ROST - Ross Stores: No Discounts For Investors

2023-03-26 04:53:45 ET

Summary

- ROST has established itself as a standout in the retail industry with a business model that delivers significant cost savings to its customers.

- ROST has a strong track record of generating free cash flow growth and profitability.

- Despite ROST's impressive financials and growth prospects, its current share price may give some investors pause.

Intro

Ross Stores, Inc. ( ROST ) has a successful business model in the retail industry, which offers its customers significant cost savings. ROST's stores provide off-price retail products that are usually 20% to 60% cheaper than traditional department stores. This approach has led ROST to establish strong financial performance over the years.

In addition, ROST's future is bright as the company has strong growth prospects, with the company continually adding new stores to its portfolio. The firm is executing a disciplined expansion strategy that focuses on markets where it can effectively compete with other retailers.

The article aims to investigate ROST's business model and financial performance in more detail, including its outlook for the future. By exploring these factors, the article seeks to determine the company's intrinsic value, including growth prospects and potential risks associated with its business. The analysis can help investors make informed investment decisions.

Business Model

ROST manages two types of discount retail stores for clothing and home decor, which are named Ross Dress for Less and dd's Discounts. The California company has been in business since 1957 and today has almost 1700 stores, making ROST the biggest chain of off-price retail stores for clothing and home decor in the United States. The company's dd’s DISCOUNTS brand adds 323 stores more stores to its portfolio.

The company drives value for its customers by offering customers with in-season, high-quality apparel, accessories, footwear, and home decor from name brands and designers at discounts ranging from 20% to 60% off department store prices. ROST achieves this by purchasing overproduced or excess inventory merchandise from manufacturers.

ROST's competitive advantage revolves around its ability to maximize its inventory turnover and customer traffic through using an opportunistic merchandising strategy and a low-frills store layout that focuses on the thrill of the treasure hunt. This approach enables the company to maintain its low-price strategy and pass on savings to its customers which has allowed the company to build a loyal customer base that appreciates the value it offers.

Track Record

In the past ten years, ROST has achieved consistent revenue growth, with the latest fiscal year reporting $18.9 billion in revenue, representing a 94% increase from ten years ago. Equally noteworthy is the fact that the company has grown its revenue in every year except one year over the period. The one year the company had experienced a revenue decline was 2020 the year of the COVID-19 pandemic.

Data by Stock Analysis

In addition, ROST has exhibited substantial growth in its free cash flow, as the company announced of $1.1 billion in free cash flow during the latest fiscal year. This impressive figure represents a remarkable 98% increase in free cash flow over the preceding ten years.

Aside from its impressive growth, ROST has demonstrated remarkable profitability over time. For the past decade, the company has maintained an average return on equity of over 41%, with just one year falling below 40% which was in 2020 when the company reported just 2.8% due to the COVID-19 pandemic.

Data by Stock Analysis

Looking at ROST's balance sheet, it's apparent that the company has achieved significant growth in its book value. Over the last decade, ROST has increased its book value by over 186%. Additionally, the company boasts an interest coverage ratio of over 700, providing further confirmation that its balance sheet is in excellent condition.

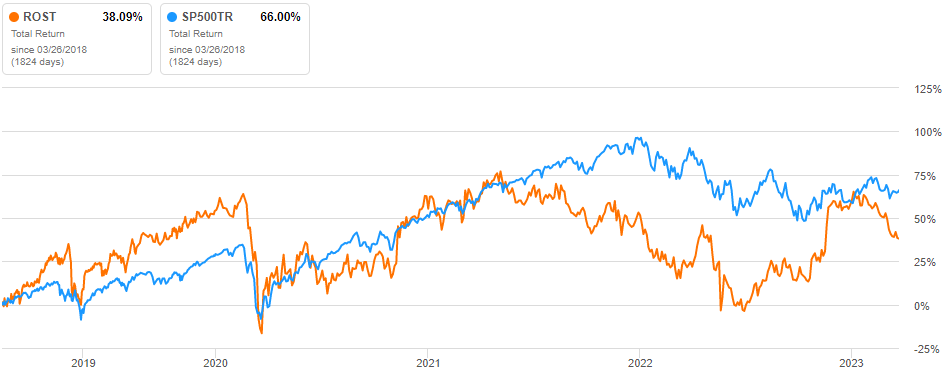

ROST's exceptional track record has not provided outstanding returns to its investors. Over the last five years, the company's total return has trailed the total return of the S&P 500, 66% to 38%. Such performance has raised concerns among investors about whether ROST can turn its stock performance around.

{kind=link}

Outlook

ROST growth strategy revolves around opening more stores in areas with high market penetration, favorable demographic characteristics, limited competition, anticipated profitability, and the ability to benefit from shared expenses. The company has big plans in 2023, because it's planning on opening 100 new stores in 2023. These new store openings will be comprised of 75 new ROSS stores and 25 new dd's DISCOUNTS stores.

