ROP - Roper Technologies: Steady Growth Continues

2023-06-10 05:14:59 ET

Summary

- Roper Technologies is a serial acquirer of over 50 businesses, focusing on asset-light, cash-generating companies with high barriers to entry and market leadership in their niche.

- The company has been transitioning from industrial to more tech-focused, with strong organic growth and a decentralized operational structure.

- Valuation of Roper is challenging due to its unique business model, but the company has consistently outperformed the S&P 500 since its IPO in 1991.

Today's article focuses on Roper Technologies, the serial acquirer of diversified technologies.

We will focus on the company's operations, moat, capital allocation, and valuation.

Let's dive in.

Business Overview

Roper Technologies (ROP) is an acquirer, integrator, and operator of over 50 businesses in various industries. Roper focuses on asset-light businesses, focusing on companies that generate cash flow each year. The company is transitioning from industrial to more tech-focused with recent divestitures.

Once it acquires these businesses, the company operates in a hands-off method, preferring mgmt stay in place to continue running the business. Roper does a great job investing in R&D, integrating the new acquisitions, and allocating capital for shareholders.

As I mentioned a moment ago, the company is divesting a majority stake in its industrial segment, which, once done, the company will realign into two segments:

- Vertical Software

- Medical & Water Products

Roper focuses on buying businesses that fit a particular niche with specific characteristics. They don't stick to one or two specific niches. Instead, they focus on companies that meet their four criteria:

- Roper's CRI (Cash Return on Investment)

- Management can thrive under Roper's ownership

- Businesses must have a moat, or high barriers to entry,

- and be a market leader in the niche.

Let's unpack those for a moment.

Roper's cash return on investment is an internal metric measuring cash flow growth and disciplined investments. The company measures CRI as (Net Income + Depreciation - Maintenance Capex) / (Net working capital + Net PP&E + Accumulated Depreciation)

