RPAR - RPAR: Still Too Soon To Buy Despite Higher Interest Rates

2023-09-11 09:21:53 ET

Summary

- RPAR ETF aims to generate positive returns during economic growth, preserve capital during economic contraction, and preserve real rates of return during inflation.

- Diversification and rebalancing boost are key factors in achieving equity-like returns with less risk.

- RPAR has underperformed expectations due to the higher correlation of commodity producer stocks with both equities and gold, and poor bond performance.

The RPAR Risk Parity ETF ( RPAR ) was very ambitious at the start:

- generate positive returns during periods of economic growth,

- preserve capital during periods of economic contraction, and

- preserve real rates of return during periods of heightened inflation.

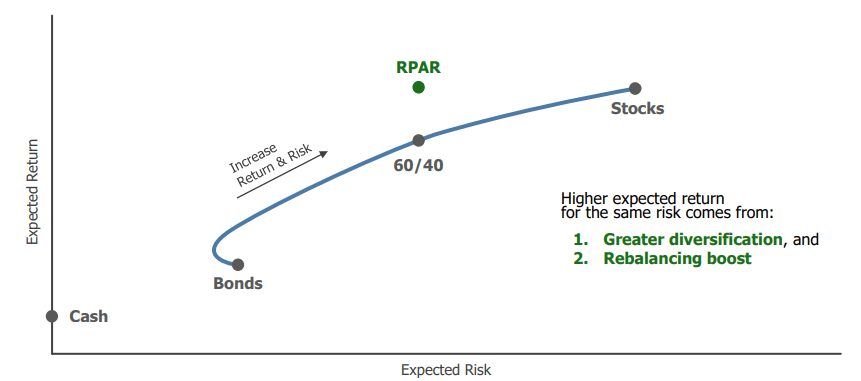

In short: equity-like return with less risk over the long run

{kind=link}

Greater diversification and a rebalancing boost would lead to the equity-like return with less risk.

RPAR thus far failed to live up to the expectations. We’ll try to explain why and look at what might come next.

Diversification and rebalancing boost

Let’s first take a look at the diversification.

The Risk Parity ETF is managed by Evoke Advisors. Co-CIO is Damien Bisserier who spent nearly a decade at Bridgewater Associates and hence knows the ins and outs of risk parity portfolios.

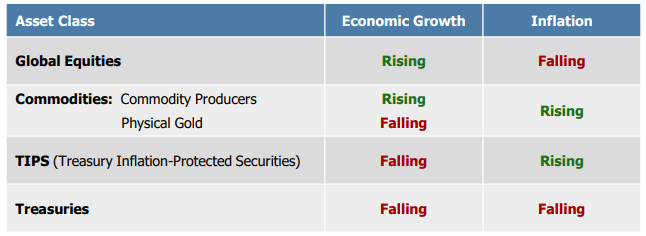

Traditional 60/40 portfolio invests 60% in stocks and 40% in bonds. When you look at the volatility of such a portfolio something like 90% of the portfolio’s risk is due to the stocks. A risk parity portfolio looks first at the risk allocation and the final asset allocation is the result of this equally weighted risk allocation.

RPAR e.g. divides the risk allocation equally to stocks, bonds, TIPS and commodities.

Figure 2: Risk allocation (Evoke Advisors)

This results in the below asset allocation.

Figure 3: Asset allocation (Evoke Advisors)

Since stocks are more volatile than bonds, they receive a smaller percentage of the ETF’s asset allocation, even though they account for 25% of its risk allocation. Treasuries and TIPS account both for 35% of the portfolio, stocks and commodities are each 25%—for a total of 120%. The total is bigger than 100% because risk parity funds use leverage to equalize the volatility levels between asset classes.

Figure 4: Asset allocation (Evoke Advisors)

But are we really talking about an evenly split risk allocation? Are stocks of commodity producers part of the commodity allocation or the equity allocation?

{kind=link}

The correlation between stocks of commodity producers and the S&P 500 (0.68) is certainly bigger than the correlation between commodities and equities (0.47).

The correlation between stocks of commodity producers and gold (0.28) is also bigger than the correlation between commodities and gold (-0.04).

Figure 6: Correlations (Portfolio Visualizer)

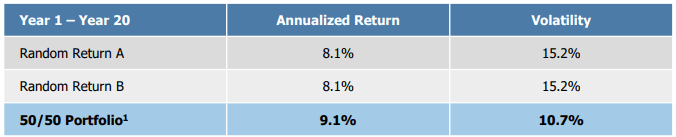

Regular rebalancing can “boost” returns without increasing risk. This boost is greater the lower the correlation among asset classes and the greater the volatility of each asset class.

Evoke provides an example to illustrate the rebalancing boost. Suppose you have a 2 asset portfolio that allocates 50% to asset A and 50% to asset B, which are uncorrelated to one another. Both assets average the exact same return and risk but with annual rebalancing, the return of the portfolio after 20 years is approximately 1% higher than the average return of the assets (9% vs. 8%), with a lower volatility. Higher returns with lower volatility indeed.

