RPAR - RPAR: Use Upcoming Rally To Reassess (Rating Downgrade)

2023-11-30 18:14:50 ET

Summary

- RPAR Risk Parity ETF's heavy fixed-income allocations have acted as a headwind, causing the fund to underperform.

- Looking forward, I worry the fund's allocation strategy may be based on historical data since 2000 that is biased towards bonds.

- However, I believe there are structural reasons inflation and interest rates will be secularly higher in the coming years, which would prove to be detrimental to RPAR.

- I recommend investors take any upcoming rallies to reassess whether RPAR should be in their portfolios.

Back in the spring, I wrote a bullish article on the RPAR Risk Parity ETF ( RPAR ), noting that the RPAR ETF should do well if my thesis was correct and the U.S. economy were to fall into a recession/stagflation, then expectations for interest rate cuts would build, which should benefit the fund's heavy fixed income allocations.

However, I also noted that the key risk for the fund was if the economy 'muddles through' and the Federal Reserve stuck to its 'higher for longer' policies. If that were to happen, then RPAR's heavy fixed income allocations would act as a headwind and the fund would likely do poorly.

Unfortunately, my fears were realized as the U.S. economy shook off the SVB/regional bank crisis and reported a strong 4.9% YoY annualized GDP rate in the summer, defying my calls for economic weakness. The Fed was therefore able to maintain tight monetary policies, leading to weakness in bonds. The RPAR ETF declined by 6% as a result (Figure 1).

Figure 1 - RPAR declined by 6% since May (Seeking Alpha)

As we approach the end of 2023 and look forward to the new year, I wanted to take the opportunity to revisit my thesis on RPAR.