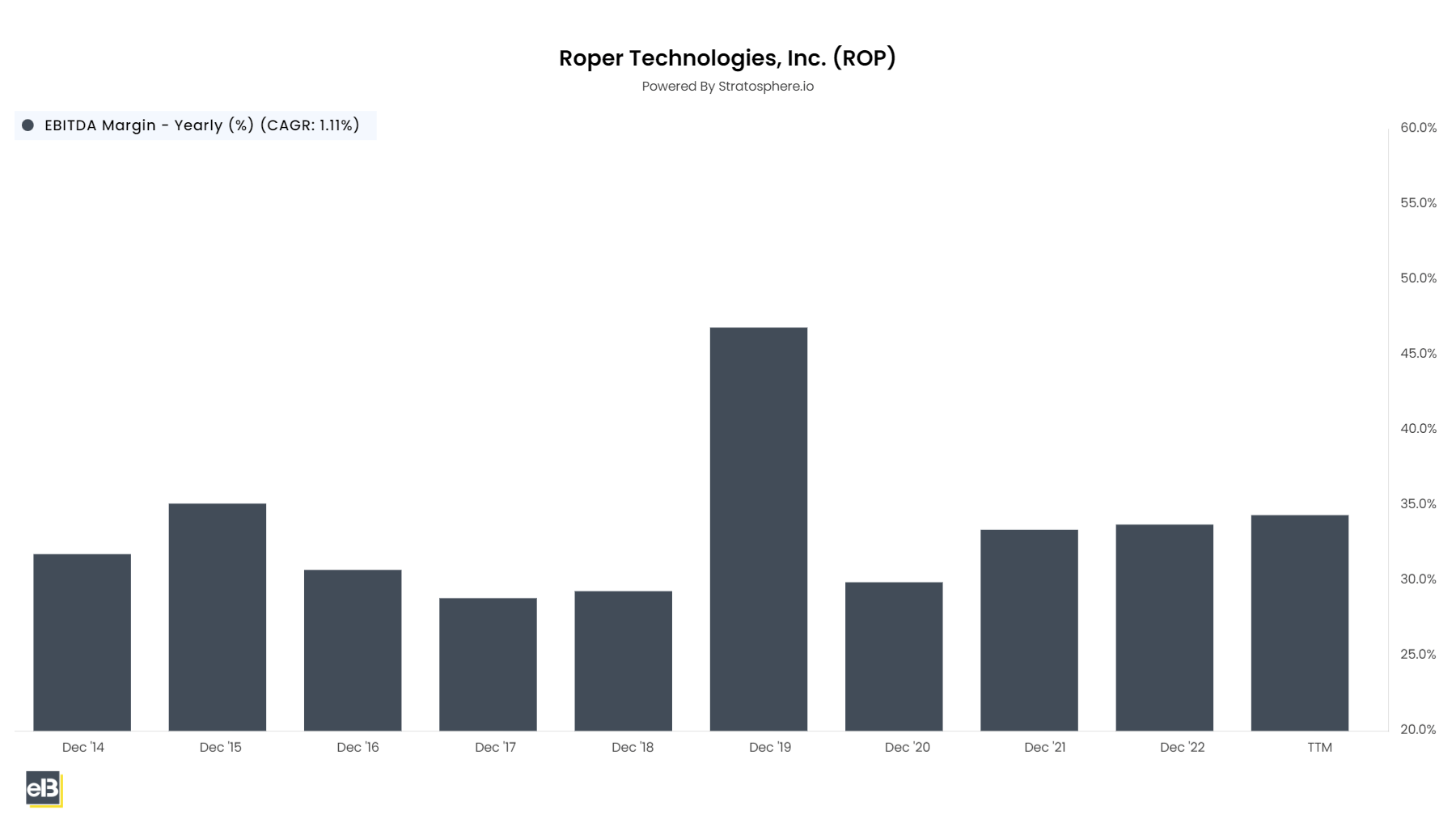

Roper currently runs an EBITDA margin of 40%, with stock-based compensation running through the number, which Neil Hunn, CEO, claims is a "very clean number."

{kind=link}

Roper sources their targets almost exclusively from PE firms. Roper likes to approach PE (private equity) after they've owned a business for three years, giving them time to clean them up before they would likely IPO. Roper also likes to acquire established market leaders with defensible niches.

Over the past decade, Roper has acquired almost 60 businesses, and most of those acquired were platform deals. This has all been part of the transformation to a more software-focused business. Roper, like most businesses, loves the recurring nature of these revenues.

Roper has also continued divesting of the more cyclical businesses, 16 of those in the latest divestiture in June 2022. Roper now carries 28 businesses in its portfolio.

Once Roper acquires a business, they allow it to continue running without much interaction from HQ.

They run each business decentralized with little overlap in backend systems and resources between segments. Each business operates as a standalone company, making resource and capital decisions for their business.

Roper focuses on software companies with large amounts of deferred revenue. Large quantities of deferred revenue exist because many software businesses receive cash far in advance when rendering services. Roper uses this cash to invest in businesses at incrementally higher rates of return.

Roper's businesses typically don't own their infrastructure, contributing to its asset-light business model. From 2003 through today, Roper's net working capital as a percentage of sales has dropped from 18% to negative 13%.

Roper runs a decentralized structure for operations, but capital allocation remains centralized. Headquarters makes all decisions on allocating capital from excess returns, focusing on new platform acquisitions, paying down debt, and R&D.