{kind=link}

But due to the higher correlation of commodity producer stocks with both equities and gold, the rebalancing boost has been smaller than expected.

Rising real rates

Rising real interest rates are another reason for RPAR’s poor performance so far. RPAR started at the end of 2019, when real rates were even negative!

{kind=link}

Since then real rates have normalised but this rise in real rates had of course a negative impact on TIPS. Rising real rates accompanied of course also a rise in nominal rates which had a negative impact on the treasuries in RPAR’s portfolio.

Nominal rates rose the past year almost 1% from 3.29% to 4.27%. Nominal yields are the sum of real rates and inflation expectations. The latter were almost stable the past twelve months, so the rise in nominal yields was completely due to rising real rates.

Figure 9: Treasury yields (Radar Insights)

Figure 9: Treasury yields Radar Insights

Rising yields have also a negative impact on gold. Gold has no yield and higher bond yields make it less attractive.

All-in-all, since inception, equities, including those of commodity producers, and gold have contributed positively to RPAR’s return, while bonds, both treasuries and TIPS, had a negative contribution.

Figure 10: Return attribution (Evoke Advisors)

Given the fact that treasuries and TIPS are “overweight” in a risk-parity portfolio, this bad bond performance drags down RPAR’s performance.

{kind=link}

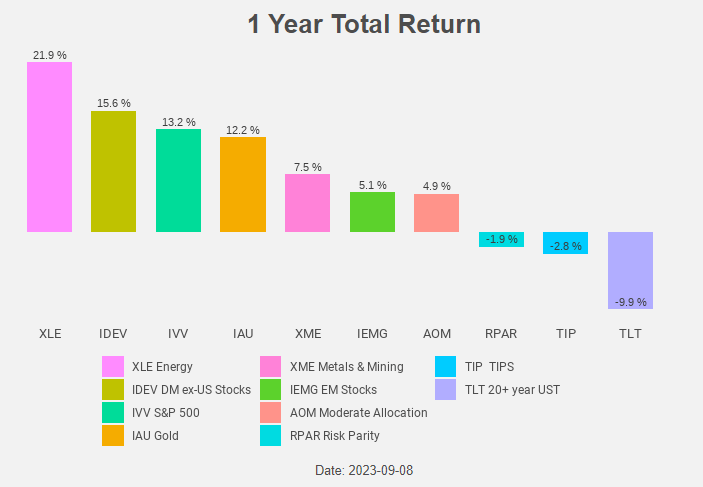

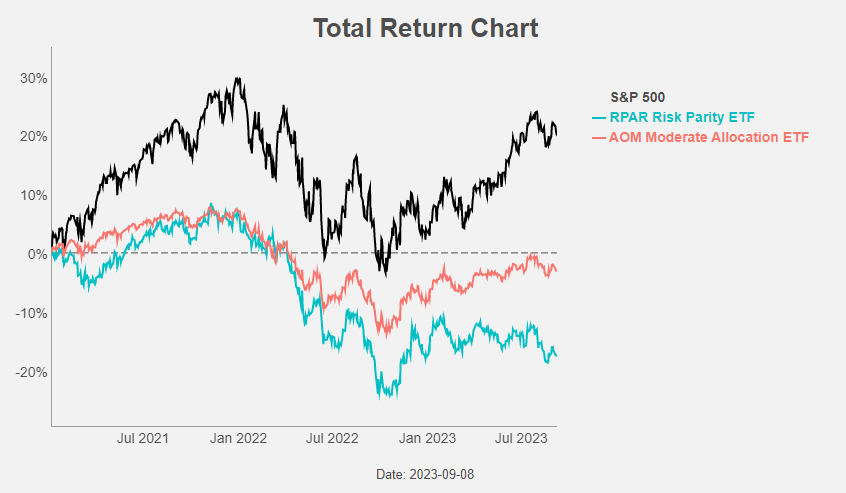

RPAR even underperforms the iShares Core Moderate Allocation ETF ( AOM ), a 60/40 portfolio.

{kind=link}

The net expense ratio is 0.50% and the dividend yield is 3.22%.

What’s next?

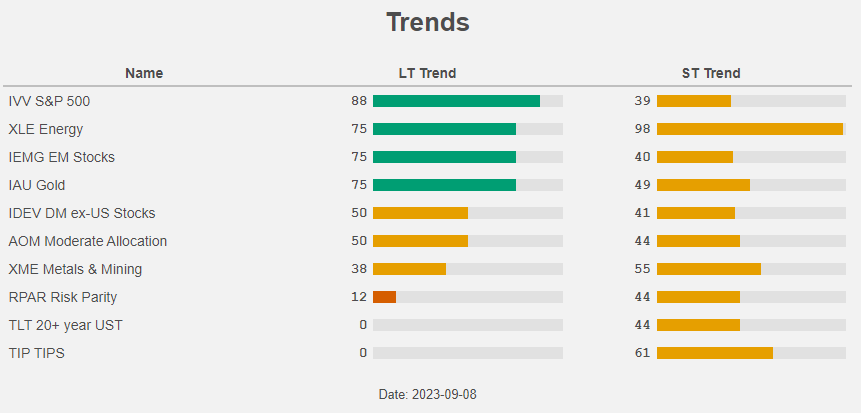

When we take a look at the long term trends, we can see that Treasuries and TIPS are in a long term down trend. This is also the case for RPAR itself.

