ROST - Ross Stores: P/E Derating To Pressure Stock Initiate At Sell

2023-05-18 10:30:44 ET

Summary

- Ross remains one of the standout players in off-price retail segment which is likely a beneficiary as consumers trade down.

- Exposure to lower end of consumers likely to drive sales growth lower.

- We believe as growth trends normalize, Ross will likely face PE derating.

- We maintain a sell rating on the company with a target price of $93 at 20x PE.

Investment Thesis

Ross Stores (ROST) has significantly underperformed its major rival TJX Companies (TJX) due to decelerating foot traffic, slowing sales and weaker operational performance.

Consumers prefer off-price retailers during downturns as they trade down and look for more value for money deals. However, ROST primarily caters to lower income consumers which are likely to cut back on their discretionary spends due to inflation and an impending recession. This also comes back on account of lower tax refunds and end of the SNAP benefits which were continuing since the pandemic and had significantly benefited the lower end of consumers. We believe the company will likely witness a PE derating as growth trends normalize and EPS is revised downwards. We initiate the stock as Sell with a target price of $93 (at 20x PE, in line with its long term average).

Earnings Preview

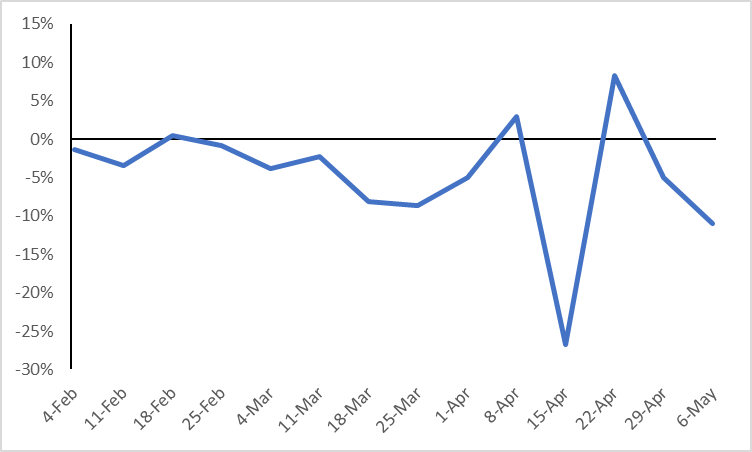

We expect ROST to post a sales growth of less than 2% vs consensus expectation of 4-5% growth factoring a negative comp growth as traffic has steadily decelerated over the quarter, according to the data from Placer.ai. While February was relatively strong, traffic deteriorated further in March to pick up in April during Easter holidays, but remained relatively flat. This also comes against a weaker quarter in Q1 2022 where comp sales declined by a significant 7%.

Weekly Average Traffic Growth YOY

{kind=link}

It plans to open about 100 stores in FY23 including 22 new stores in Q1 FY23 (11 each of Ross Dress for Less and DD's Discount) which would offset the losses due to declining foot traffic and we project a positive sales growth.

Gross margins will likely remain under pressure due to occupancy cost deleveraging and promotional environment offset by freight tailwind, particularly with ocean rates. We also expect SG&A $ to increase over 5% YoY as the company complies with state-wide and local municipality statutory wage increases at half of its stores along with higher incentive compensations. Given negative comp growth and margin pressure, we believe the company to post an EPS below its Q1 guidance of $0.99-$1.05.

Guidance for FY23

Management has guided for a 2-5% sales growth and flat comp growth for FY23 as well as in line operating margins compared to FY22. We believe the exit rate from Q1 will continue to pressure sales trends in Q2 and management is likely to revise the guidance downwards. Further, while freight and easy supply chain are likely tailwinds for the margin, we believe slower than expected sales will lead to fixed cost deleveraging which will offset much of its positive margin drivers for FY23. As a result of the same, we believe the EPS outlook for the year is likely to be revised downwards from a midpoint of $4.80 to the lower end of the earlier guidance.

Valuation and Final Thoughts

ROST is one of the defensive stocks within the off-price retail segment that has performed historically better during an impending recession. However, the bar for the company is set higher and we believe given the trends and channel checks, the performance is likely to fall short. ROST currently trades at more than 15% premium to its long term average of 20x PE, given the growth prospects that the street is anticipating.

However, we believe that as the growth trends normalize, it will lead to downward EPS revisions and PE derating and ROST will likely revert back to its long term average of ~20x P/E. We rate the shares as Sell with a target price of $93.

Risks to Rating

Risks to rating include 1) more than anticipated tailwinds on freight related expenses 2) deteriorating mall ecosystem and store closures of competitors (such as Bed Bath & Beyond) could lead to gain market share for ROST and aid higher comp sales growth 3) access to high quality inventory and product assortment would drive sales while maintaining margins 4) overall demand improvement in home improvement segment and 5) investments in supply chain, technology and automation could lead to a higher than anticipated margin expansion.

For further details see:

Ross Stores: P/E Derating To Pressure Stock, Initiate At Sell