ROST - Ross Stores: The Type Of Company That's Always A Buy

2024-01-17 05:43:56 ET

Summary

- Ross Stores presents a compelling investment opportunity as an off-price retailer with a well-established and successful business model.

- Acquiring discounted excess inventory and offering brand-name and designer merchandise at lower prices has resonated well with consumers, particularly younger consumers and those in lower-income demographics.

- With a wide geographical reach and a growing store count, Ross is poised to deliver continued expansion.

- Shares look attractive with potential for margin expansion, a robust balance sheet, and a reasonable valuation.

Company Overview

Ross Stores, Inc. (ROST) owns a chain of department stores that sell discounted products including apparel, accessories, home goods, and more through its banners "Ross Dress for Less" (1765 locations) and "dd's DISCOUNTS" (347 locations). Ross Dress for Less is the main brand with significantly more locations and more variety in its products whereas dd's DISCOUNTS is strategically positioned to be the company's more value-oriented option for consumers.

Ross Stores' business model essentially involves purchasing excess inventory at big discounts from brand manufacturers or retail locations (as a result of overproduction, weak sales, closeouts, canceled orders, overruns, or simply Ross being another channel to moves goods through) and selling them at a reasonable mark-up to the end consumer.

Manufacturers and retailers love the model as they can get rid of inventory that didn't sell and consumers love it because they can benefit from the savings as they get brand-new merchandise at decent discounts off of the retail price.

Investment Thesis

As an off-price retailer, Ross Stores can sell brand-name and designer merchandise (products recognizable and well-known by the average consumer) and price them lower than what a traditional department store might sell them for. In my view, this is significant as U.S. census data shows that half of Americans are considered poor or lower-income. With poverty rates climbing from 7.8% in 2017 to 12.4% in 2022, more and more consumers are looking for cheaper places to shop without compromising on their lifestyle. In addition, despite inflation on the rise, consumers still want discretionary items, just at cheaper prices . Providing value to the customer isn't just about cheaper items, but also great quality, desirable brands, and merchandise that customers want to buy.

Resonating With Younger Consumers

While Ross Stores' typical customer is middle-aged females, in recent years, it began developing more interest from younger consumers. In recent years, the company has been able to attract a substantial new number of Gen Y and Gen Z customers who align with Ross' value proposition.

This is significant because when we consider what demographics will look like five or ten years out, its younger shoppers who will be spending more, and so it's that future spend that translates to higher sales growth for Ross Stores.

We are also seeing similar trends at its competitors as well. In the case of TJX (TJX), one of Ross Stores' competitors, the company saw a big bump in sales year over year in its recent quarter with sales growth of 8% year over year as a result of younger shoppers making up a larger percentage of the demographics.