Brief Fund Overview

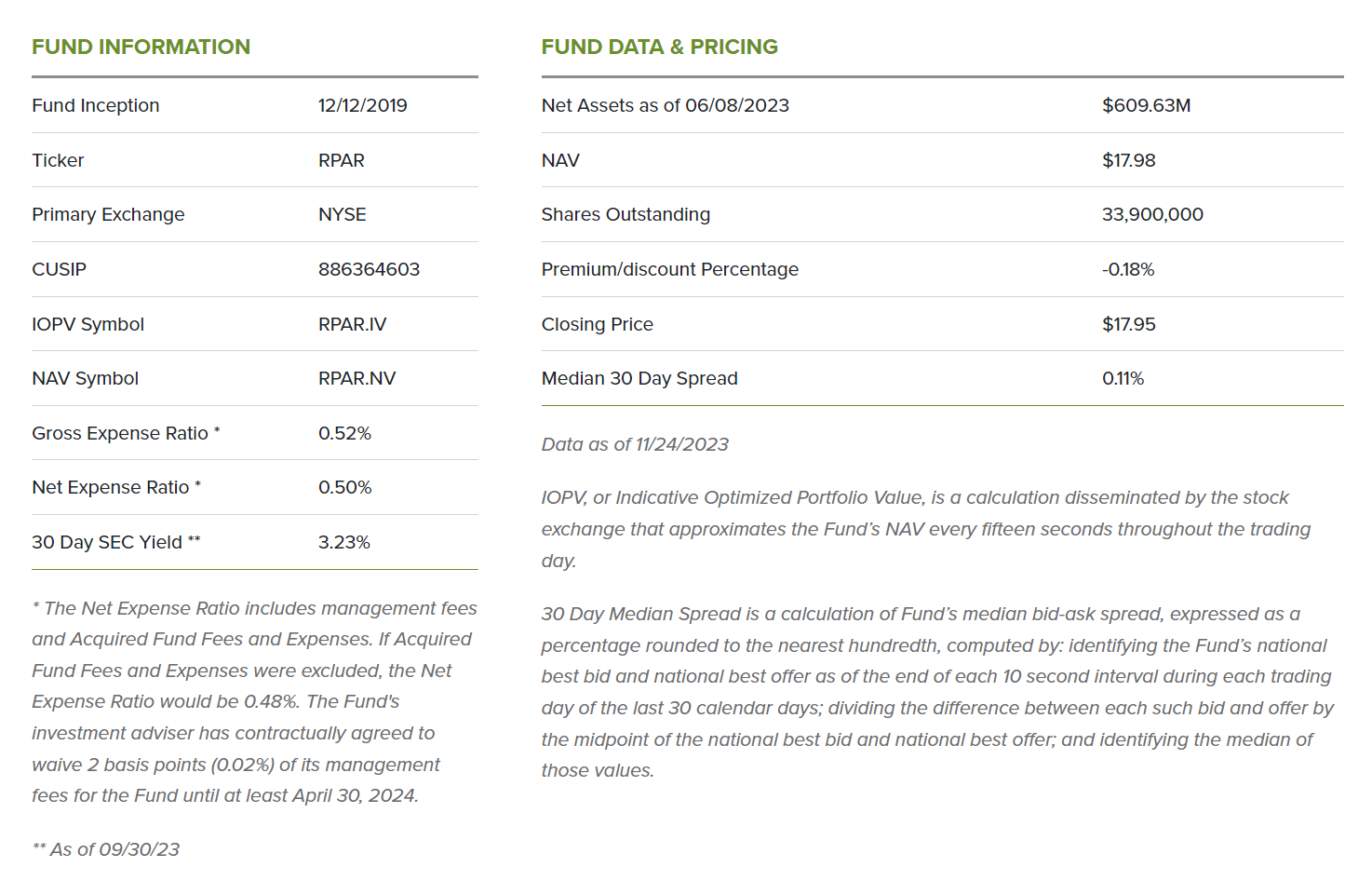

The RPAR Risk Parity ETF gives retail investors convenient access to risk-parity strategies in a liquid ETF structure. The RPAR ETF currently has over $600 million in assets and charges a 0.50% net expense ratio (Figure 2).

