RQI - RQI: Real Estate Is On Fire And This 7.84% Yielding CEF Can Go Higher

2024-01-04 13:00:00 ET

Summary

- Big tech led the market in 2023, but a broad market rebound is expected in 2024, with the income trade becoming more popular.

- The Cohen & Steers Quality Income Realty Fund is a diversified CEF focused on real estate, generating a 7.84% annualized distribution.

- The income trade in real estate is expected to do well in 2024 as interest rates decline, making REITs an attractive investment. RQI is expected to continue rebounding and generating large distributions.

2023 was the year of big tech as the Magnificent 7 led the markets higher. Income-producing assets fell out of favor, with the risk-free rate of return exceeding 5%. Many sectors, including industrials, real estate, energy, and utilities, underperformed the market as investors had less of a reason to take on risk to generate income. As big tech grabbed headlines and proceeded to appreciate, the higher for longer rate environment negatively impacted sectors that are typically associated with generating income. While big tech led the way in 2023, I think a broad market rebound will be the story for 2024, and the income trade will come into focus. I have been a fan of the Cohen & Steers Quality Income Realty Fund ( RQI ) and added to my position as shares significantly declined during the fall months. RQI is a diversified CEF focused on real estate with 206 positions and generates an annualized distribution of 7.84% through monthly distributions. As the Fed looks to pivot, I think the income trade will become more popular, and RQI will continue rebounding while generating large distributions in 2024. I am long RQI and am planning on continuing to add to my position during Q1 2024.

{kind=link}

Following up on my previous article about RQI

I look for positions that I feel are undervalued, which I believe will generate an appealing return over a long period of time. Being able to time the markets is extremely difficult, and getting in at the very bottom and selling at the top occurs infrequently. I previously wrote an article on RQI on October 18th ( can be read here ), and this ended up being a great call. Since then, shares of RQI have appreciated by 24.45% compared to 8.43% on the S&P 500. When the monthly distributions since that article are factored in, RQI's total return has been 26.35%. At the time, I had felt REITs and real estate-focused funds sold off too much, and after additional macroeconomic data, I think REITs and real estate funds will do exceptionally well in 2024. I am following up on my previous article with my outlook on RQI and why I am still planning on adding to my position despite a large bounce off the bottom.

Why I believe the income play will do well in 2024 and real estate will be a shining spot in the market

In the spring of 2023 , Silicon Valley Bank collapsed along with Signature Bank and First Republic Bank. The domino effect impacted the financial markets, and we endured a regional banking crisis as fears of a bank run increased and the potential for additional failures due to mismanaged risk mitigation increased. As rates continued to increase, the face value of lower-yielding bonds decreased with new debt being issued with higher yields. The regionals came under significant pressure until the government backstopped deposits, and the fear shifted to the debt markets. Financials weren't out of the woods yet, as commercial real estate was having its own issues, as hybrid work policies were impacting occupancy rates and leasing activity in the office sector. The commercial real estate market was estimated to have roughly $1.5 trillion in loan maturities due from 2023 to 2025, according to Bloomberg . There was approximately $1.2 trillion of real estate debt held by regional banks which couldn't have come at a worse time as a regional banking crisis was occurring.

Many REITs, especially those focused on commercial real estate and office buildings, were slammed as an evolving bear case surfaced. While hybrid work still being considered normal didn't help, the main fear was around debt. Much of the debt that was maturing was issued at much lower rates when the cost of capital was at multi-decade lows. With rates at multi-decade highs, there was a widespread notion that operators wouldn't be able to refinance debt at rates that would fit into their operating models, causing them to hand the keys back to their lenders. As regional banks had roughly $1.2 billion of exposure, this acted as an additional fear because if this scenario occurred, regionals would be left with the keys to unwanted assets that they weren't equipped to manage. This would likely cause them to sell these assets at discounted rates to unload them off the books while realizing substantial losses. Morgan Stanley ( MS ) had speculated that commercial real estate values could fall as much as 40% if this scenario occurred, and many REITs and commercial real estate stocks significantly declined in value.

{kind=link}

The doomsday scenario ended up not playing out, and while many REITs and real estate ETFs drastically fell during the first half of 2023, a large rally was seen during the back half of 2023. REITs have always been associated with generating income because of the large dividends. The combination of a debt bubble and the risk-free rate of return exceeding 5% was a disaster for these investments. Being able to generate over 5% from money markets, CDs and T-bills became an alternative to income-producing assets that had market risk, especially with the possibility of operators defaulting on debt maturities increasing. At the last FOMC meeting , Jerome Powell specifically stated that the Fed believes they are likely to be near or at the peak of its tightening cycle. He also disclosed that Fed members took an individual assessment as to what they felt would be the appropriate path going forward. The results indicated that the Fed Funds Rate was at 4.6 percent at the end of 2024, 3.6 percent at the end of 2025, and 2.9 percent at the end of 2026. This has caused a further decline in rates as the 10-year finished 2023 at 3.83% after reaching 5%, and the 2-year fall from 5.49% to 4.25%.