{kind=link}

Nevertheless, the long-term expected return of a risk parity portfolio like RPAR is materially higher now due to significantly higher interest rates.

Higher rates also increase the odds of lower rates which would positively impact Treasuries, TIPS and gold. Rates could drop if the long expected recession effectively would arrive. A recession would of course be bad for equities in general and equities of commodity producers in general.

The current bad performance of risk parity portfolios is reminiscent of the Volcker-tightening period in the 80’s. When that tightening ended, the performance improved markedly.

Figure 14: Performance in Volcker tightening (Evoke Advisors)

This might happen again when the Powell tightening is over. The question is now: when will the Fed end the rate hikes?

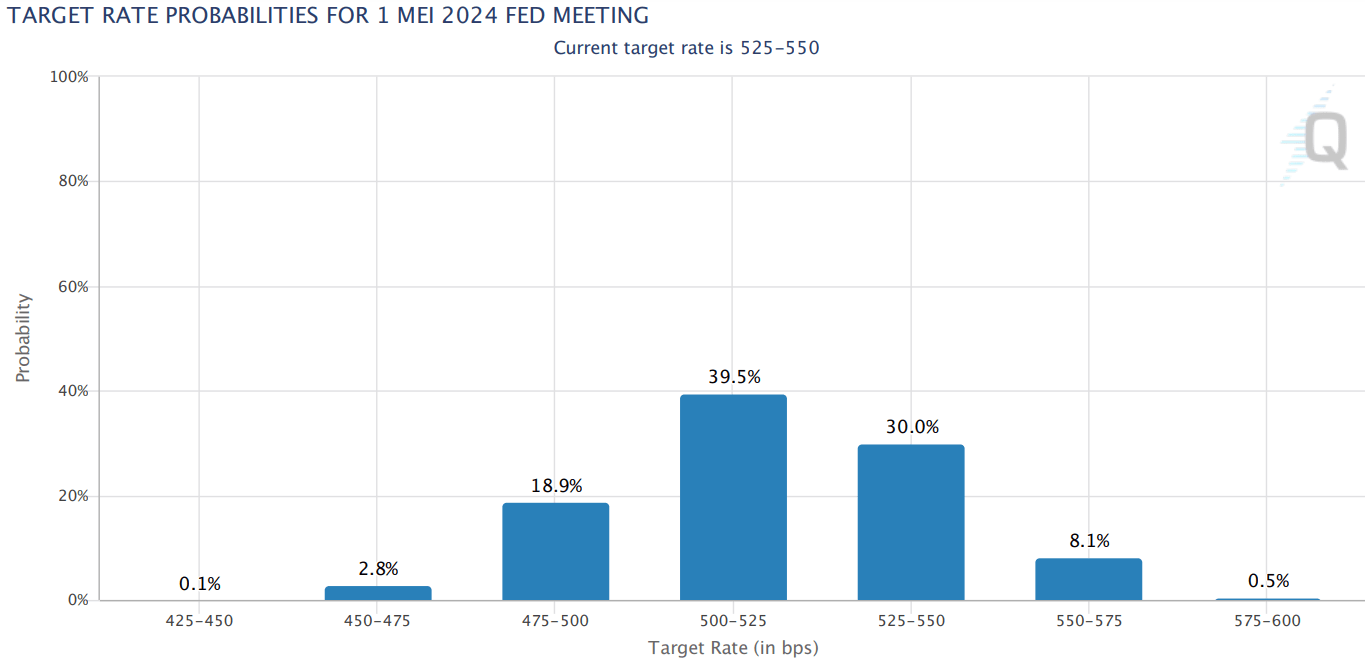

The peak rate that can be deducted from the Fed funds futures is the current rate .

The first change that can be deducted from the Fed-futures is a rate cut in May 2024.

Figure 15: FOMC May 2024 target rate probabilities (CME Group)

{kind=link}

On the other hand, while inflation has cooled the last months, a new rise in inflation figures the coming years cannot be excluded. If the current inflation cycle keeps following the path of the inflation cycle in the 70’s…

Figure 16: Inflation cycles (Bloomberg)

Maybe the best outcome might be to avoid a recession altogether. This way equities and commodities will not fall as they use to do in a recession and yields can remain at the current level, offering a nice coupon.

Conclusion

The long-term expected return of a risk parity portfolios like RPAR is materially higher now due to significantly higher interest rates. Real and nominal rates have never been higher since the inception of RPAR at the end of 2019.

Due to the rising rates, Treasuries and TIPS are in still a long term down trend. This is also the case for RPAR itself. So while we think RPAR is certainly an improvement compared to a traditional 60/40 portfolio, we aren’t buyers as long as the long term trend remains down.

For further details see:

RPAR: Still Too Soon To Buy Despite Higher Interest Rates