RQI - RQI: A 9.66% Yielding REIT CEF That May Have Bottomed

2023-10-18 09:00:00 ET

Summary

- The Cohen & Steers Quality Income Realty Fund may have bottomed after bouncing off long-term support levels.

- RQI has historically rebounded after hitting the $10 level, indicating potential for future growth.

- Despite a challenging year for real estate, RQI remains an attractive income investment with a strong track record of distributions.

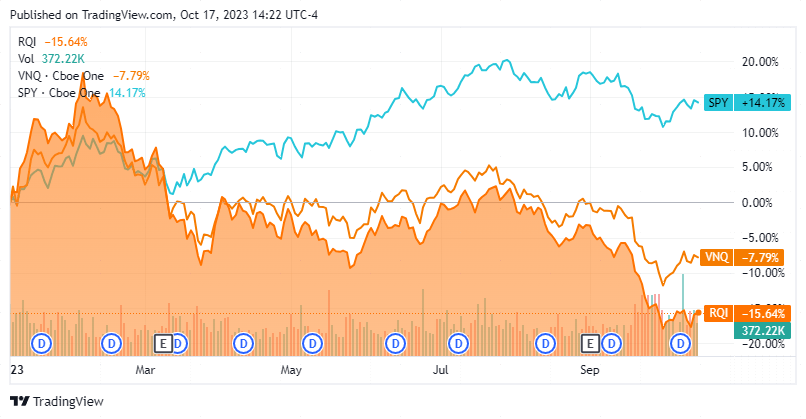

It's been a difficult year for real estate as rising rates have changed the dynamic of these investments. The Vanguard Real Estate Index Fund ETF Shares (VNQ) has declined by -6.64% YTD while one of the most popular REITs on Seeking Alpha, Realty Income (O) has declined by -19.73% in 2023. As 12-month treasuries (US12M) have yields that exceed 5.4% and investors can lock in a 4.8% yield on a 10-year treasury (US10Y), equity risk from income investments has become less appealing for some income investors. I have been sifting through the carnage and looking for what I believe will become strategic long-term opportunities. The Cohen & Steers Quality Income Realty Fund (RQI) has again caught my interest. This closed-end fund [CEF] allocates its assets into real estate securities and is focused on generating large amounts of income with a secondary focus on capital appreciation. Despite the REITs sell-off, RQI may have bottomed as it bounced off long-term support levels. I plan on adding to my investment in RQI as I believe REITs will turn around in 2024.

{kind=link}

Following up on my previous article on RQI

I had previously written an article covering RQI in April of 2022 ( can be read here ) and wanted to follow up since many REITs have faced downward declines. In the article I discussed how CEFs were different from traditional mutual funds, the investment methodology of RQI, its distribution history, and its total return over 2 decades. At the time inflation climbed to levels not seen since the early 1980s and as we now know, it wasn't transitory. This caused the Fed to hike interest rates which has been negative for REITs. Since April of 2022 RQI has declined -38.01% and after factoring in the distributions, its total return is -28.91%. I wanted to follow up on RQI because I believe the Fed is at the end of its tightening cycle and RQI is in a bottoming process as it's bouncing off key support levels. I plan on dollar cost averaging into my position in RQI and wanted to revisit this idea since the macroeconomic environment has drastically changed over the past year and a half.

The Cohen & Steers Quality Income Realty Fund may have bottomed after bouncing off long-term support.

Over the past ten years, RQI has declined by -2%, and while the current share price is just above $10, it has spent the majority of the past decade significantly above $11.50. The $10 level has acted as a long-term support level, excluding the pandemic crash. Over the past decade, RQI has receded toward the $10 level many times and broke through it twice, but each time it came back:

- 9/22/14 RQI hit $10.51 then rebounded to $12.85 by 1/19/15

- 2/8/16 RQI hit $10.52 then rebounded to $14.67 on 7/25/16

- 12/24/18 RQI hit $10.18 then rebounded to $15.85 on 9/23/19

- 3/16/20 RQI hit $7.43 then rebounded to $18.22 on 12/27/21

- 10/10/22 RQI hit $10.99 then rebounded to $13.51 on 2/6/23

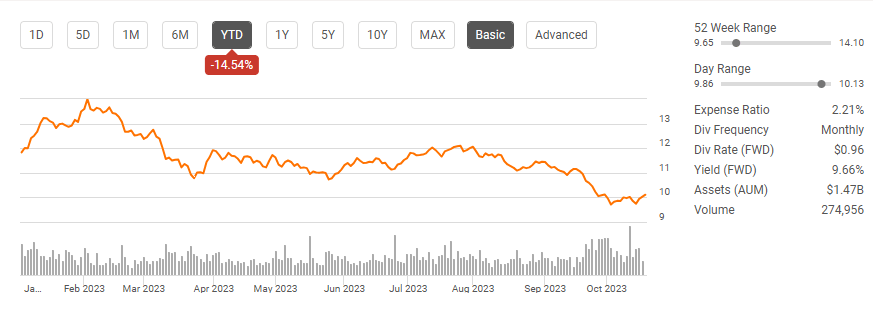

Recently, shares of RQI dipped below $10 but failed to stay below this long-term support level. Back during the initial pandemic crash, shares of RQI had dipped below $10 for the first time since 2013, and that stint was short-lived. This time around, RQI remained under $10 for several days and managed to resurface. It hasn't been an easy road for investors, as shares of RQI have lost roughly -40% of their value since the beginning of 2022. The rising rate environment hasn't been advantageous for real estate, and shares of RQI have been under pressure. I think it's important that shares didn't continue downward after breaking through the $10 level and ultimately reestablished trading above this long-term resistance level. Shares of RQI may bounce around a bit, but I think they are in a bottoming process, and as we have seen before, shares have ultimately found the strength to head higher over the past decade when threatened with establishing a new trend under the $10 level.

{kind=link}

I am bullish on RQI despite Real Estate underperforming the market

It's no surprise that RQI isn't having a good year due to rising rates. The Fed has hiked rates at the quickest pace since the early 1980s, and its tightening cycle has drastically impacted the credit markets, banking, and real estate. Bloomberg reported that the commercial real estate market has roughly $1.5 trillion in loan maturities due from 2023 to 2025. This could turn from active loans to defaults or foreclosures where landlords would be forced to turn the keys over to banks as the assets were used as collateral against the loans. Morgan Stanley ( MS ) has speculated that commercial real estate values could fall as much as -40% in the process. The impacts from the Feds decisions have been felt by the largest companies as Unibail-Rodamco-Westfield and Brookfield Properties are getting ready to hand the keys to the Westfield San Francisco Centre, which is a 1.2-million-square-foot shopping center in downtown San Francisco's Union Square, back to its lenders. Payments have stopped on their $588 million loan.

The S&P is up roughly 14%, while VNQ has fallen almost 8%, and RQI is down by double digits. The macroeconomic environment hasn't been bullish for REITs in general, as properties could be unmanageable if the debt coming due isn't financed at lower levels than what rates will allow for in today's market. This has caused many REITs to decline in value, and even the ones with mitigated downside risk through swaps have been impacted. RQI invests at least 90% of its total assets in common stocks, preferred stocks, and other equity securities issued by real estate companies. RQI will allocate at least 80% of the invested capital to income-producing equity securities issued by high-quality REITs. With $2.19 billion in managed assets and 32.44% leverage throughout its portfolio, it's not surprising that shares have taken a large hit.

{kind=link}

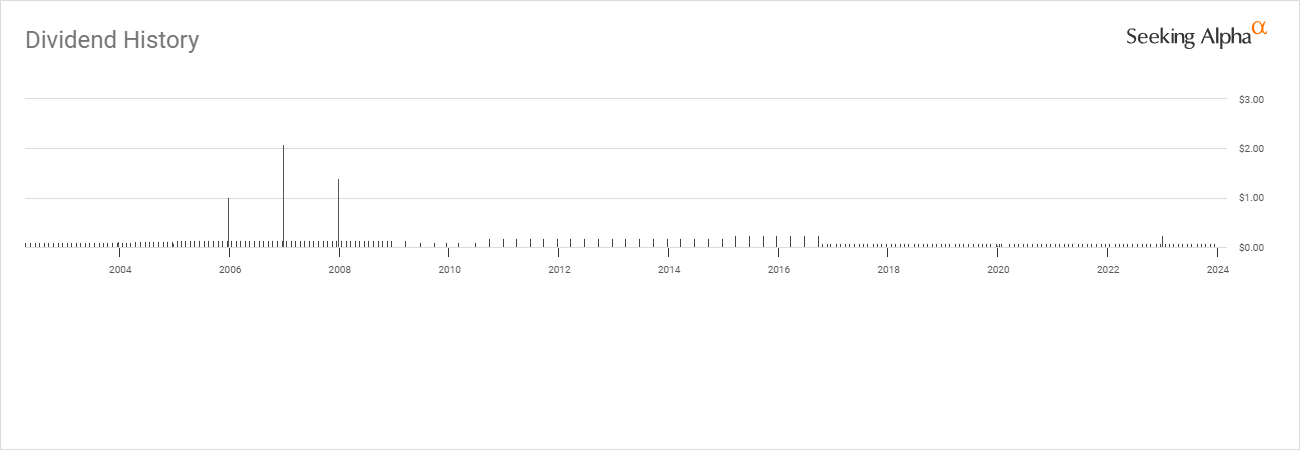

Since its inception, RQI has paid a healthy distribution, which started as monthly, went to quarterly, and is now paid in monthly installments. I am looking at RQI as an income play that could rebound in the future. RQI went IPO for $15 on 2/24/02, and over the past 22 years, shares have withstood a financial crisis, mortgage crisis, pandemic, and a rising rate environment. While shares have ultimately shed 1/3rd of their value over the past 2 decades, they have distributed $28.11 per share in income. Long-term shareholders have generated 187.39% of their initial investment through distributed income. RQI has not missed a distribution and is yielding almost 10% due to the declining share price.

