EADSF - RTX Corporation: The Stock Price Crash Provides Opportunity

2023-09-28 04:58:36 ET

Summary

- RTX Corporation stock has lost nearly 25% of its value due to issues with the geared turbofan engine.

- The problem with the PW1100G-JM engine is contamination in the high pressure turbine discs, affecting durability and time-on-wing.

- The company announced an increased number of engines to be inspected with estimated costs of $3.2 billion to $4.5 billion.

In July 2023, I analyzed the Investor Day of RTX Corporation (RTX) and issued a buy rating. Since that buy rating, however, the stock has lost nearly 25% of its value driven by expanding issues on the geared turbofan, which should have been a driver of profits in the years ahead as engine production becomes less loss making while services become profitable.

What Is The Problem With The PW1100G-JM Engine?

From technical perspective, the problem is that the Pratt & Whitney turbofans are coping with a contamination in the HPT (high pressure turbine) discs which could lead to earlier than anticipated fatigue cracks to occur. It's not an immediate threat, but it certainly is a durability issue and one of the many elements that is being considered when selecting a turbofan is not just its costs or fuel efficiency but also its durability and Time-on-Wing or ToW. The issues with the GTFs certainly dents the durability and Time-on-Wing, while in its pitches and contracts Pratt & Whitney likely made projections and guarantees to customers.

Engines are getting more complex and generally there is little margin for error, what makes the issue so bad for RTX Corporation is that the contamination has been present from 2015 to 2021 with the only positive that current engines do not suffer from contamination but it is somewhat remarkable that for a period of six years the contamination went unnoticed.

From technical perspective, it is not looking great for RTX Corporation because the contamination went unnoticed for so long. However, what I find equally problematic is how the company brought the news to the market. I have followed the Boeing ( BA ) 737 MAX crisis and what I highlighted many times is the importance of communication and how a company responds to a crisis and RTX Corporation did not do a great job.