{kind=link}

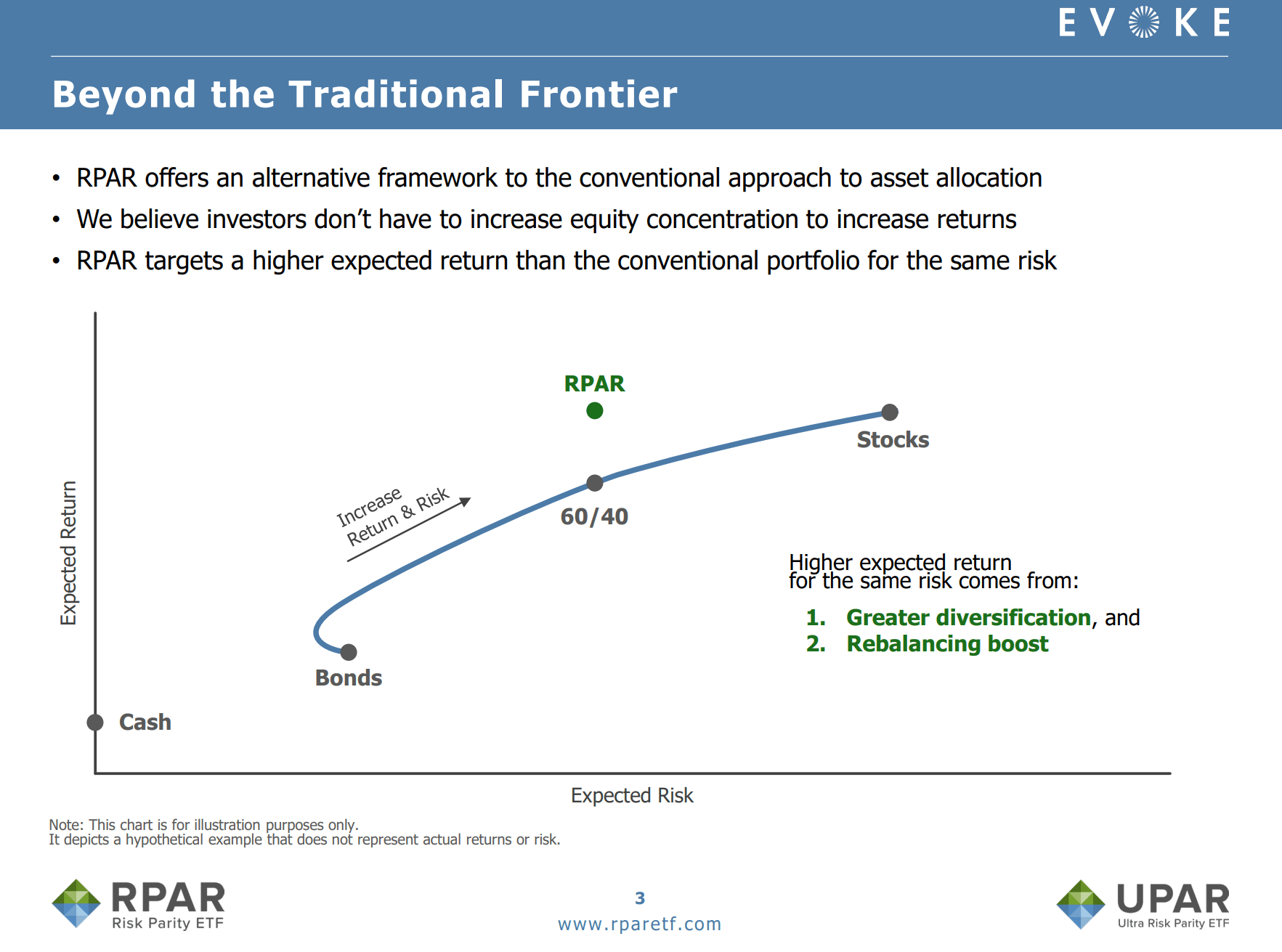

The basic concept of 'risk-parity' is to design a portfolio with various assets that will work in all economic scenarios. For example, the RPAR invests in 4 asset classes: Global Equities, Commodities, TIPS, Treasuries, that the manager believes will outperform a traditional 2 asset portfolio (Figure 3).

Figure 3 - Manager believes RPAR will outperform 2 asset portfolio (rparetf.com)

{kind=link}

Returns Have Been Disappointing

Unfortunately, with the passage of time, it increasingly appears that RPAR ETF has underperformed its mandate, as the RPAR ETF has delivered -1.1% average annual returns since inception to September 30, 2023, significantly trailing the 60/40 Portfolio at 3.7% and the MSCI World Index at 7.4% (Figure 4).

Figure 4 - RPAR has underperformed its mandate (rparetf.com)