Business Operations

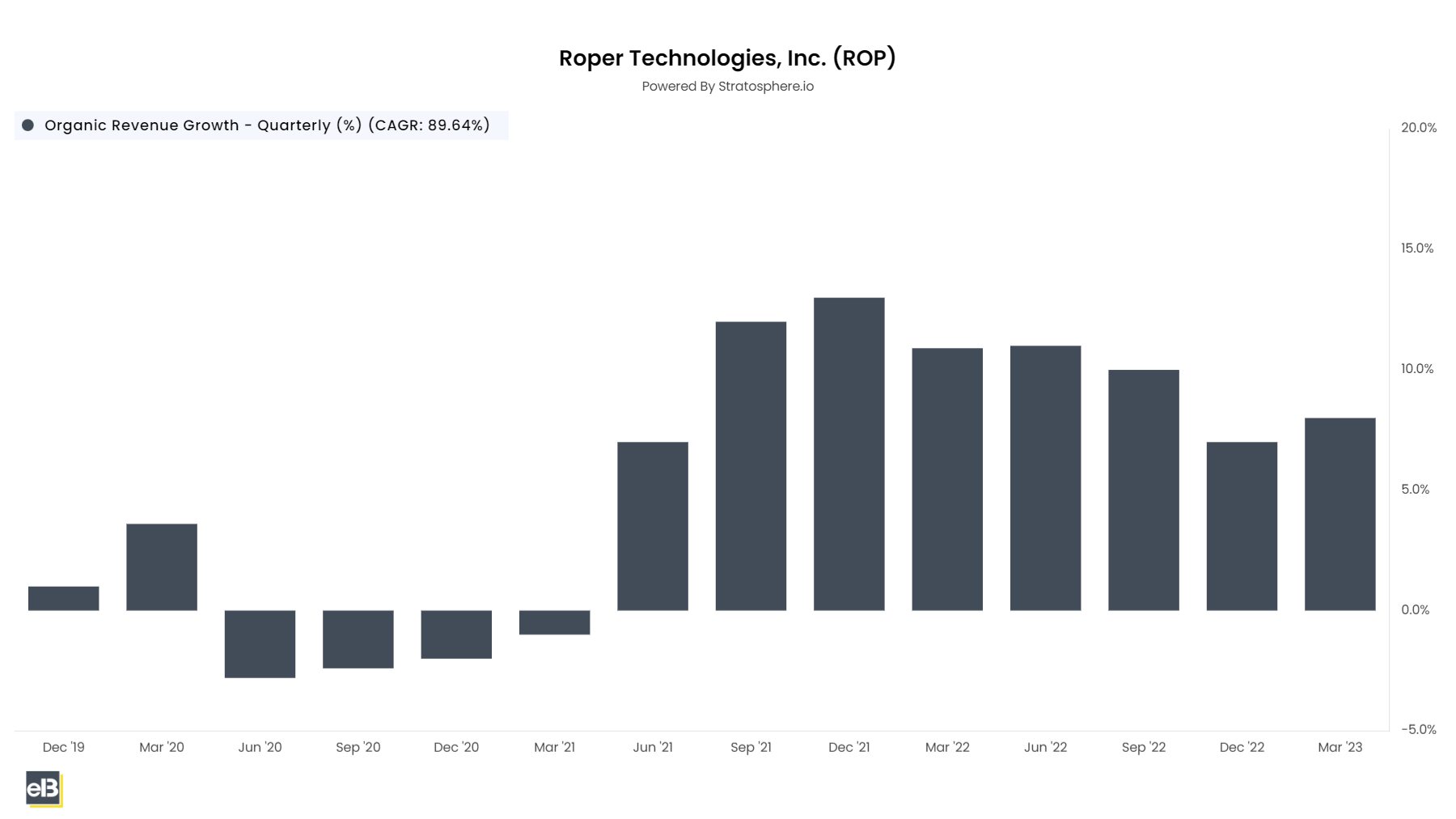

Roper focuses on organic growth with average organic growth of 4%, focusing on acquisitions in the $200 million range, 40-50% EBITDA margins, with mid-single to high single-digit organic growth. Roper averaged organic growth of 4.2% over the past decade.

Over the last eight quarters since June 2021, Roper has generated at least 7% organic growth, including this quarter's result of 8%.

{kind=link}

Seeing organic grow is a great sign for a serial acquirer like Roper. Focusing on organic growth for acquirers like Roper is important because many acquirers can cover up core growth by making more acquisitions. But as we can see, Roper isn't falling into this trap.