Last year, the company had roughly $700 million in capital expenditures , majority of which will be channeled towards fortifying its supply chain infrastructure to drive long-term growth. This includes constructing a new distribution center, as well as funding fixture and leasehold improvements for our planned Ross and dd's DISCOUNTS stores.

ROST is subject to a few risks including external factors such as the overall state of the economy, fluctuations in financial and credit markets, and geopolitical conditions can all have a negative impact on its business. This is because these factors can affect consumer confidence and the amount of money consumers have available to spend at ROST stores. At present, the economy is marked by increasing interest rates and elevated levels of inflation, which are limiting the amount of disposable income that consumers have, creating a significant head wind for ROST.

Despite concerns about rising interest rates and inflation, analysts are forecasting a return to growth for the upcoming year, with average earnings estimate of $ 5.04 for this year and $5.58 for the following year. Additionally, analysts' revenue projections are set to increase, with an estimated $19.6 billion this year and $20.6 billion in 2025. As long as ROST maintains its successful growth strategy by expanding its store count and investing in long-term growth projects, such as the new distribution center, the company is well-positioned for a bright future, particularly as the overall macroeconomic environment improves.

Valuation

We will use two methods, comparative analysis and discounted cash flow ("DCF") analysis, to determine ROST's intrinsic value. First, we will perform a comparative analysis by reviewing ROST's historical highest, lowest, and median price-to-earnings (P/E) ratios over the past five years, as well as the sector median P/E ratio of 14.70 . By applying these ratios to ROST's consensus 2023 EPS estimate of $ 5.03 per share, we will establish its fair value based on the market's past valuation patterns.

| Scenario |

| P/E |

| Next Year Earnings Estimate |

| Intrinsic Value Estimate |

| % Change |

| Bear Case |

| 13.04 |

| $5.03 |

| $65.59 |

| -35.27% |

| 5Y Median P/E |

| 24.34 |

| $5.03 |

| $122.43 |

| 20.82% |

| Bull Case |

| 570.35 |

| $5.03 |

| $2,868.86 |

| 2731.21% |

| Sector Median Valuation |

| 14.7 |

| $5.03 |

| $73.94 |

| -27.03% |

Assuming a bullish scenario is unrealistic to take place with a multiple of 570.35 we will focus on the other data points. In the bearish scenario, if ROST is valued at the low P/E ratio of 13.04 applied to next year's average earnings estimate of $5.03, investors may incur a significant loss of over 35%. Meanwhile, if ROST is valued at the sector median multiple, investors would suffer a loss of 27%.

The base case scenario for ROST, based on the 5-year median P/E ratio, is deemed the most likely outcome and therefore, it is crucial for investors to consider. If this scenario does come to fruition, investors could potentially gain almost 21%.

Overall, the comparative analysis indicates mixed results for ROST valuation, and at the company's current market price ROST doesn't appear to be obviously undervalued or overvalued.

To start the discounted cash flow analysis, we will utilize the average free cash flows of ROST from the previous five years, which were $1.5 billion. We will use a growth rate of 7% for the next ten years which would double the company's free cash flow over the period based on rule 72.

We will follow rule 72 since making precise predictions about free cash flow growth rates spanning several years can be challenging. Nevertheless, considering ROST's history of growth and the long-term growth prospects, I am confident that the company has the potential to double its free cash flow over the next decade or more.

Following the 10th year, we will assume a growth rate of 2.5% to find the company's terminal value. The discount rate used to discount cash flows in the DCF analysis will be 10%, reflecting the long-term return of the S&P 500 when dividends are reinvested.

Based on these inputs, the DCF analysis indicates an intrinsic value of $64.83 per share. This suggests that investors could experience a potential loss of 36%. Therefore, ROST is currently overvalued at its current share price based on this DCF analysis.

{kind=link}

Takeaway

ROST has established itself as a standout in the retail industry with a business model that delivers significant cost savings to its customers. ROST's stores offer off-price retail products that are generally 20% to 60% cheaper than those found at traditional department stores by purchasing merchandise from manufacturers that are overproducing or have excess inventory. This model has resonated with consumers, as ROST has produced consistent same-store sales growth and customer loyalty.

ROST has a strong track record of generating free cash flow growth and profitability. The company's operating cash flow has consistently outpaced its capital expenditures, resulting in positive free cash flow. In addition, ROST's future growth prospects are particularly promising in light of the company's successful expansion strategy. ROST has continued to add new stores to its portfolio, with plans to open 100 new locations in 2023.

Despite ROST's impressive financials and growth prospects, its current share price may give some investors pause. A discounted cash flow analysis suggests that ROST's shares may be overvalued. The high share price reflects optimistic expectations for the company's future growth prospects and profitability. While ROST has a history of strong financial performance, and a bright future to match, all this must be compared with its share price. As such, investors should exercise caution and carefully evaluate ROST's current valuation before making any investment decisions.

For further details see:

Ross Stores: No Discounts For Investors