ROST - Ross Stores: Recovery On The Way As The Worst Is Likely Over

2023-05-18 09:51:15 ET

Summary

- Over the last three years, Ross Stores was impacted by the COVID-19 shutdowns, rising inflation, as well as skyrocketing ocean container shipping, freight, and wage costs.

- I believe the worst is over as the COVID health emergency has ended, more employees return to the office, container shipping costs fall to pre-COVID levels, and freight costs recede.

- Even though retail wages continue to rise as the labor market remains tight, I believe margins will recover in the near to intermediate term.

- My long-term investment thesis continues to hold up. As such, I rate Ross a hold.

Overview

The last several years have not been kind to Ross Stores ( ROST ) as the company was hit from multiple directions by exogenous factors. Apparel stores were deemed "non-essential" and shut down by the authorities in the early stages of the COVID-19 pandemic, rising inflation has crimped the appetite of their middle/lower-income core customer base for semi-discretionary goods like apparel, while Ross faced skyrocketing ocean container shipping, freight, and wage costs.

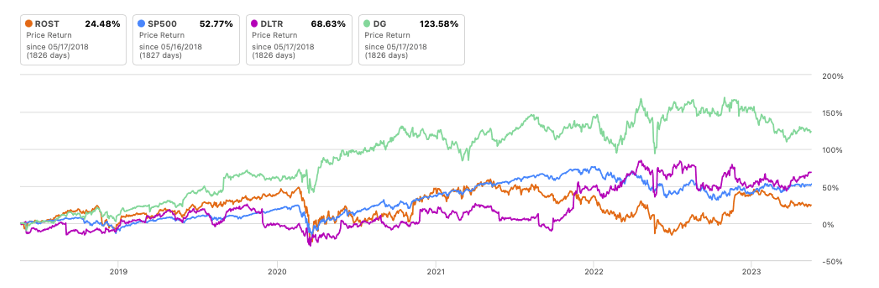

Over the last five years, Ross's stock price has only appreciated by 25% (Figure 1, orange line), significantly underperforming its discount retailer peers Dollar Tree ( DLTR ) and Dollar General ( DG ) - which have grown by 75% and 125% respectively (purple and green lines).

Figure 1: Stock price performance

{kind=link}

Even though the going has been tough, I believe the worst is over as (1) my long-term investment thesis continues to hold; and (2) some of the key causes of the weakness are receding.

My long-term investment thesis holds

1. Ross's core market of middle/lower-income consumers will continue to need to purchase good quality apparel

While consumers can postpone refreshing their wardrobes, they cannot do so indefinitely. If incomes continue to be squeezed by inflation of non-discretionary, consumers could start trading down from more costly retailers to Ross, and Ross customers could start trading down to the company's lower-end DD's Stores.

2. Low-cost retailer of quality and branded apparel and home goods

The company's value proposition to customers is to buy good quality and branded merchandise at below-departmental stores costs and sell the products at strong discounts to departmental stores on an ongoing basis.

This is sometimes accomplished by purchasing inventory later in the merchandise cycle than mainstream department and specialty stores to take advantage of manufacturers' "close-out" inventory, which consists of production overruns and other customers' cancelled orders. The close-outs can be sold in the same season or stored as packaway merchandise for sale the following year. As packaway merchandise, which sometimes account for nearly half of Ross' inventories, comprises mainly of fashion basics that are less affected by shifts in fashion trends, they can be sourced and sold at deep discounts to less fashion-conscious customers for whom it is not crucial to be seen in most up-to-date clothing and accessories.

The smaller and mom & pop retailers it competes against lack the scale, sourcing capabilities, or working capital to do so consistently as well as the financial stability. As these competitors fail in tough times, Ross is well-positioned to pick up their business.

3. More markets to penetrate

Ross currently operates over 2,000 stores-around 1700 Ross and 300 DDs stores-in 40 states (Figure 3), but there is still room to expand. Management noted the it believed there is potential for at least 1,000 more new stores over time, including 700 and 300 more Ross and DD stores respectively.

4. Operating leverage

Well-run retailers benefit from economies of scale and operating leverage over time, as Dollar General (Figure 2, blue line) and Ross (green line, until the COVID-19 outbreak) both demonstrated. (As a side, Dollar Tree's margins have shrunk, largely due to self-inflicted problems that began with its acquisition of Family Dollar Stores).

Figure 2 Net income margins

Created by author using public financial data

Ross's main problems are beginning to recede

Ross's revenue growth has slowed, and its margins have shrunk since the onset of the COVID-19 outbreak in 2020 as apparel stores were deemed "non-essential" and shut down by the authorities in the early stages of the COVID-19 pandemic, rising inflation has crimped the appetite of their middle/lower-income core customer base for semi-discretionary goods like apparel, while Ross faced skyrocketing ocean container shipping, freight, and wage costs.

Revenue growth slowed due to lower same store sales growth and store openings

From 2014-2020, revenue grew at a compounded annual growth rate of 7.8% p.a. but slowed down to 5.3% p.a. since 2020 (Figure 3). This is a result of the COVID-19 lockdowns in 2020, continued social distancing measures in 2021, the trend toward remote work, and the spending power of its core customers crimped by inflation.

