RPT - RPT Realty: Underwhelming 2023 Guidance

Summary

- RPT Realty has an interest in a national portfolio of open-air shopping centers, located primarily in the top MSAs in the U.S.

- Their tenants include large national retailers, as well as smaller local tenants.

- The company is fresh off their most recent earnings release relating to the full 2022 fiscal year. And while leasing figures impressed, forward guidance appears underwhelming.

- Though shares are attractively priced at about 10.9x forward FFO, investors are unlikely to realize meaningful upside in the near to medium term.

RPT Realty ( RPT ) owns and operates a national portfolio of open-air shopping destinations, located principally in the top 40 metropolitan statistical areas (“MSAs”). Some top individual markets representing more than 10% of annualized base rents (“ABR”) include Detroit (12.9%), Boston (11.5%), and Cincinnati (10.1%).

Their top tenants include The TJX Companies ( TJX ) and DICK'S Sporting Goods ( DKS ), among others. And these two are the only ones that represented over 2.5% of ABR at the end of fiscal 2022. Similar to other shopping center-focused REITs, RPT also has its share of exposure to weaker tenants, such as Bed Bath & Beyond ( BBBY ).

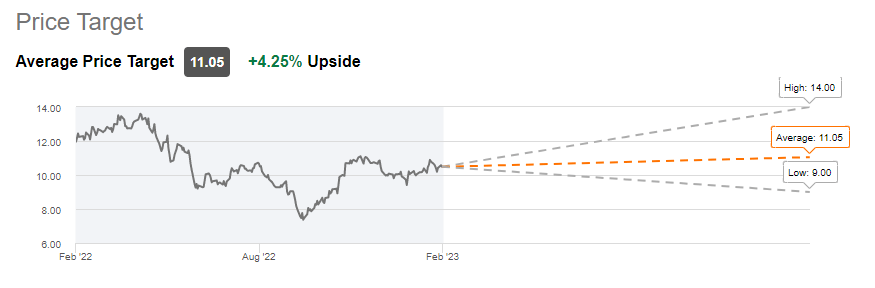

Currently, shares are up about 5% YTD but are still down over 15% over the past year. The stock is lightly covered by Seeking Alpha (“SA”) authors and Wall Street alike, but those covering the stock in recent periods tend to be neutral to bullish, with the SA community generally bullish. Wall Street, on the other hand, view shares more neutrally.

{kind=link}

Seeking Alpha - RPT Average Wall Street Analyst Price Target

Currently, shares are fresh off their Q4FY22 earnings release. While there were positive takeaways in their leasing activity, forward guidance appears underwhelming. Even though shares are attractively priced at a multiple of 10.9x, with the possibility of further dividend growth, the stock is unlikely to provide meaningful shareholder returns in the coming periods.

Recent Performance and Current Portfolio Metrics

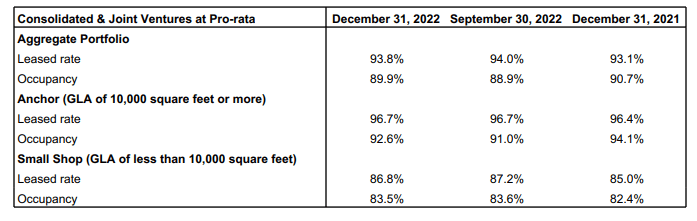

As of December 31, 2022, RPT’s total portfolio was 93.8% leased. While this is up 70 basis points (“bps”) from last year, it’s slightly down on a sequential basis, at 20bps. This, however, is on higher physical occupancy levels of 89.9%. This is up 100bps from last quarter.

{kind=link}

Q4FY22 Investor Supplement - Summary Of Portfolio Occupancy By Quarter

Though the pipeline of pending commencements is lower in the current quarter, at 390bps, from 510bps last quarter, the pipeline is still significant. Overall, the total pipeline, in addition to recovery income, amounted to +$11.2M. This is over 7% of their net base rents earned in 2022.

During the quarter, RPT signed 503K SF of space at spreads of 5.6% on comparable renewals and 24.3% on new signings. This brought their full year total up to 2.2M, which is their highest leasing volume in nearly a decade. In addition, re-leasing spreads on new and renewal leases came in at 42.6% and 6.5%, respectively.

Higher base rents contributed in part to growth in same property net operating income (“NOI”) during Q4 of 1.1% compared to the same period last year. On a full year basis, same property NOI was up 4.3%. All considered, operating funds from operations (“FFO”) was little changed during the quarter but up about 9.4% YOY.

Looking ahead, management expects same property NOI growth between 1.5% to 3.25% in 2023. Weighing on growth are the effects of higher assumed bad debt expense and occupancy loss due to tenant bankruptcies. And given the current market environment, no multi-tenant acquisition or disposition activity is expected in 2023.

Liquidity and Debt Profile

At year end, RPT’s total leverage, as measured by their total net debt as a multiple of adjusted EBITDA, was 6.9x. When including their signed but not commenced pipeline (“SNO”) and recovery income balance, the ratio would be slightly lower, at 6.3x.

Though the company operates on a slightly higher multiple than their peers; Urstadt Biddle ( UBA ), for example, reported a multiple of just 3.6x at year end. The risks appear limited.

Presently, RPT remains in compliance with all their required covenants. And they also have ample cushion afforded to them. Interest coverage, as calculated through their covenant requirements, for example, stands at 4.1x. This is on a requirement of 1.75x.