Over the past few years, as Roper has transitioned to their new business model they have acquired bigger companies.

Roper, often compared to Constellation Software (CNSWF), focuses on larger targets, while Constellation focuses on small VMS businesses of a certain size and valuation. This allows Constellation to buy lots of companies, upwards of 100 last year.

But one chink in the armor is the lower organic growth than Roper, with organic growth negative for the past year.

If we break down Roper's revenue in the most recent annual report, we see:

- Application Software = $2.64 billion (49.14%)

- Network Software = $1.38 billion (25.66%)

- Technology Enabled Products = $1.35 billion (25.20%)

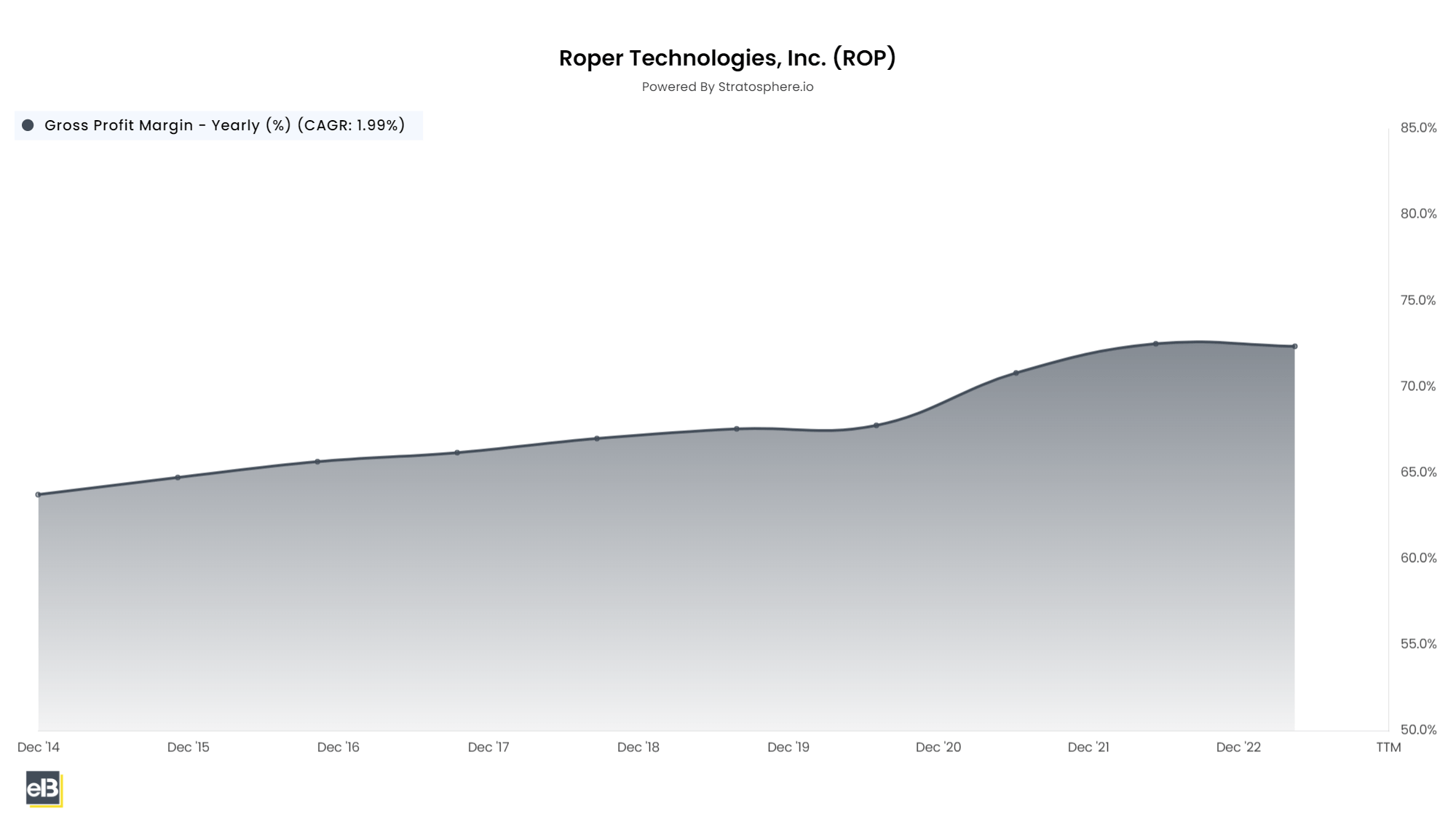

The revenue growth has translated to growing gross margins as the company continues to evolve to the newer business model. Margins have grown 1.99% CAGR over the past ten years while growing from 59.4% to 69.7% in the last trailing twelve months.

{kind=link}

Capital Allocation

Roper focuses on allocating upwards of $2-$3 billion annually, but with the recent divestiture, combined with ongoing deleveraging, the company is sitting on over $7B in dry powder. They now have some money to deploy but expect to be patient, per their usual pattern.

Roper's financial position consists of cash and cash equivalents of $792 million and total debt of $6,661 million. Roper has reduced the debt from a high of $9.5 billion to $6.6 billion over the past two years. Roper also carries a Moody's credit rating of Baa2, an investment grade. The company also has an untapped credit facility of $3.5 billion available.

Free cash flow has dropped in the past few years, primarily because of the following:

- Higher taxes related to the 2021 divestitures

- Less cash provided from working capital, mostly from higher compensation payments.

Roper's free cash flow yield equaled 1.5% in 2022, and the TTM margins equaled 11.6%, all down due to the above mentioned reasons.

