RQI - RQI: 8% Yield And A Nice Way To Play The Duration Exposure

2023-12-03 04:05:31 ET

Summary

- Commercial real estate has struggled since the Fed started increasing interest rates in 2022, but there are signs of material recovery.

- As the odds are becoming increasingly stacked in favour of experiencing rate cuts over the next year and further, the attractiveness of duration factor has increased.

- Considering RQI's exposure to commercial real estate equity, preferred and fixed income securities that are boosted by ~30% (of AuM) external leverage could provide outsized returns for investors.

Since the FED started increasing the level of interest rates in early 2022, the commercial real estate segment has experienced a rather volatile ride. Even before the FED decided to assume restrictive monetary policy, certain parts of the commercial real estate segment were already weakened due to the effects from COVID-19. For example, office, hotel and retail properties were under a notable trouble as the occupancy prospects had suddenly become unclear.

{kind=link}

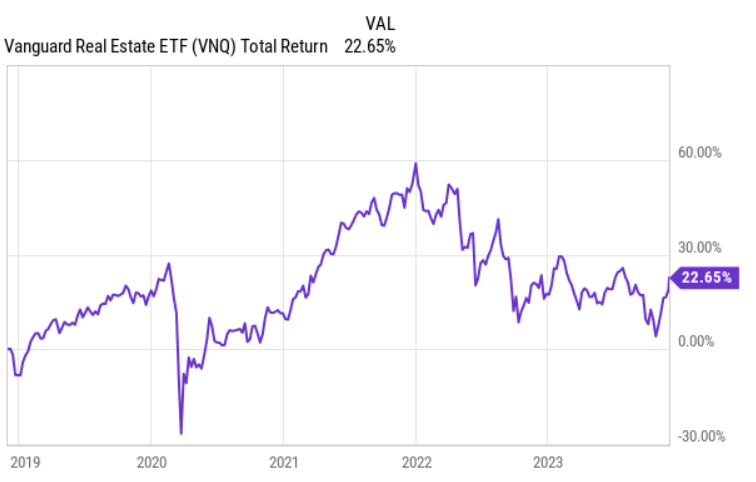

The chart above, which measures the total return performance of the Vanguard Real Estate Index Fund ETF Shares ( VNQ )

(i.e., index representing a broad spectrum of the U.S. equity REITs) clearly indicates that starting from 2022, the real estate as an asset class has struggled breaking the momentum that was associated with the recovery from the pandemic.

In other words, there has been a rather consistent decline underpinned with pronounced spikes in the underlying volatility.

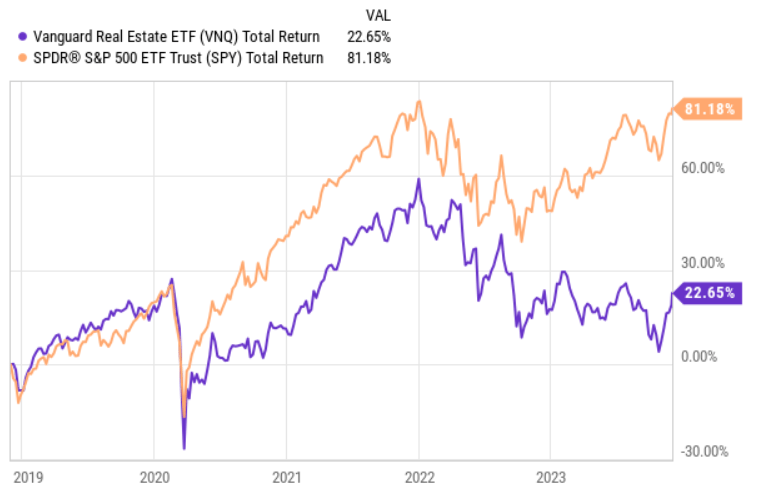

If we add the S&P 500 to the picture, it is quite evident that VNQ has lagged behind the market in a material manner.

{kind=link}

There are several reasons that explain this, but the key one is the inherent sensitivity of real estate to the changes in the interest rates. It is the elevated duration factor, which causes REITs to respond more to both cuts and increases of in the SOFR. So, it is only obvious that starting from 2022 REITs have considerably diverged from the S&P 500.

Yet, in over the past month, VNQ has finally outperformed the S&P 500 in a notable fashion, registering 14.1% gains (compared to 8.3% by the S&P 500). It has been the recalibration of market's expectations towards a more normalized SOFR level in the economy over the near future.

{kind=link}

Just as REITs had been facing headwinds stemming from more restrictive monetary policy since early 2022, now it seems that REITs are in a position to experience some tailwinds, which could contribute to a convergence to the S&P 500.

Thesis update for RQI

As a result, an exposure in the REIT segment that is heavily skewed towards duration factor has now become rather interesting for investors to play.

For this reason, the Cohen & Steers Quality Income Realty Fund ( RQI ) has caught my interest again. Approximately, half year ago I wrote an article on RQI indicating that the Fund could be an attractive vehicle for investors, who want to capture both high yielding dividend and the exposure on duration factor via real estate segment.

Since then, RQI has registered total returns of ~8% beating VNQ by ~200 basis points.