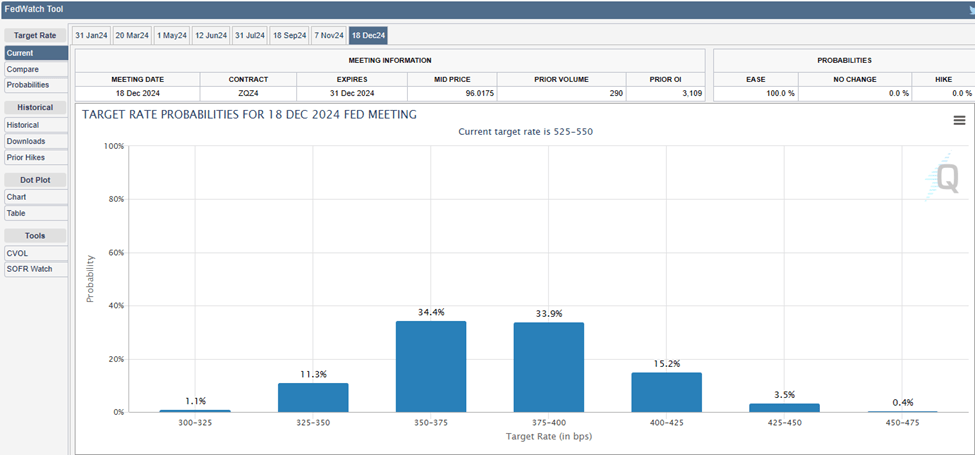

In my opinion, this is going to make the income trade a hot ticket item in 2024, with REITs front and center. The CME Group FedWatch Tool is now indicating there is a 15.5% chance a rate cut will be announced at the first Fed meeting of 2024 on January 31st, and there is a 68.3% chance rates close out 2024 somewhere between 350 bps and 400 bps. I feel that this is bullish for REITs because debt maturing over the next several years will be less of an issue than originally anticipated, and as the risk-free rate of return declines, there will be less of a reason for investors to keep capital in risk-free assets. I think that a portion of the capital that flows back into the market will look to recreate the yield that they have become accustomed to, and REITs are already associated with higher-than-average yields. This should cause them to be at the top of the list for reallocating capital. I think that we're going to see stronger earnings and better forward projections from REITs as we move further away from the doomsday scenario that isn't taking place. If this occurs, RQI should continue to move higher in 2024.