Along with the firepower from free cash flow and credit facility for any acquisitions, the company also is a dividend aristocrat, paying a dividend of $2.73 per share, with a yield of 0.60% and a payout ratio of 16.87%.

Risks

As with any company focusing on technology, Roper faces risk in product launch failure with any software from its verticals and cybersecurity risks.

But, as with any serial acquirer, the greatest danger is that the current management will misjudge the deal's economic potential or overlook specific competitive risks in a target's markets. Neil Hunn, CEO, and the team have done a great job carrying on former CEO Brian Jellison's framework.

Although Roper has never had to take an impairment charge due to an acquisition, if its market capitalization increases, it might eventually have to, even if it's many years away.

In some aspects, size itself might become a problem in the future, although this will be more of a problem after the next 15 years as the company grows.

Management

Using Glassdoor as a proxy for culture, it appears that Roper ranks in the lower end of its peers, with a lower ranking for its CEO:

- 3.2/5 stars

- 42% recommend working there to a friend

- 58% approve of the CEO

Albeit all of this with lower reviews, only 37, a small sample size may play a part. So inconclusive on the culture.

Neil Hunn has led Roper since August 2018 , and the average tenure of the management and board of directors equals 5.4 years and 8.1 years, respectively. Hunn worked as the COO prior to becoming the CEO, albeit for less than one year. He started working for Roper in 2011 as a Group Vice President.

Hunn has continued the changing of the guard for Roper since the unfortunate passing of Brian Jellison. He has helped steer the company through a difficult passage from industrial to SaaS while reducing the debt load from recent acquisitions.

Regarding strategic focus, I like management's approach to shifting Roper towards a SaaS model and the continued emphasis on a decentralized approach to managing its assets while maintaining a more strict approach to acquisitions.