At the same time, I also indicated a potential risk that would come from additional leverage that RQI uses to magnify the returns of the underlying portfolio. My concern was that RQI's weighted average interest rate yielding ~2.6% that is associated with the ~30% (of total assets) external leverage position was locked in for relatively short time period (i.e., slightly below 3 years). So, for instance, if the interest rates stayed higher for longer or even worse continued to surge higher, RQI would be forced to gradually recognize higher interest rate costs that would eventually make the dividend coverage unsustainable; especially considering the fact that one third of RQI's AuM is explained by the external leverage.

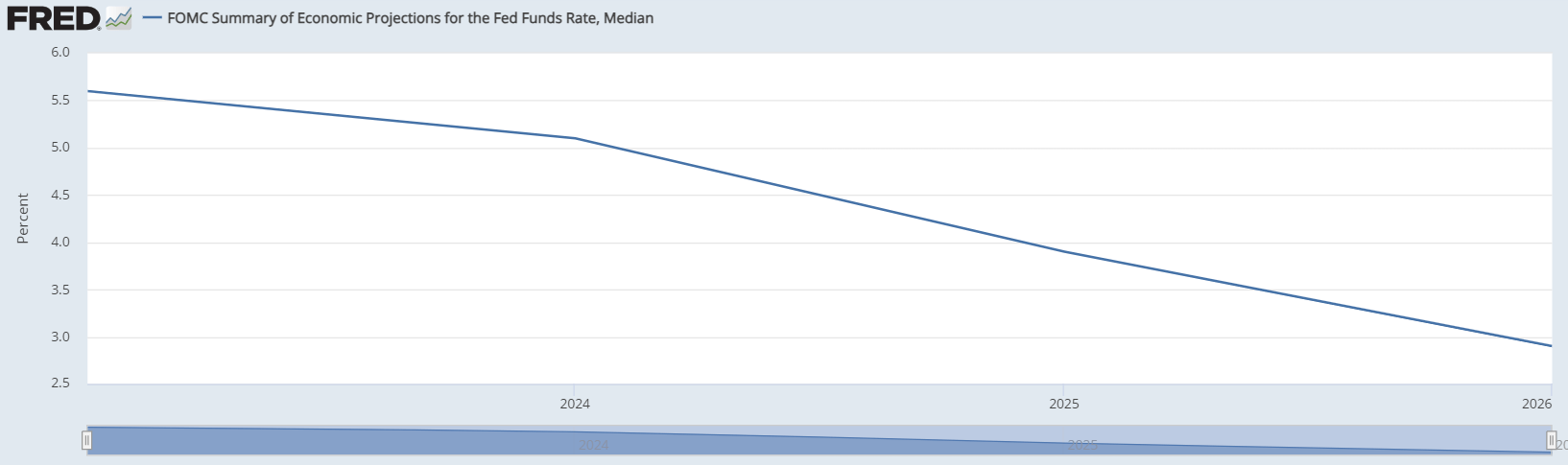

Now, however, the probability of experiencing further interest rate hikes seems to be very distant. There is no serious chatter around suffering from additional increases in the SOFR, and instead the market (including the FED) has increasingly focusing on solving the mystery of the duration of the prevailing restrictive interest rate policy.

By looking at the FOMC's chart above, we can see that the market is pricing in rate cuts already this year and more tangible ones in 2024.

Granted, these are only expectations that, in fact, typically do not materialize just as predicted. Nevertheless, in my view, the odds are clearly stacked in favour of interest rate cuts before RQI has to rollover its external debt load.

Factsheet as of September 30, 2023

While we have established that it is highly unlikely that RQI would have to refinance its debt at dramatically higher interest rates, there is the variable debt portion accounting for 19% of the total financing that should render an immediate impact on RQI's cash flows when the rates tick lower.

Namely, the current trajectory of the interest rates should not only relax the concerns of painful refinancings, but also provide a direct positive impact on the cash generation from the changes in variable rate.

An additional benefit that investors can capture from staying long on RQI is the embedded exposure towards preferred and fixed income REIT securities, which as of September 30, 2023 comprised 20% of the total AuM . This means that in the scenario of falling interest rates, RQI really benefits from the duration factor that is based on three sources: (1) commercial real estate, (2) external leverage, and (3) preferred and fixed income instruments that per definition embody greater sensitivity to the changes in the monetary policy.

The bottom line

Currently, RQI provides a dividend yield of 8.2% that is underpinned by robust fundamentals. Previously, there were some concerns about the sustainability of the dividend because of the potential consequences from RQI repricing its debt position. However, now when more restrictive monetary policy seems very unlikely and the probability of experiencing rate cuts over the foreseeable future, the dividend is clearly derisked.

Plus, due to the combination of external leverage and allocation into real estate and preferred & fixed income securities, RQI is greatly positioned to provide tangible capital gains from the changes in the interests rates.

Yet, investors have to be still cognizant of the scenario in which the SOFR stays this high for longer and does not trend downwards for the next several years, thereby forcing RQI to rollover debt at much higher costs. In this case, RQI's dividend would be in a serious trouble, considering the spread of the existing cost of financing and the market level.

All in all, in my opinion, RQI has become a more appealing investment to consider against the backdrop of the current dynamics in the monetary policy.

For further details see:

RQI: 8% Yield And A Nice Way To Play The Duration Exposure