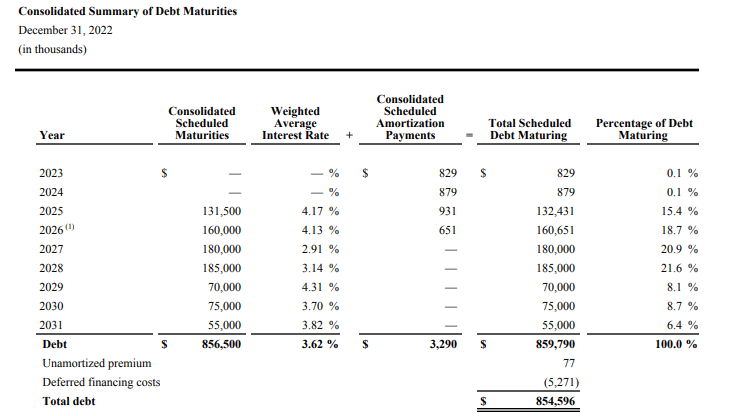

In addition, the company has no significant maturities until 2025 at the earliest. This was made possible by a recent repayment made in October of 2022.

{kind=link}

Q4FY22 Investor Supplement - Debt Maturity Schedule

On top of this, they have available liquidity of over +$450M, comprised of cash on hand and availability on their revolving credit facility. And if need be, they have access to about +$133M on their at-the-market equity distribution program (“ATM”). This is following their December settlement of 1.2M shares that were previously sold on a forward basis at a weighted share price of $13.85/share.

Dividend Safety

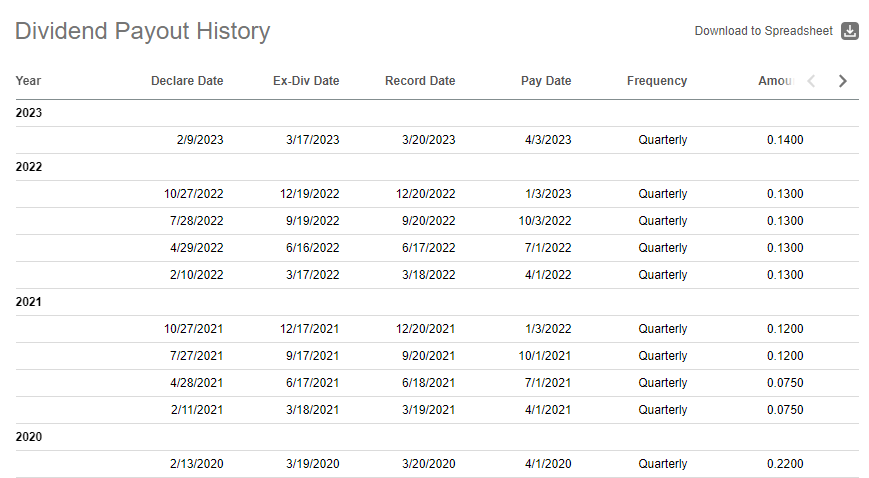

RPT recently increased their quarterly payout by 7.7% to $0.14/share. This follows an 8.3% increase at the beginning of 2022 and a 60% increase in 2021.

{kind=link}

Seeking Alpha - RPT Recent Dividend Payout History

The payout, however, is still nearly 60% below the rate provided in 2020 just prior to the COVID-19 pandemic. At that time on the payout date of 4/1/2020, the dividend yielded a forward 14.6% based on a closing price of $5.40/share.

{kind=link}

Seeking Alpha - Snapshot Of Historical Prices In April Of 2020

The cut then was likely justified, given the uncertainty. But the payout has made a steady run higher since then. This rise has also been in line with the share price. At current pricing, the new payout represents an annualized yield of 5.3%.

For investors, further hikes are likely in the periods ahead. During the quarter, RPT generated $0.24/share in FFO. The new payout, then, represents less than 60% of FFO. By contrast, at the end of 2019, the payout ratio for the year came in at 81.5%.

At an 80% payout level, the quarterly dividend would be just over $0.19/share. That represents over 35% upside from current rates. And assuming there is no movement on the stock price, the annualized yield on that would be over 7%.

Final Thoughts

In 2023, RPT is expecting full year FFO per diluted share to land between $0.97 to $1.01/share. This would be down about 5% from 2022’s reported figures on the low end of the range and slightly below on the top end. Contributing to the lower range is weakness in their same property portfolio, which is expected to see elevated bad debt expense and occupancy loss due to tenant bankruptcies.

In November of 2022, shares were downgraded by Credit Suisse on some of these expectations likely coming to fruition. But markets largely discounted the view, as shares have been generally trending higher since that downgrade. And even with the downgrade, shares are still estimated to be fairly valued at about $12/share. This would represent upside of about 13% from current trading levels.

In addition, the company has been steadily increasing their dividend payout to levels closer to where they were prior to the pandemic. At a payout ratio of less than 60%, the dividend still has ample capacity to be increased further. Should the quarterly rate return to its former levels, investors would receive a yield of over 7%. This would be in addition to the estimated upside embedded within the share price.

At 10.9x forward FFO, shares are attractively priced. And while the upside is there, the underwhelming guidance is disappointing. Sure, their portfolio remains well-anchored by quality tenants, with TJX Companies and DICK'S Sporting Goods together representing 8.7% of annualized base rents, but the near-term earnings hit from losses relating to Bed Bath & Beyond and other weaker tenants reduces the appeal of the stock.

For investors seeking entry, waiting another quarter or two to get a feel for how the portfolio shakes out likely wouldn’t result in missing out on any meaningful interim upside.

For further details see:

RPT Realty: Underwhelming 2023 Guidance