{kind=link}

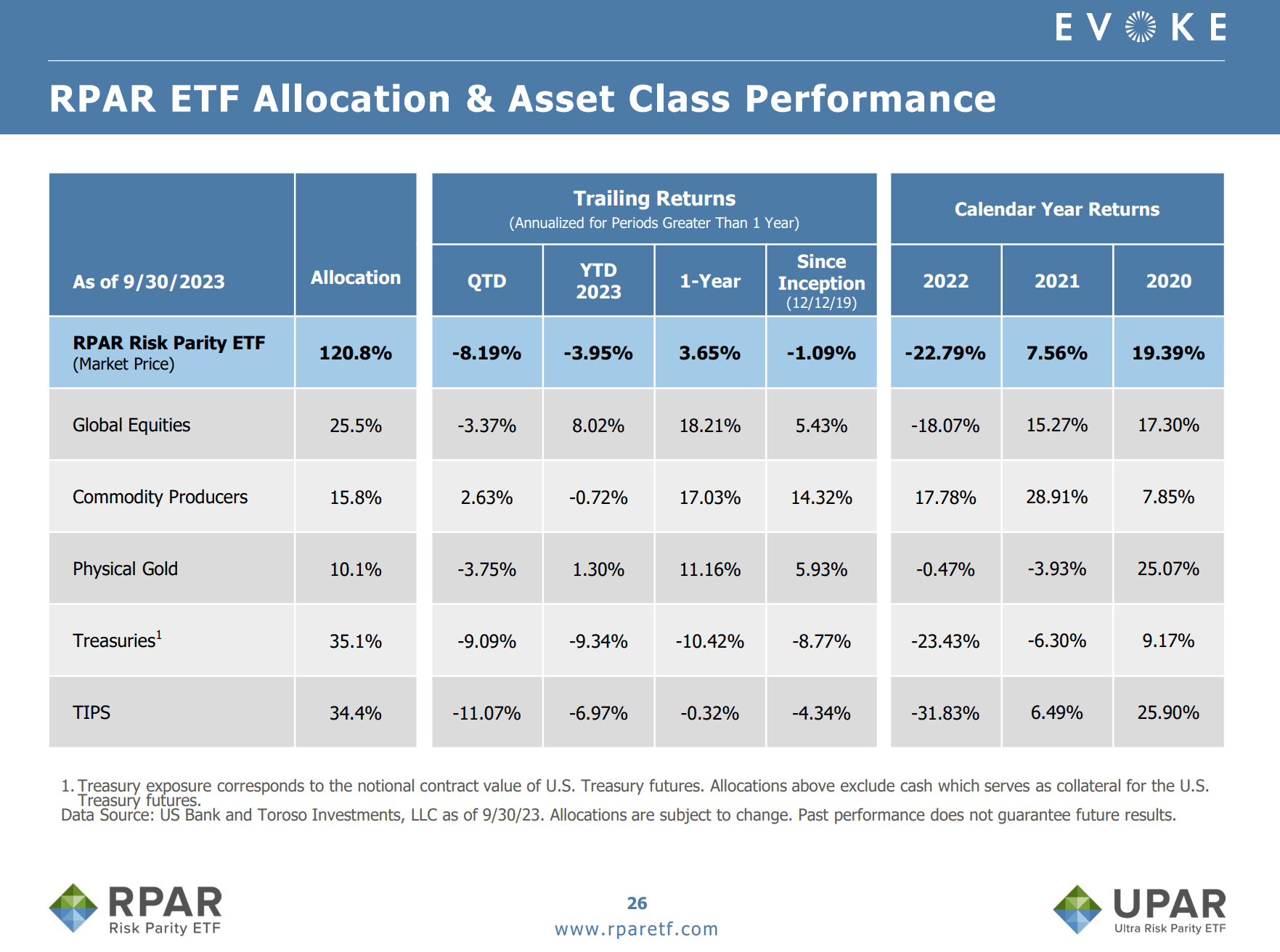

With the benefit of hindsight, RPAR's underperformance appear to be driven by the fund's heavy allocation to bonds that I have noted previously. For example, as of September 30, 2023, the RPAR ETF had a 35.1% allocation to Treasuries and a 34.4% allocation to TIPs (Figure 5).

Figure 5 - RPAR allocation as of September 30, 2023 (rparetf.com)

{kind=link}

Since the Fed began raising interest rates in 2022, both Treasuries and TIPS have suffered due to their duration exposures.

