RSP - RSP: It's On The Right Track

2023-12-17 23:59:39 ET

Summary

- The S&P 500 is top-heavy with tech stocks, raising concerns about portfolio diversification.

- Invesco S&P 500 Equal Weight ETF offers equal weighting and sector balance, but its diversification benefits are unclear.

- RSP has had a similar performance to the S&P 500, but its larger drawdowns and negative momentum bias are worth consideration.

Motivation

The recent equity bull market has been driven primarily by the Magnificent 7 tech firms, which now leave the S&P 500 at a historic high concentration in these stocks. This new regime, paired with the relatively large TTM P/E ratio of 23.6 (Yahoo Finance) of the S&P 500 ( SPY ), poses practical questions for portfolio diversification going forward. Is the S&P 500 really diversified if it's so top-heavy? We are sympathetic to this line of thought.

The top-heavy nature of the S&P 500 is a consequence of its market cap weighting scheme. Choosing to weight a portfolio by market capitalization has a number of theoretical and practical advantages, but it naturally overweights overvalued stocks and underweights undervalued stocks when the market gets these weights wrong. Indeed, we generally want to do the opposite by overweighting higher forecasted return and/or lower volatility stocks and underweighting everything else. Equal weighting may achieve these goals to some extent.

The Positives of RSP

The Invesco S&P 500 Equal Weight ETF's ( RSP ) portfolio does exactly that: an equal 0.20% weighting across all S&P 500 constituents, in accordance with the S&P 500 Equal Weight Index. This moves RSP away from the Magnificent 7 and into the (less weighted and more value-y) heart of the S&P 500.

RSP holds smaller and less expensive stocks than the S&P 500. (Morningstar)

Certainly, equal weighting also restores some sector balance to the S&P 500. The tech sector (originally at 29%) no longer dominates the portfolio. Other sector weights are largely undisturbed, remaining similar to the original sector weights to within a few percentage points.

RSP has more favorable sector diversification than the S&P 500, specifically related to technology stocks. (S&P Dow Jones Indices)

Despite sounding good so far, we don't believe that the common arguments for RSP's inclusion into portfolios hold up to scrutiny.

The Rubs with RSP

RSP is almost definitely more diversified than the S&P 500 in our mind, but how much so? At the time of writing, the effective number of stocks held in the S&P 500, accounting for market cap weights, is ~180 (Shannon-Wiener diversity index). For an equal-weighted S&P 500, the effective number of stocks is plainly 500. This would be a tremendous difference if all stocks were uncorrelated, but especially within large caps, most stocks are strongly correlated with one another via market beta. Moreover, there are diminishing returns to diversification with an increasing number of stocks. We are skeptical of the benefits to be gained from this angle, and this lack of diversification in numbers is reflected in past performance.

The performance of RSP since inception versus the S&P 500 has been similar. RSP came out ahead in the years following the tech bubble and had a faster recovery after the financial crisis and COVID flash crash. RSP did, however, suffer larger drawdowns during those last two events, which is not encouraging. Moreover, the correlation to the S&P 500 has been 97%.

RSP and the S&P 500 have had comparable results over the last 20 years. (Portfolio Visualizer)

With the historical record not supporting diversification away from the S&P 500, RSP needs to have persistent excess returns to justify its place in a portfolio. Fortunately, RSP does seem to offer these somewhat.