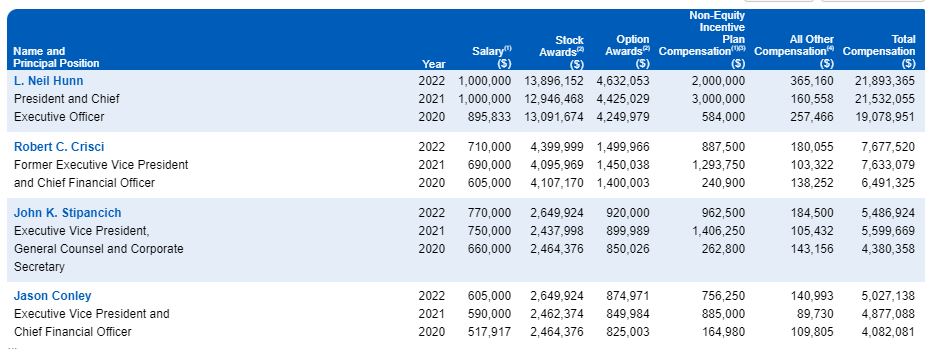

Digging into pay, we see the CEO pay ratio equals 244:1. The executive compensation includes annual base salary, annual stock awards, option awards, non-equity incentive plans, and others.

{kind=link}

The company's equity awards will vest after three years, in the form of 50% performance stock units (PSUs)(payable based on the achievement of three-year cumulative financial goals and vest on the third year) and 50% stock appreciation rights, with a three year cliff vesting period.

Annual bonuses are based on adjusted EBITDA and operating cash flow, based on 3-year targets for the above metrics compared to their stated peers.

Most of the CEO's compensation is in the form of long-term incentives (62%), which is fair and similar to others in the peer group. Per Simply Wall St, the CEO's total payroll of $21.89M is above average for companies of similar size in the US market ($12.M)25, therefore, we can conclude that the package is a little high and may not align with shareholders.

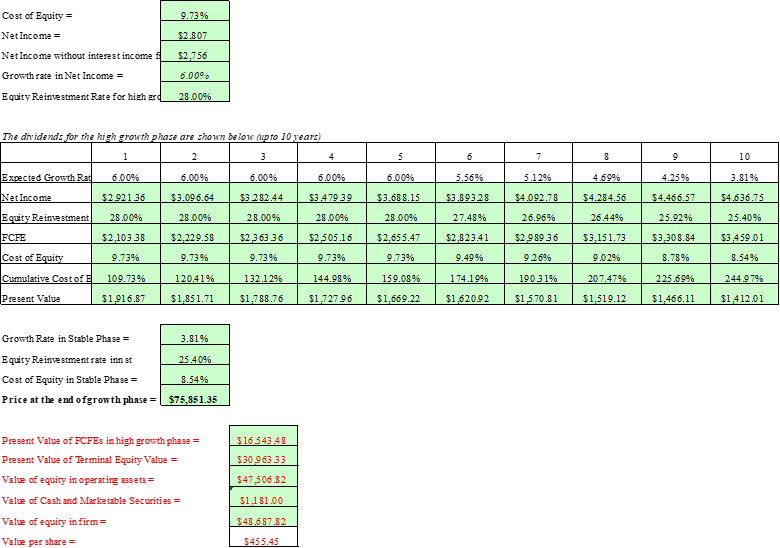

Valuation

Valuing Roper is challenging because of how they operate; instead of using my usual FCFF, we will use an FCFE to measure the value of equity and reinvestments to give us a value of the growth of the company's earnings.

Because Roper sees a drop in capex compared to revenues over the years, the company needs little reinvestment to grow FCF/EBITDA.

The model below assumes:

Net income growth = 6%

Cost of equity = 9.73%

Reinvestment rate = 28%

Stable growth rate = 3.8%

{kind=link}

If we give a fair value of $455+, which gives us a fair value close to market value, which tells me we are "approximately correct."

Investor Takeaway

Roper is a strong company with predictable/recurring revenues, high margins, low competition in a defensible niche, higher terminal value, low need for capital and assets to grow, low or even negative net working capital, differentiated/custom products, and services.

I love the execution of the switch from industrial to SaaS, the continued discipline in acquisition targets, and the paying down of debt. They have bought great businesses which generate good organic growth.

I am long on Roper, and the company has outperformed the S&P since its IPO by 2,122% to 515% since 1991. They might be one of those quality companies that never intrinsically approach "fair value" but deliver strong returns.

For further details see:

Roper Technologies: Steady Growth Continues