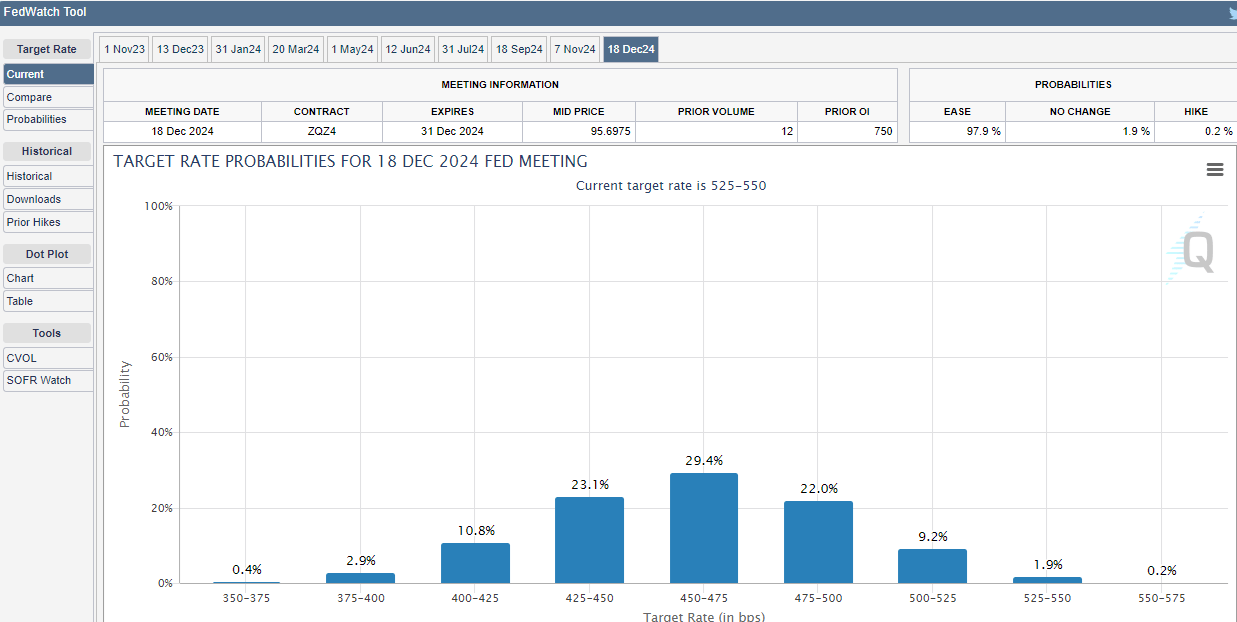

I think we are at the end of the Fed tightening cycle as CPI has remained under 4%, and Core CPI has fallen for 6 consecutive months to 4.1%. My prediction is that the Fed will pivot in the first half of 2024 if Core CPI continues to fall into the low to mid-3 range. The CME Group Fed Watch Tool is now forecasting an 11.8% chance of a .25 bps increase in rates in November and a 31.4% chance for a .25 bps increase in December. Overall, the percentages of another rate hike continue to decline, and as CPI continues to decline, there is less of a reason for the Fed to increase rates. Looking out to the end of 2024, CME Group has the highest conviction that rates will be between 450 - 475 bps and a 63.3% chance rates will be between 4 - 4.75 bps. If the Fed starts to pivot in 2024, the risk-free rate of return will decline and make treasuries less attractive. I think capital will flow into income investments as the risk-free rate declines, and real estate will look attractive as the negative impacts of high-rates also decline. This will be bullish for RQI, and investors could catch this CEF at the lowest point since the pandemic and add a monthly income generator with a strong record of distributions.

{kind=link}

{kind=link}

The risks of investing in RQI

My investment thesis on RQI could drastically be impacted if the Fed does hold rates higher for longer or takes rates higher. With $1.5 trillion in loan maturities due from 2023 to 2025, a lot of my thesis is tied to rates. When companies refinance at higher rates than their loans were established, it impacts the P&L statements as additional interest expenses are accrued. This could leave some assets underwater, forcing companies to either foreclose on the properties or sell them at discounted rates. This scenario could drag REITs further into the red even if the impacts are minimal, as the entire industry will be looked at as toxic. If the Fed keeps rates higher for longer or increases, it would most likely be negative for REITs and other income investments. In addition to the operating issues, income investors won't be as incentivized to move capital from non-risk assets to equities if rates remain at these levels or go higher. This could also strain the investment case for REITs and RQI in particular.

Conclusion

I plan on adding to my position in RQI as it looks as if shares are bouncing off long-term support levels. An investment in RQI carries significant risk because if the Fed takes rates higher or stays higher for an extended period, the real estate market could continue to be negatively impacted and cause additional strain on REITs. I believe that the Fed is probably done hiking and will pivot in the first half of 2024. I am basing my timing of dollar cost averaging on what I think will occur regarding Fed policy and how REITS will respond in a declining rate environment. RQI could continue to be negatively impacted, but I feel that 2024 will be a much stronger year for REITs, and want to lower my cost basis on shares of RQI.

For further details see:

RQI: A 9.66% Yielding REIT CEF That May Have Bottomed