Growing Store Count

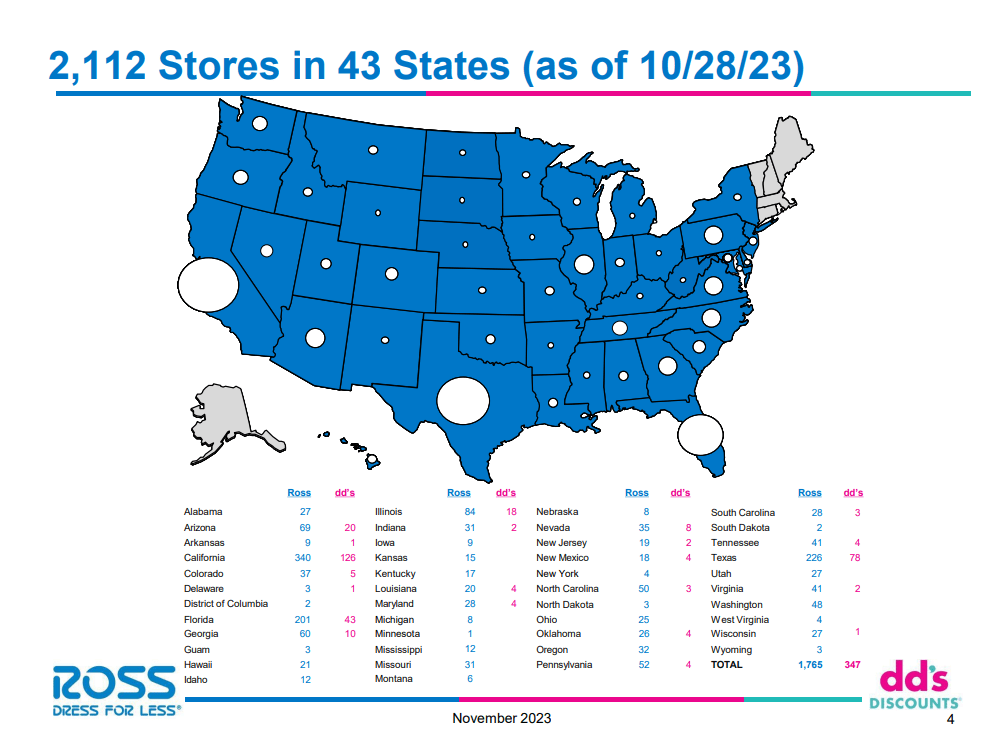

Ross has a wide geographical reach in 43 out of 50 U.S. states as of quarter end. With 2112 stores throughout the U.S., we can see from the chart below that its locations are pretty spread out with a larger presence in the 3 largest states by population: California, Texas, and Florida. As there are clearly pockets on this map where Ross doesn't have a large presence, I believe there's room to continue expanding for the company.

Geographical Reach (Investor Presentation)

{kind=link}

On the company's earnings call for the quarter, management discussed how there continues to be opportunities to grow the company's geographical reach and expand their value proposition to new markets.

During the quarter, as part of the company's expansion program, Ross Stores added 43 Ross Dress for Less locations and 8 dd's DISCOUNTS stores which brings the year to date total 72 Ross Dress for Less locations and 25 dd's DISCOUNTS stores. With a net increase of 94 stores, this represents an overall store count increase of about 4.5% blended between the two banners.

While management doesn't provide guidance on store count growth, we can observe that the net increase of 94 stores is higher than the six-year average net new store annual increase of 80 stores, highlighting that the growth is still there even as Ross gets larger.

Resilient to Online Disruption

According to IBIS World, Ross Stores has about 30% market share in the U.S. for off-price retailing and is the second-largest player in the space. With mid-single digit growth in net new store counts, Ross is outpacing its competition and has remained resilient to disruptions from online channels.

In my view, because of the wide assortment of goods that consistently gets updated for customers to find bargains, Ross stands out as a leader in the space due to its growth rate which is supported by its business model with good inventory management and strong supplier relationships.

With the rise of online shopping and ecommerce, one may be quick to rule out large department stores and brick-and-mortar type businesses. But in the case of Ross Stores, I don't view this to be the case.

Because Ross sells discounted inventory that brands don't want anymore, they're unlikely to want to see those products pop-up for sale in highly-visible omnichannel platforms. So by having them in physical stores instead, brands can better protect their brand image and stay tight on their brand equity to avoid being characterized as 'lesser' or 'cheaper' brands. With inventory dispersed across thousands of its locations, Ross is very resilient to online shopping trends as an off-price retailer.

In my view, with a net new store increase of around 94 this quarter, or about 5% growth, it wouldn't be far-fetched to think Ross can grow about 10% a year if there able to grow in-store sales 5% a year as well.

Improving Margins

The next part of my thesis is about improving margins at the company. In the last 10 years, according to S&P Capital IQ, Ross Stores has maintained very consistent gross profit margins in the 30-33% range and EBITDA margins in the 12-17% range (excluding 2021 as an anomaly year when margins were 4.4%).

While we're currently at the lower end of the historical EBITDA range, I believe there's room for Ross to expand margins back to the top of their historical range as margins have been pressured over the last few quarters due to freight headwinds and higher labor costs from weak comparable sales in 2022.

Given that management views these more as short-term headwinds, and freight headwinds have already started to abate, I believe we can expect to see around 300 bps of margin expansion, which would put as at the midpoint of the historical EBITDA margin range.