RPAR ETF Designed Using Post-2000 History

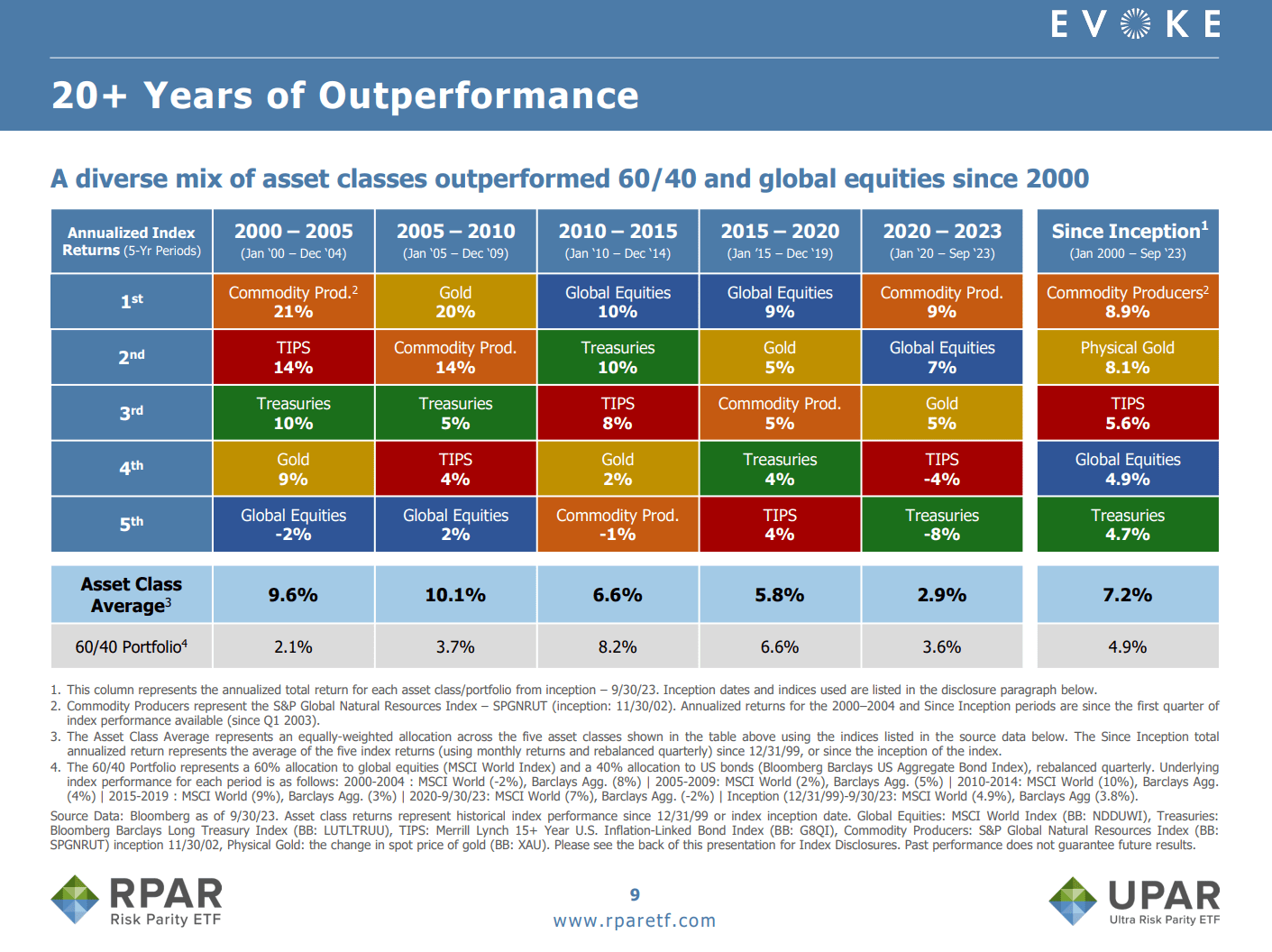

Thinking about the RPAR ETF's strategy, I believe there may be a flaw in the RPAR ETF's design that I have overlooked in my prior article. Specifically, while reviewing the RPAR's marketing documents, I noticed that the asset class allocations was based on the past 20 years of historical performance (Figure 6).

