RUBSF - Rubis Grows Its Dividend Despite Higher Renewable Capex

2023-05-28 09:00:00 ET

Summary

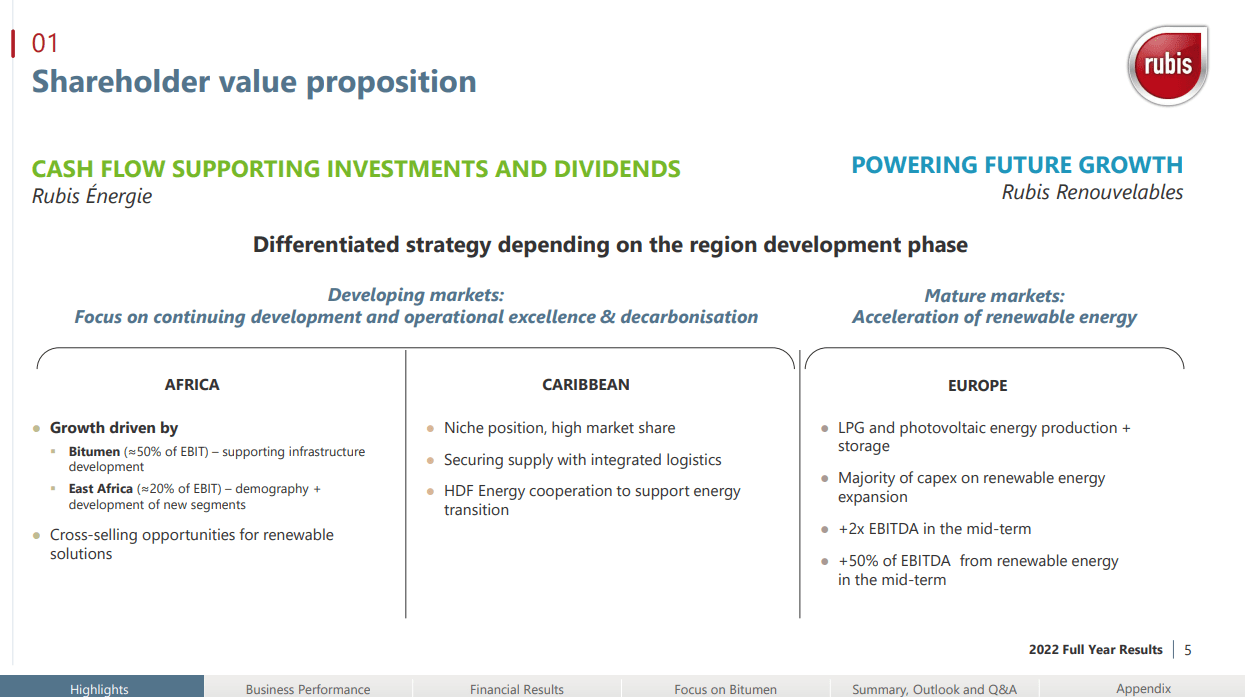

- Rubis is signaling that its initial Photosol acquisition will definitely not be the end of the renewable foray, where they want 50% of European EBITDA to be from renewables.

- In Africa, while infrastructure spending has reverted slightly, new markets are being opened in South Africa, and bitumen becomes a key driver of African EBITDA.

- Europe would be unlikely to have such a warm winter again in the coming year, so weaker results there should revert in late-2023. Stockpiling helps terminal business.

- Shipping stays strong thanks to new bitumen businesses in South Africa, refinery margins remain, as ever, contractually fixed in the Caribbean.

- Dividend up 3%, cash flows stable, CAPEX will continue to drive growth in addition to organic tailwinds in Africa and Europe. Yield at 7.4%, clear buy.