Strong Balance Sheet

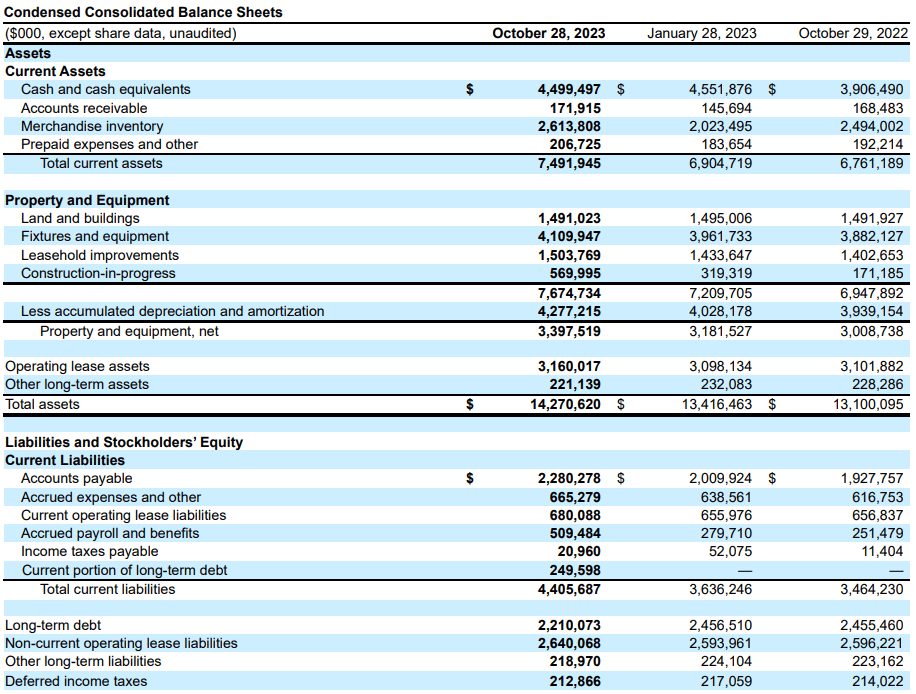

Ross Stores has a great balance sheet . With a cash position of $4.5 billion partially offsetting $2.2 billion of long-term debt, the company has a net cash position with a Total Debt to EBITDA ratio of 0.9x. With consistently high returns on equity over 30% over the last decade, this is all the more impressive. It also shows that management isn't willing to take on unnecessary debt just to prop up EPS short-term to his bonus targets. So all in all, the management at Ross Stores takes a very disciplined and conservative approach to maintaining the company's balance sheet.

Balance Sheet (Company Filings)

{kind=link}

Valuation

Based on the 20 sell-side analysts who cover the stock, the average one-year target price is $140.29, with a high estimate of $160.00 and a low estimate of $112.00. From the current price to the average price target twelve-months out, this implies about 2.7% upside for the stock, suggesting analysts see little upside for Ross Stores' stock near term and that the company is likely fully priced.

However, when we zoom out, Ross has been able to compound revenues and EBITDA at a 6.8% and 5.0% CAGR over the last decade, respectively, and 8.7% and 9.6% CAGRs over the last 20 years. It shows up in its fantastic price performance too, outpacing the S&P500's ten-year total return of 158.8% with a total return of 275.4%

Ross' stock isn't particularly expensive either. Ignoring the 2021 period when the multiple climbed high as a result of depressed EBITDA, the EV/EBTIDA multiple of 16x earnings doesn't look too expensive compared to the historical range. Compared to TJX at 12.0x EBITDA, one might be quick to conclude that Ross is the more expensive of the two. But on a free cash flow basis, Ross is cheaper at 22.3x FCF by about 5 turns compared to TJX. And given that Ross has grown faster and has a much better balance sheet, I think Ross is the way to go here.

Risks

In terms of the risk to the investment thesis here, the primary one would be if big brands decided to stop discounting their merchandise and selling excess inventory to off-price retailers like Ross (in an effort to enhance their brand image). While this has been a risk for years, and some brands have indicated that they wanted to do so, that hasn't materialized meaningfully for Ross as I think the sales channels are just too attractive to give up for some brands and manufacturers.

The next risk would be that Ross' growth rate is slowing down. With over 2100 stores, it's now got a presence in most states. That said, I'm still confident in the company's growth rate to grow above GDP (5% from store growth plus 5% from in-store organic growth), not to mention that there is likely to be further margin expansion as temporary headwinds from freight lift. So while growth may be slowing, the story isn't over yet for Ross Stores which has a commanding and growing market share of 30% in the industry.

Conclusion

In summary, Ross Stores presents a compelling investment opportunity as an off-price retailer with a well-established and successful business model. The company's strategic approach of acquiring discounted excess inventory and offering brand-name and designer merchandise at lower prices has resonated well with consumers, particularly younger consumers and those in lower-income demographics. With a wide geographical reach and a growing store count, Ross is poised to deliver continued expansion. In my view, the company has demonstrated that it is resilient to online disruptions, maintaining a strong market share in off-price retailing. Furthermore, I view the story compelling due to potential for margin expansion, a robust balance sheet, and a reasonable valuation. While risks such as potential changes in brand discounting strategies and slowing growth exist, the overall outlook for Ross Stores appears promising. As such, I rate shares as a buy today.

For further details see:

Ross Stores: The Type Of Company That's Always A Buy