Figure 6 - RPAR design based on historical data post 2000 (rparetf.com)

{kind=link}

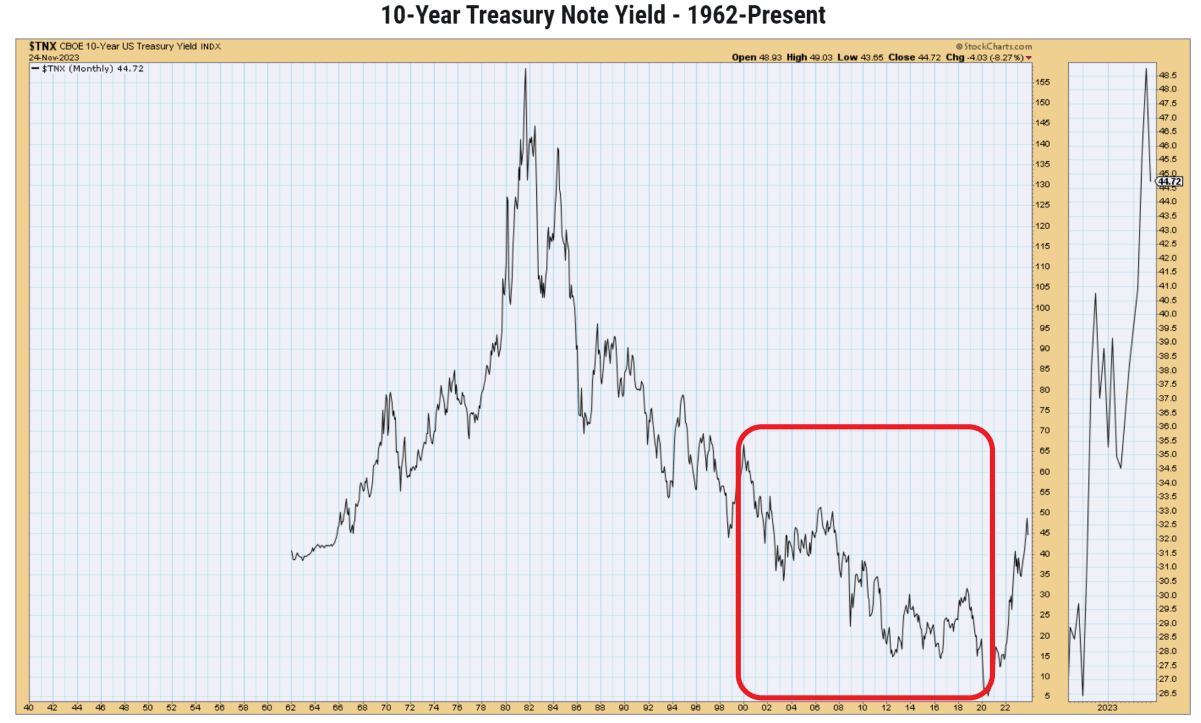

The problem is that the past 20 years have been characterized by a secular decline in interest rates, with 10 year treasury yields falling from over 6% to a low of less than 1% in 2020 (Figure 7).

Figure 7 - 2000s characterized by secular decline in interest rates (stockcharts.com)

{kind=link}

This secular decline in interest rates would have flattered any fixed income asset class, and may be the primary reason why the RPAR ETF was designed to hold such high allocations to bonds via a 35% target allocation to both treasuries and TIPs (Figure 8).

{kind=link}

In fact, if we zoom out and reconsider the macro regime we are currently in: the Federal Reserve raising interest rates to combat an inflation shock, the most analogous time period is the 1970s, when the western world suffered from an inflation spiral which ultimately required Paul Volcker to raise interest rates to 20% in 1981 to resolve.

Case For Secular Inflation

While headline CPI inflation has moderated in the past few quarters, one concern I have is that we currently have the conditions for secular inflation to persist for years to come. The biggest difference between now and the past 20 years is China and its role in the global economy.

In the early 2000s, China was just entering the WTO and the western world was able to enjoy the fruits of China's demographic dividend . China's one-child policy rapidly changed the age-structure of its population, creating a 1 billion strong labour force with low dependency ratios (Figure 9).