Figure 3 Annual revenues from 2014-2023

{kind=link}

Adjusted 2-year comp store sales holding up

Ross's same store sales have been volatile. It surged in 2021 following the shutdown of its stores in 2020 but pulled back in 2022 against tough 2021 comps (Figure 3, solid blue line). Two-year stacked same stores sales (dashed orange line), which I believe is a useful measure as it smooths out the volatility, is beginning to return to pre-COVID levels.

Figure 4 Same store sales growth

Created by author using public financial data

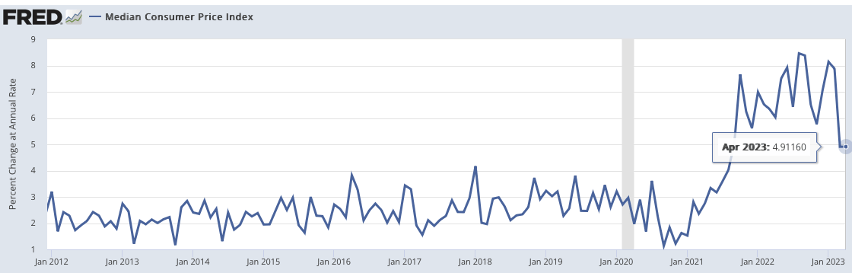

I am optimistic about the recovery now that the Center for Disease Control and Prevention has declared the end of the COVID health emergency. Life is returning to normal, more employers are summoning staff back to the office, and inflation showing signs of moderating (Figure 5).

Figure 5 Inflation as measured by the median CPI

FRED St. Louis Federal Reserve

{kind=link}

Continuing to open new stores

The company scaled back store openings in 2020 and 2021 in response to weaker consumer demand but has gradually resuming the pace of stores openings (Figure 6, dotted line), which should revive intermediate-term revenue growth.

Figure 6 Ross store count

Created by author using public financial data

Margin squeeze

Operating margins dropped to 10.65% for the year ended January 2022-the lowest in a decade if we exclude the year of the COVID-19 outbreak.

Figure 7 Annual operating margins

{kind=link}

Using numbers provided by management, the causes of the decline can be attributed to the sharp increase in ocean freight costs (under merchandise cost), domestic shipping costs, and wages (Figure 8).

Figure 8 Quarterly operating margin reconciliation

Company earnings calls

Ocean freight costs, as measured by the cost to ship a container from Shanghai to Los Angeles, quintupled from 2020 to 2021 but have retreated to early 2019 levels (Figure 9). Assuming Ross has longer term shipping contracts locked in at higher prices, merchandise margins will expand over time as these contracts expire.

Figure 9 Ocean container shipping costs (Shanghai to Los Angeles)

Statista

Domestic freight costs, which also surged in 2021, have started to pull back (Figure 10), which should also contribute to higher margins.

Figure 10 Domestic freight costs

FRED St. Louis Federal Reserve

On the negative side, retail employee wages continue to rise (Figure 11).

Figure 11 Retail employee hourly wages

FRED St. Louis Federal Reserve

The company trimmed operating expenses through lower SGA and buying incentives, both of which will likely rise over time. While Ross may be pressured to pass on some savings to its customers in the short term, I believe operating margins, which have languished at 7-year lows, will recover in the intermediate-term (Figure 12).

Figure 12 Quarterly operating margins

FRED St. Louis Federal Reserve

Ross's operating margins are significantly higher relative to its discount retailer peers Dollar Tree and Dollar General (Figure 13, green line vs orange and blue lines).

Figure 13 Operating margin (trailing 12-month) vs peers

Created by author using public financial data

Share buybacks

During the fourth quarter and fiscal 2022, the Company repurchased a total of 2.1 million and 10.3 million shares of common stock, respectively, for an aggregate purchase price of $231 million in the quarter and $950 million for the fiscal year, i.e., average price of $92.23 per share (vs $104 now).

Since 2019, Ross has reduced the number of shares outstanding by 8.7%, i.e., each share now owns 9.5% more of the economics (Figure 15). It has $950M remaining in the re-purchase authorization, which it expects to be completed in 2023.

Figure 14 Shares outstanding (diluted)

Seeking Alpha

Figure 15 Revenues (TTM and two-year rolling) on a per-share basis

Created by author using public financial data

Return on tangible capital

Ross's EBITDA return on tangible capital was in excess of 50% and in-line with its discount retailer peers prior to the COVID-19 outbreak. While it has dropped over the last 3 years (Figure 16, blue line), I believe it will recover in the intermediate term as margins tick back up.

Figure 16 Return on tangible capital comparison vs peers

Created by author using public financial data

Valuations

Ross's earnings yield (the reciprocal of price-earnings) is approximately 4%, lower than Dollar General and Dollar Tree's, likely reflecting the expectation of a margin recovery.

Figure 17 Earnings yield valuation vs peers

Created by author using public financial and share price data

In summary

Over the last three years, Ross Stores was impacted by the COVID-19 shutdowns, rising inflation, as well as skyrocketing ocean container shipping, freight, and wage costs.

I believe the worst is over as the COVID health emergency has ended, more employees return to the office, container shipping costs fall to pre-COVID levels, and freight costs recede.

Even though retail wages continue to rise as the labor market remains tight, I believe margins will recover over the near- to intermediate-term.

My long-term investment thesis continues to hold up. As such, I rate Ross a hold.

For further details see:

Ross Stores: Recovery On The Way As The Worst Is Likely Over