped more than offset additional costs associated with the ramp-up of implementation capacity in the Application Software segment. This resulted in an adjusted EBITDA margin increase of 100 bps YoY to 40.3%. The margin growth was led by the Network Software segment, which grew adjusted EBITDA margin by 230 bps YoY. The Application Software and Tech-Enabled Product segments grew adjusted EBITDA margin by 60 bps YoY and 140 bps YoY respectively.

ROP's Historical Adjusted EBITDA Margin (Company Data, GS Analytics Research) ROP's Segment-Wise Historical Adjusted EBITDA Margin (Company Data, GS Analytics Research)

{kind=link}

Looking forward, I expect Roper to continue expanding its margins. The company is experiencing broad-based easing of supply chain challenges in its Tech-Enabled Product segment. This should help support margin growth in the coming quarters as headwinds from supply chain pressure become less of a margin drag. I also expect margins to see good benefits from operating leverage as revenue continues to increase moving forward.

Moreover, while the company is seeing good opportunities in the generative AI space to support the top line moving forward, it is also relying on generative AI internally to boost productivity for its daily operational process through digitalization and automation. The company is working closely with all of its businesses on the productivity and product-enabled opportunities associated with Generative AI. This should enhance efficiencies and help margin growth. The company should also continue to benefit from its improved business portfolio of high-margin and asset-light businesses, which should also boost the margin expansion in the coming years. Hence, I remain optimistic about the company's margin expansion prospects ahead.

Valuation and Conclusion

Roper is currently trading at a 30.29x FY23 consensus EPS estimate of $16.49 and a 28.06x FY24 consensus EPS estimate of $17.8. The company is trading at a premium to its historical 5-year average forward P/E of 28.66x if we look at FY23 consensus EPS estimates, and almost in line with its historical valuation if we look at FY24 numbers. The company has good long-term growth prospects, benefiting from secular demand trends from AI and generative AI products, an improved business portfolio, an accretive M&A strategy, and improved productivity and efficiencies. However, the growth prospects seem to have already been reflected in the current valuation. Hence, I would prefer to wait on the sidelines for a more attractive entry point and have a neutral rating on the stock for now.

For further details see:

Roper Technologies: Moving To Neutral Post The Recent Run-Up