Figure 9 - China's working age population peaked at 1 billion (china.unfpa.org)

To keep its giant work force occupied and content, China opened up its economy and became the world's factory, manufacturing everything from t-shirts to iPhones. This exported deflation globally.

However, as we enter the 2020s, China's demographic dividend is about to reverse as China's population ages. According to the UN , China's working age population has already peaked and is going to decline swiftly in the coming decades (Figure ).

Figure 10 - But Chinese workforce is starting to decline (population.un.org)

Furthermore, the western world saw first-hand the weakness of 'just in time' manufacturing practices during the COVID pandemic, with many key goods like microchips unavailable as China locked down and supply chains were disrupted. Therefore, many companies have chosen to re-shore their manufacturing back to North America or to other Asian countries like Vietnam and India. While building redundancies and shortening supply chains is good for product availability, it will inevitably raise prices and lead to inflation.

Finally, the growing geopolitical divide between the U.S. and China is causing friction and increased costs. Although President Trump was the one who introduced tariffs on Chinese-made goods and initiated a trade war, President Biden has maintained many of these tariffs and in some cases, like semiconductors, have even escalated the trade war.

Throw in hot wars in Ukraine and the Middle East and it is not difficult to imagine oil embargoes at some point in the future that could send energy prices skyrocketing and boosting inflation.

In a world of secular inflation, I believe interest rates will be structurally higher and may act as a headwind for fixed income investments.

Cyclical Interest Rates May Have Peaked

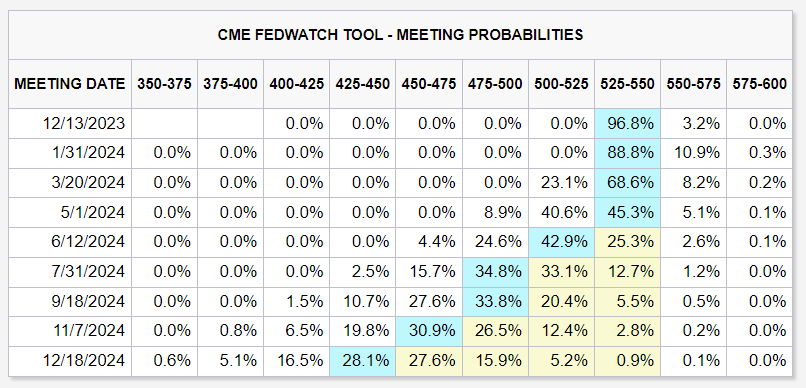

However, cyclically, short-term interest rates may have peaked as the Federal Reserve has paused its Fed Funds rate at the current level for several FOMC meetings as it seeks to fine tune monetary policies.

In fact, traders broadly expect the Federal Reserve to start cutting interest rates in mid-2024 and with cuts of almost 100 bps by the end of the year (Figure 11).

{kind=link}

So in the short- to medium-term, bonds should see some relief in 2024 and my outlook for the RPAR ETF continues to be constructive.

However, given my longer-term concerns regarding secular inflation and structurally higher interest rates, I recommend investors take the opportunity to seek alternative investments with less duration risk.

Conclusion

The RPAR ETF gives investors a convenient vehicle to invest in risk-parity strategies. The RPAR ETF invests in a portfolio of asset classes that it believes will deliver strong performance across all market environments.

However, when analyzing the strategy's allocation, the RPAR ETF does have unusually high allocations to fixed income (70% of net exposure). This could be driven by the strategy's lookback from the past 20 years. Unfortunately, I worry the upcoming decade could be characterized by secular inflation and structurally higher interest rates, which may prove to be a headwind for RPAR's allocation strategy.

I recommend investors take the upcoming cyclical rally in bonds to reassess whether the RPAR should fit in their portfolio. I rate the RPAR ETF a hold .

For further details see:

RPAR: Use Upcoming Rally To Reassess (Rating Downgrade)