Rubis ( OTCPK:RBSFY )( OTCPK:RUBSF ) remains a great dividend pick. While the dividend growth isn't tremendous, the CAPEX sink they plan for renewables seems wise, and organically we expect growth in Europe, and sustained growth in Africa as the bitumen exposure grows and becomes the region's driver. Haiti's troubles are not tanking Caribbean revenues, and segments like shipping which we expected to see decline has been helped by the idiosyncratic growth in the African bitumen business, supported by an entry into South Africa. With a mild winter in Europe not likely to repeat itself, stockpiling in Rubis' Rotterdam terminals, and with the relatively secular growth of bitumen demand driven by African infrastructure needs and this new South African foray, Rubis looks to be in for a good year.

Q1 2023 Results

The trading update is out and we can see the more updated performance of the company, while not as detailed as the HY and FY disclosures. Some of the big effects we are seeing are related to geopolitical concerns and LPG. With the Ukraine war, Russian gas is no longer a chief option, and therefore stockpiling is happening which is supporting Rubis' terminalling business. Revenue is up about 16% in the storage business, and it is being driven by stockpiling ahead of expectations of a colder winter in Europe, where the last one was uncharacteristically warm. It's a great infrastructure exposure to have with the terminals being at premier locations in the Rotterdam port.

The Support and Services operations, which include shipping, were actually up 51% in revenues thanks to strength in activity of bringing bitumen to the new South African bitumen operation. Otherwise, the SARA refinery remained perfectly stable, as is contractually set in the agreement with the French Antilles.

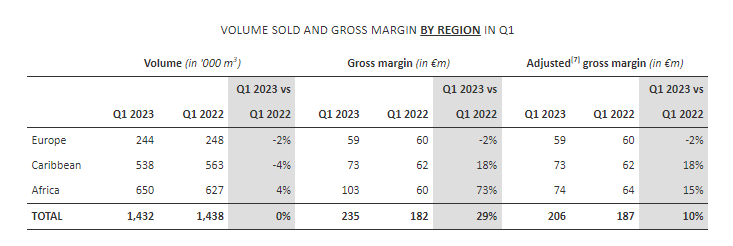

Moving onto the retail and marketing business, bitumen has been a key element this quarter. Regional gross profit growth shows strong results in the Caribbean and Africa. The Caribbean story remains much the same as last quarter: an aviation recovery. In Africa, Rubis is benefiting from the fact that they have opened a bitumen business in South Africa, which is a large market. So while in their previous markets volume was down after a hefty infrastructure spending bill in 2021 and 2022, the South African new business completely offset that, and in one year of activity that business has already matched the Senegal or Togo volumes after a 7x growth. As mentioned, Europe was weak due to a warm winter and less LPG volumes.

Retail and Marketing - Regional Breakdown (Q1 2023 Trading Update)

{kind=link}

On an activity basis within the retail and marketing business, retail fuel demand remained decent, growing slightly by 2% YoY, while C&I customers saw 11% volume declines but that was offset by higher unit margins, so gross margins were stable. Aviation is where the real growth is, concentrated in the Caribbean where those economies are tourism-levered.

Bottom Line

In the last presentation for the FY 2022 , Rubis started pointing markets towards a greater focus on the renewables business.

{kind=link}

They are planning on bringing the renewable contribution up to 50% of the European EBITDA in the medium-term. This is where the CAPEX will be going. The Photosol acquisition was their first foray, and they are growing their activity nicely thanks to growth in capacity. This will likely grow the CAPEX burden. At the same time, organic outlook looks great in its markets, with aviation recovery as well as new markets being found in Africa being important drivers, on top of higher expected LPG demand in Europe in the next, likely colder winter. In line with these expectations, Rubis has grown its dividend by 3%, and the yield is closing in on the 8% mark at current prices.

We are pretty optimistic about Rubis' gross profit growth potential. Moreover, we have seen that Rubis is unfazed in even the worst possible market environment for its assets, demonstrated by the only 10% declines in EBIT during COVID-19. It's an infrastructure play but with a 10x PE. A very low valuation. An 8% dividend yield on safe, sustainable infrastructure economics is a steal. A clear income and value buy.

For further details see:

Rubis Grows Its Dividend Despite Higher Renewable Capex