ROST - Ross Stores: Business Fundamentals Should Continue To Stay Strong

2023-07-06 06:26:19 ET

Summary

- Despite facing challenges such as inflation and weather disruptions, Ross Stores has shown resilience with a 1% increase in same-store sales in Q1 2023.

- I expect ROST to benefit from the current macroeconomic environment, with its focus on value for low to moderate-income consumers and potential for improved gross margins.

- Although a cautious outlook is advised due to the ongoing weak macro situation, the company could exceed current estimates and restore margins to pre-recession levels.

Overview

Ross Stores ( ROST ) owns and manages two different discount retail chains known as ROST Dress for Less and dd's DISCOUNTS. The company's strong performance has led management to raise their guidance for FY23, so I'm keeping my buy recommendation . Nonetheless, I am now much more cautious in my outlook (in comparison to my first post) as it continues to face a challenging macro, with the lower income consumers increasingly focused on value as a result of inflationary cutting into discretionary spending budget. I also didn't account for the weather, which proved to be an uncontrollable variable and a drag on performance in California and the West by delaying the start of the spring buying season. However, ROST still managed to grow comp at 1% in 1Q23 despite these headwinds, and the company is seeing positive trends in business on a 4-year stack basis. In contrast to price, which has been a key driver for many businesses due to inflation, traffic was the primary contributor to 1Q23 performance. I continue to think ROST's sequential improvements in providing more value to customers will lead to above-average revenue and profit growth compared to the rest of the retail industry.

Revenue growth

When compared to management's guidance of flat same-store sales, ROST's 1% increase was a 100bps beat. In this regard, I think the ROST business model really shines, as customers are becoming increasingly price-conscious. In contrast to many other stores, ROST benefits the more inflation persists. In my opinion, ROST is a share taker rather than a share giver due to the fact that high inflation causes consumers to trade down. I would expect management to roll out much more variety of items to meet the expanded demand preference as more consumers trade down. This line of thinking accords with management comments that traffic was the primary driver of 1Q23 performance. Without the weather drag, I believe growth would have been even more impressive. Management noted that as the weather improved, they saw a positive trend in customer traffic that lasted several years.

In terms of the overall supply situation, I have no concerns because the management assures that there is an abundant availability of products across various businesses and brands in the market. As long as ROST maintains its strategy of offering more value to its low to moderate income customers, who are particularly impacted by substantial inflationary pressures, I am confident that ROST will sustain its performance.

Margins

As ocean freight conditions improve and the new distribution center in Houston nears capacity, ROST should see a rise in its gross margin. The enhanced gross margin should trickle down to the operating margin and drive expansion. Looking at consensus estimates, they expected EBIT margin to be flattish in FY24 and expand 50bps moving forward. Given that ROST has typically been the driver of a 13-14%+ EBIT margin in normal times, I think this may be too conservative. Given the decline in ocean freight and the uptick in traffic, I anticipate a much quicker increase in margin. Consensus is likely conservative because it mirrors management's cautious tone on the 1Q23 earnings call, but I anticipate a revision of estimates once ROST proves it can restore margins to their pre-recession highs.

Valuation

According to my updated view on ROST, I expect ROST to continue growing margins as previous freight headwinds turn into tailwinds and distribution center utilization ramps up to drive fixed cost leverage. However, due to the ongoing weak macro situation, I now expect a slower growth rate as I incorporate more conservative assumptions into the model. ROST, on the other hand, is still a winner in this market, as I expect consumers to continue trading down to cheaper and more valuable goods.

As a result, I expect growth to be in line with consensus (mid single digits) for my model. Profitably, I disagree with the consensus because I believe margins should return to historical levels at a faster rate. ROST should achieve comparable profitability as a normalize period (pre-covid) if there is no specific reason why it cannot, especially when the environment is well set up for success.

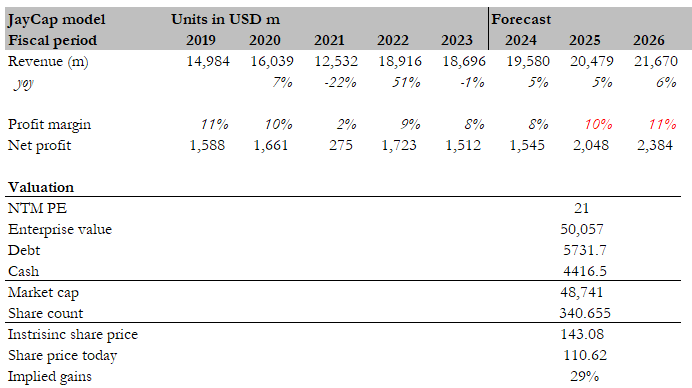

I calculated an intrinsic value of $143, 27% higher than the current share price of $110.62, assuming the aforementioned assumptions and a 21x NTM PE (which is where it is trading today).

{kind=link}

Risks

This inflationary environment is beneficial for the business sector in which ROST operates. However, if inflation were to skyrocket to an extremely high level, ROST may find it difficult to price goods in line with inflation and wages. This may result in a diminished value perception among customers if consistent price increases are required.

Conclusion

Despite some challenges faced by ROST, such as the impact of inflation and weather-related disruptions, the company has shown resilience and continues to perform well. The 1% increase in same-store sales in the first quarter exceeded management's guidance and demonstrates the effectiveness of ROST's business model in catering to price-conscious customers. With an emphasis on providing value to low to moderate income consumers, ROST is well-positioned to benefit from the current macroeconomic environment. Additionally, I expect improved gross margins as ocean freight conditions improve and the new distribution center reaches capacity. While a cautious outlook is warranted, I believe ROST has the potential to exceed current estimates and restore margins to pre-recession levels.

For further details see:

Ross Stores: Business Fundamentals Should Continue To Stay Strong