Costs Are The Big Blow To Investors But Not Unexpectedly Large

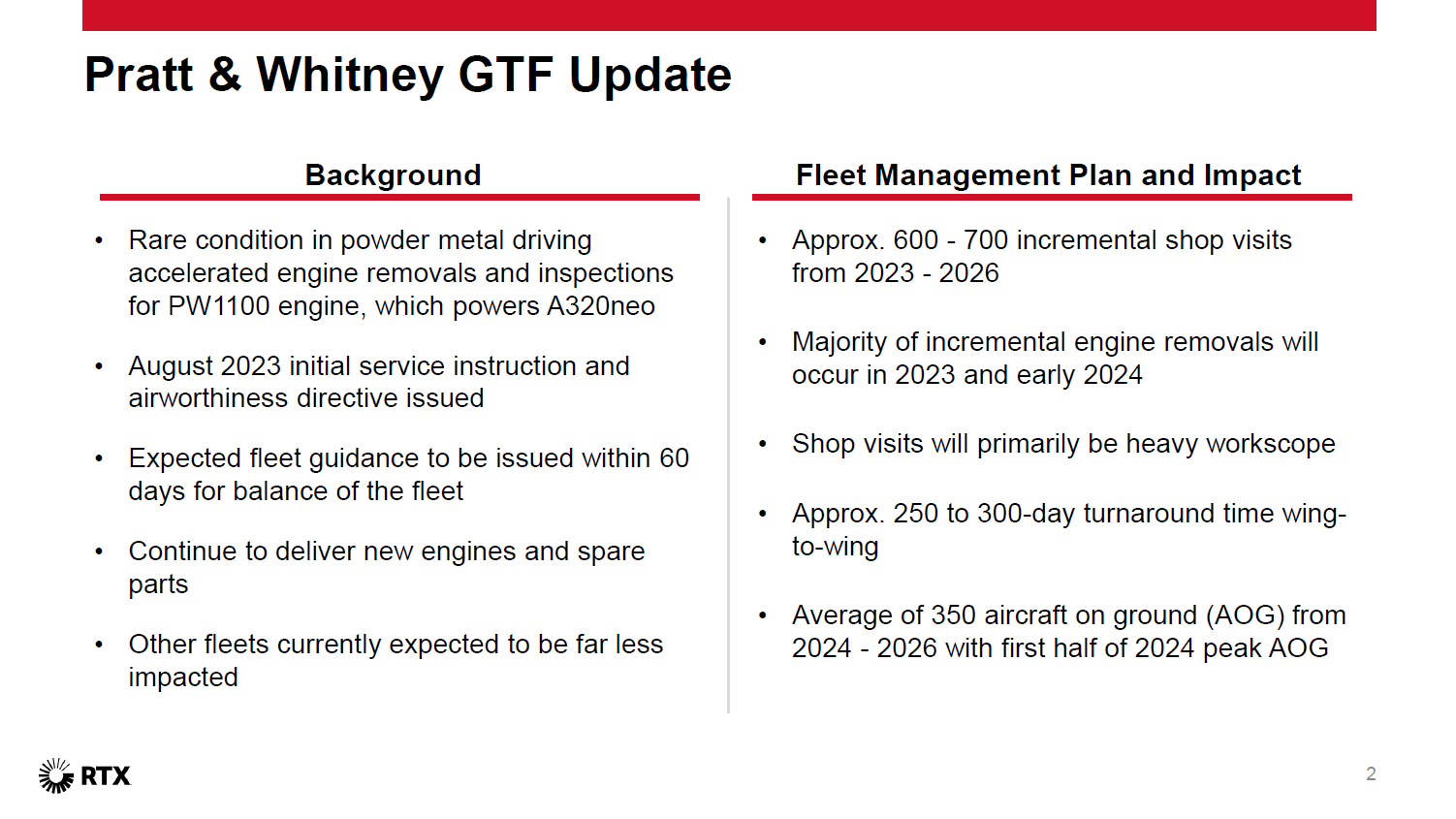

In July, during its investor day it was aware of a material issue that would affect Q2 deliveries but at the time the flaw that would add millions of dollars in costs was not yet disclosed and probably not known. During its second quarter earnings call a $500 million free cash flow cut to the guidance was announced on the back of the widespread contamination issue which would require accelerated inspections on 200 engines by September and ultimately 1,200 engines would require inspections with a 60-day turn around.

The costs for inspections would be around $17,000 plus possible additional costs of $171,085 per engine. For a batch of 200 engine this would indicate $3.4 million in inspection costs and $34.2 million in possible replacement costs. So, it can be concluded that the free cash flow hit does not come from the cost of inspection or replacement but is mostly caused by the turnaround for which airlines need to be compensated.

{kind=link}

In September, RTX provided an update increasing the scope from 200 engines to 600-700 engines which is significantly bigger than previously anticipated. Additionally, the turnaround time was much longer than the 60-day time-off-wing driving a $3 billion to $3.5 billion to be recognized in the third quarter. For 200 engines to be inspected with a free cash flow hit of $500 million, the multi-billion hit might seem excessive for 600-700 engines. By volume, the expected costs should be $1.625 billion. However, we also have to keep in mind the average turnaround time and by doing so we get to $7.5 billion. Most likely the $500 million free cash flow hit earlier announced was primarily carried by RTX while the current costs are share on a pro-rated basis. Pratt & Whitney has a 51% share in the program which would bring the cost estimate to $3.8 billion for with $3.2 billion as the lower bound and $4.5 billion as the higher bound. I have read comments from analysts saying the charge was larger than expected, but from the simple math one can do, this charge by no means is larger than expected and is actually lower than what the durations of the turn-around-times and scope would suggest.

What Is RTX Stock Worth?