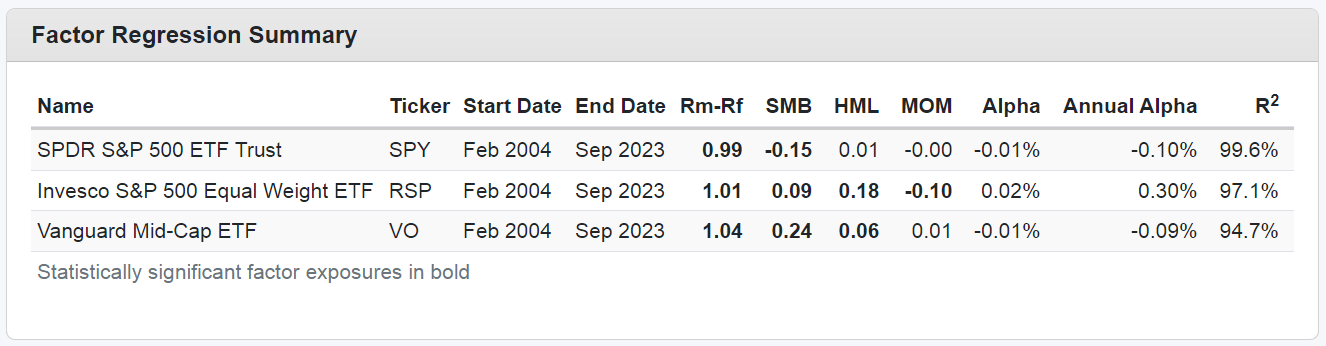

The TTM P/E ratio of RSP stands at 19.9 (Yahoo Finance), which is quite a bit lower than that of the S&P 500 and at least partially explains its larger drawdowns and higher historical volatility. To RSP's credit, a Fama-French 4-factor regression does indeed reveal a statistically significant historical value tilt. While the value tilt contributed negatively to RSP's realized return due to value's underperformance over the last decade, this should encourage future outperformance expectations. This said, if value is a desired portfolio factor, it could be better implemented directly using a large-cap value fund. Admittedly, this more targeted value approach deals in larger cap firms than is held in RSP.

On a more critical note, an index fund is probably not the most optimal way to manage an equal-weight portfolio. Turnover costs from quarterly rebalancing matter, but, to us, the greater evil is being short momentum. Any S&P 500 constituent that has a good quarter will be more likely to exhibit positive cross-sectional momentum effects, and selling winners and buying losers at the end of a quarter trade against this trend. The odds of this happening on any given trade are small, but, unfortunately, catalyzed by RSP's equal-weight structure, this harmful rebalancing tendency gets played out 500 times per quarter. The end result is a small but overwhelmingly statistically significant negative momentum bias. Granted, momentum strategies have not been roaring nearly as much as they have in previous decades (negative momentum has negligibly hurt RSP over 20 years), but this is probably not something we can rely on going forward.

There are ways to sidestep this problem, for example by tracking a market cap weight index with similar return expectations to RSP. Lyn Alden nicely argues that the Wilshire equal-weighted large cap index (an RSP proxy) has achieved similar results as the Wilshire value-weighted mid-cap index over roughly 50 years. This result is sensible given the smaller S&P 500 constituents are better described as mid caps than large caps. If only to avoid RSP's 0.20% expense ratio, we would instead recommend the Vanguard Mid Cap Index Fund ETF ( VO ), which has a lower fee and is not short momentum. This said, it does hold smaller stocks with less of a value tilt, so again it is not the perfect substitute.

Fama-French 4-factor regressions of SPY, RSP, and VO. RSP has positive value and negative momentum loadings. (Portfolio Visualizer)

{kind=link}

Verdict

RSP is a sensible fund, but not without drawbacks. An ideal solution to the diversification problem involves taking smaller and more frequent bets, regular turnover, and inclusion of assets, risks, or styles with a low or negative correlation to market beta. RSP accomplishes all of these things in an unsatisfactory manner. This is not a sleight on Invesco - the implementation is done as well as it can be given the constraints of the index ETF vehicle - but true diversification requires more than a different portfolio weighting scheme.

RSP is a unique concept. Other funds aren't quite able to replicate what it does, but several do get close. RSP serves a slightly small, slightly value-tilted fund, which we like. However, we're unsure where RSP's bet against momentum places it among the hundreds of other similar but not identical products that don't have this snag.

In short, we don't presently believe that RSP is an efficient way to drift away from a concentrated S&P 500. We do believe, however, that its philosophy is on the right track.

For further details see:

RSP: It's On The Right Track