Why I am sticking with RQI and adding more

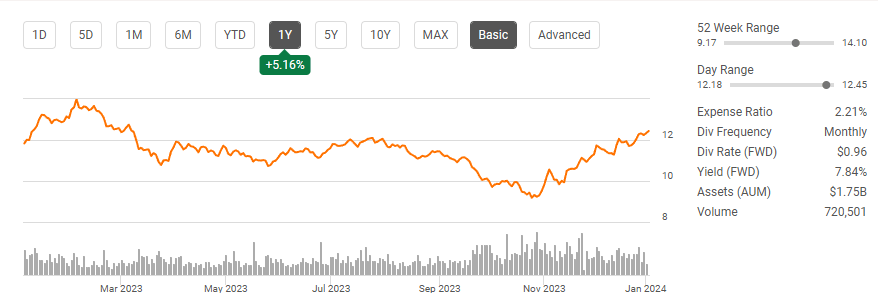

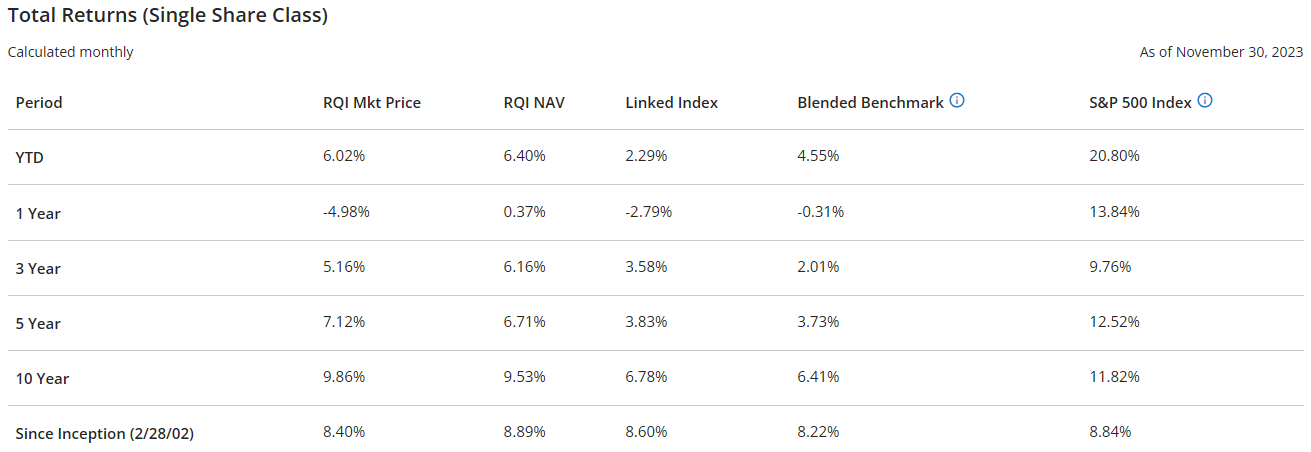

I am a fan of real estate, but I don't want to be a landlord. I prefer to invest in REITs and funds that focus on REITs as an indirect way to own real estate assets that generate income. Shares of RQI dipped below $10 for a month or so in the fall of 2023 and have rallied by around 35% since reaching a low of $9.17. RQI has $2.34 billion in assets under management ((AUM)) and focuses its investments throughout a broad range of real estate assets, which include Healthcare, infrastructure, preferreds, industrial self-storage, apartments, data centers, and corporate bonds. Since its inception, RQI has established a positive track record with an average annual return of 8.4%, which is slightly lower than the S&P, which has returned an average of 8.84%. RQI has managed its portfolio of assets for more than 2 decades, and I am confident that having navigated the financial crisis, the mortgage crisis, the pandemic, and the recent regional banking crisis, its management team is well-equipped to manage its way through a period where rates are setting up well for real estate.

{kind=link}

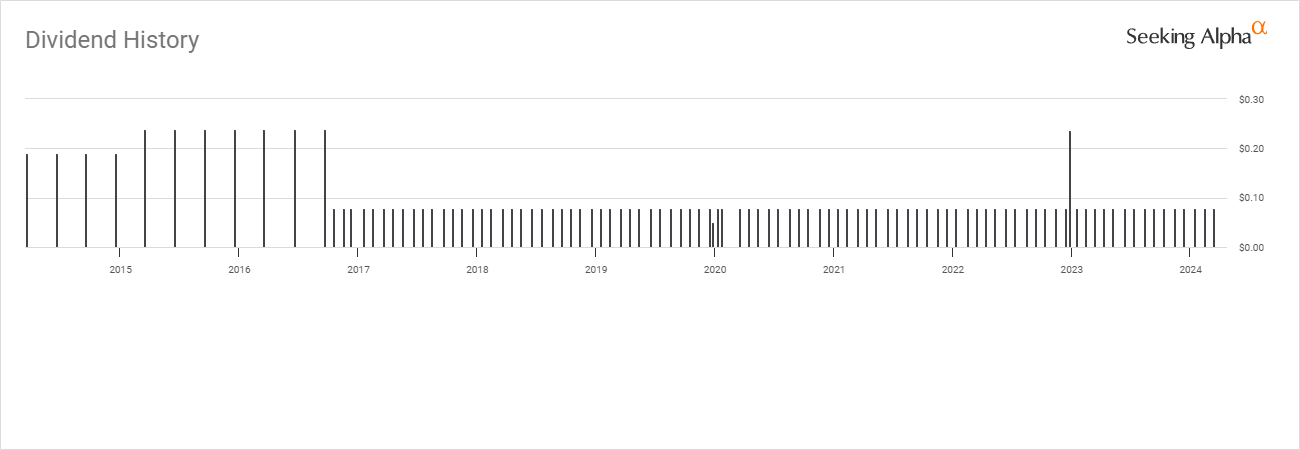

The other reason is their long-term track record of generating distributions. RQI is an income play for me so I am concerned with their ability to generate income as my primary objective and produce capital appreciation as a secondary goal. During 2023 , RQI didn't reduce the distribution, and it was paid on a monthly basis despite macroeconomic headwinds. RQI went IPO for $15 on 2/24/02 and has generated 187.39% of its initial value or $28.11 in ongoing distributions and has already declared its Q1 2024 distributions, which will bring its distributed income up to $28.35. If the distribution stays the same, RQI will generate $0.96 per share in distributed income throughout 2024, which is a current yield of 7.84%. From an income perspective, it's hard to compete with RQI as it produces a high single-digit yield and pays the distributions on a monthly basis. I think we're going to see capital appreciation and at least $0.96 of income being generated from RQI in 2024.

{kind=link}

Risks to my investment thesis

While I am bullish on real estate and RQI in 2024, there are risks to my investment thesis. First, RQI utilizes leverage to enhance its distribution. This is speculative and creates additional risks and costs for RQI. Currently, RQI has a leverage ratio of 30.4%, which could help increase larger amounts of net investment income, but the added risk could reduce RQI's NAV if the sector sells off. If inflation starts to increase again and the economy gets stronger, it could cause the Fed to reconsider cutting rates so quickly, which could pour cold water on the income trade. For the real estate sector specifically, it could spell more trouble as the risks associated with refinancing debt at current levels come back into focus, and it could cause financial and real estate stocks to head lower.

Conclusion

I think that RQI will attract many investors coming off the sidelines in addition to investors looking to reallocate capital if the income trade picks up the way I think it will. RQI has the Cohen & Steers backing behind it and established track records in generating a strong total return and ongoing distributable income for its investors. I think that we are going to see book values and earnings expand in the REIT space, which should increase the share value of RQI's underlying assets, which will correlate to a larger NAV and share price for RQI. I don't think the run is over, and I plan on increasing my position in Q1 of 2024.

For further details see:

RQI: Real Estate Is On Fire And This 7.84% Yielding CEF Can Go Higher