{kind=link}

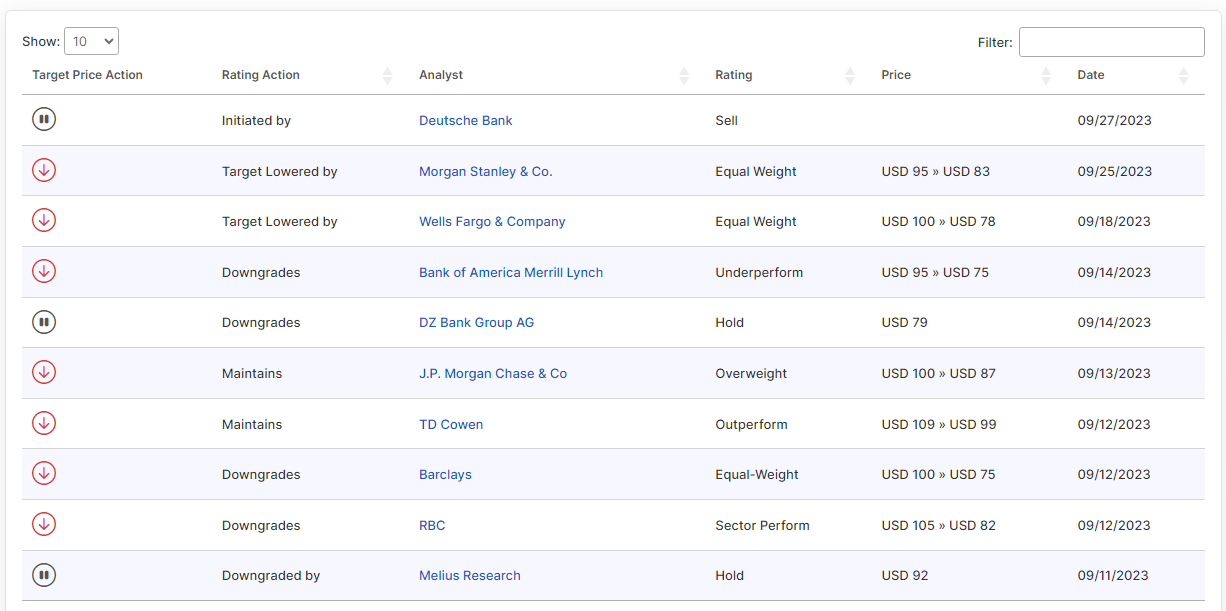

RTX was hit with a series of analyst downgrades in September, and I can see why. First and foremost, there is the earnings pressure from the premature removals of the GTFs and secondly in terms of numbers of affected engines the scope grew significantly which somewhat suggests the company did not have clear sight on how widespread the issue was. Furthermore, the issues on the HPTs are not new they went unnoticed until a few years ago and it is highly likely that in-service issues with the HPTs have led to the identification of the issue.

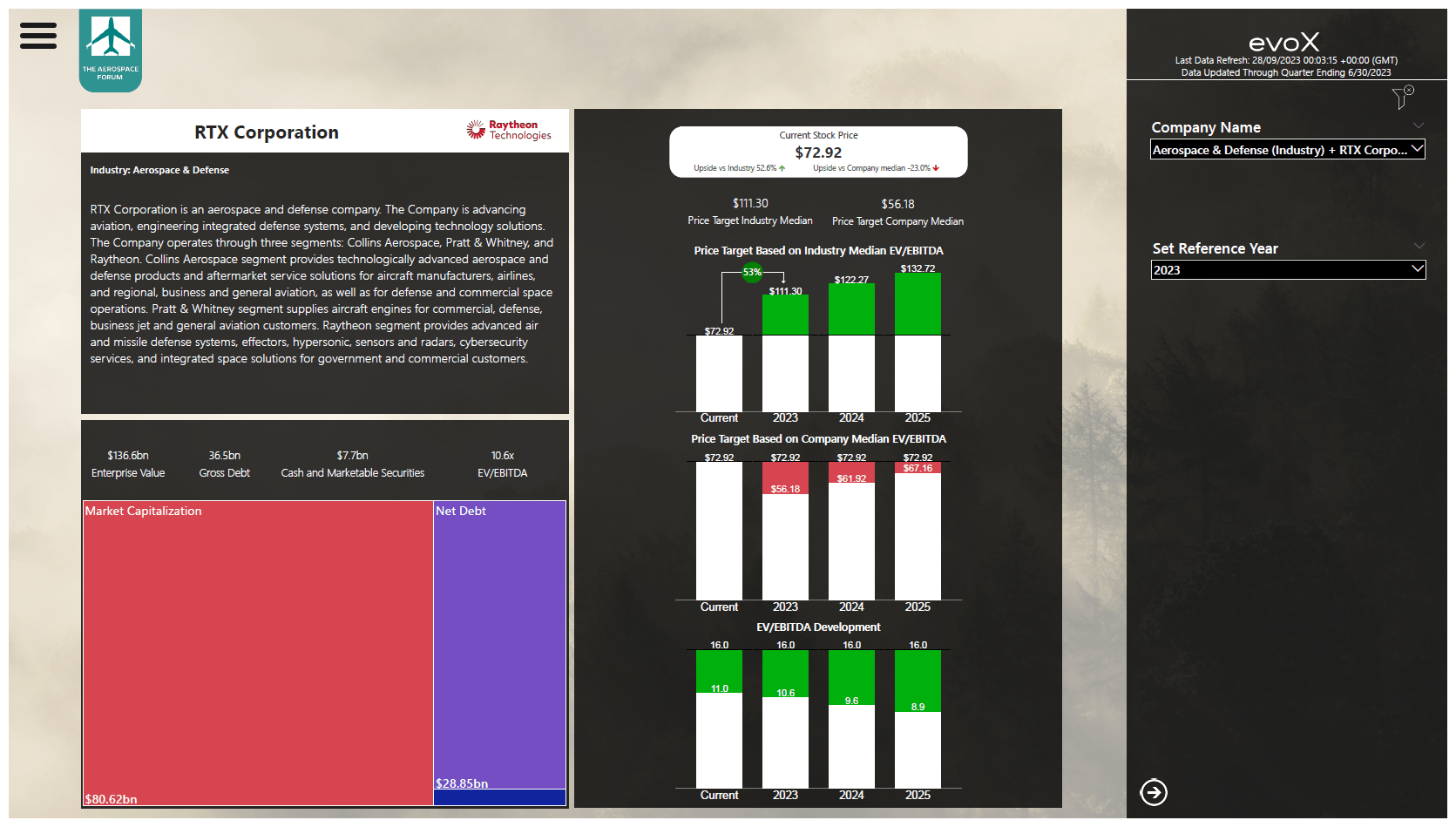

RTX Corporation stock price valuation using evoX Financial Analytics (The Aerospace Forum)

{kind=link}

When inserting the updated numbers in my model, at 8 times earnings, which is the company median, RTX offers little to no upside. At the industry median the upside would be around 53% and the $111 price target would coincide with the highest sell-side rating . However, I do think that valuing RTX at 16x EV-EBITDA is a bit overdone since there is a lot of uncertainty regarding the actual costs of the GTF debacle and what the actual cost trajectory will be like. Management certainly lost some credibility on it as the company first painted rosy pictures during the investor day and then had to announce premature engine removals for hundreds of airplanes.

If we let RTX stock trade between its median and the industry median then the stock price target would be $84 with 15.6% upside. Combined with a 3.3% yield I think that is attractive upside that the company continues to offer.

Conclusion: RTX Remains Attractive But There Is Risk

I believe that RTX remains attractive while I also agree with analysts pointing out to be cautious with this name. Management has provided transparency on the cost outlook in an earnings call, but it should also be noted that the newly announced scope of inspections is broader than just the 200 engines initially quoted for early removal and inspections, and it gives the impression that management was one step behind.

However, even when we let RTX trade at a discount, there is appealing upside to the stock in combination with a >3% dividend yield. There is of course also the risk that cost will grow beyond what is currently estimated, but that risk is accounted for part by not valuing the stock in line with the industry median.

For further details see:

RTX Corporation: The Stock Price Crash Provides Opportunity