RUBSF - Rubis: On Track In A Volatile Environment

2023-03-21 12:22:27 ET

Summary

- Rubis reported overall robust volumes and income numbers and double-digit bottom line earnings growth, although it was adjusted due to FX issues and acquisitions fees.

- Photosol growth path is delayed due to "permit congestion", 2030 objective is unchanged.

- Management proposed a 3% increase in the dividend, which seems sustainable when looking at its cash flow.

- Interesting detailed exposition on the growing bitumen African business.

- Corporate net debt stands at an acceptable 1.5x EBITDA (pre-IFRS 16).

Rubis' (RBSFY) (RUBSF) recent full-year results release showed a continuation of the recovery path after COVID-19 lows with solid growth in unit profit in every region, compensating for cost inflation. Volumes have mostly remained relatively flat with a mild European winter and increased pricing contributing to the stagnation. Rubis Renewables saw some exciting recent developments with one bolt-on acquisition and their first corporate PPA but also delays with new projects.

Even with the positive momentum, the cash flow statement didn't follow the good picture revealed in the income statement and I struggled to understand why depreciation and amortization figures saw a significant drop. Non-recurrent items have also "clouded" the statements which for me is not a positive sign.

2022 Highlights

Flat volumes combined with increased unit margins have resulted in a robust 21% year-over-year growth in EBIT, when adjusted for the FX pass-through from Nigeria. Haiti impairment and Photosol related-acquisition costs affected 2022 results by about 56M€, but when adjusting for the non-recurring items the EPS goes to 3.16€, or a 7.74 PE at recent prices.

{kind=link}

Aviation in the Caribbean and bitumen in Africa appear to be firing on all cylinders, Europe's bad result can be explained by the mild temperature so it doesn't appear structural. Rubis terminal joint venture keeps the low growth path and the amazing cash generation capability, resulting in a nice 34M€ dividend paid to Rubis. All in all, the legacy fossil business looks healthy to drive the necessary investments for a renewable future.

Working capital, one of my concerns last year, seemed to normalize for the full year, even despite ending the second year in a row with an increase due to previous elevated oil prices. With the now depressed oil prices, we should see a positive cash effect on the working capital, at least for the start of the year.

Cash Flow Statement (Rubis Press Release)

For me, the cash flow statement is where the big question mark lies. I'm hoping the final annual financial report can answer why the sudden drop in D&A. We are seeing the lowest amount since 2015, with much fewer assets than now. Focusing on the cash flow before the cost of debt, taxes, and working capital, the value for 2022 is less than 2021 despite double-digit EBITDA and EBIT improvements. I feel it is relevant to know how much of this is non-recurring due to FX and Photosol fees? This can be a potential red flag to me.

{kind=link}

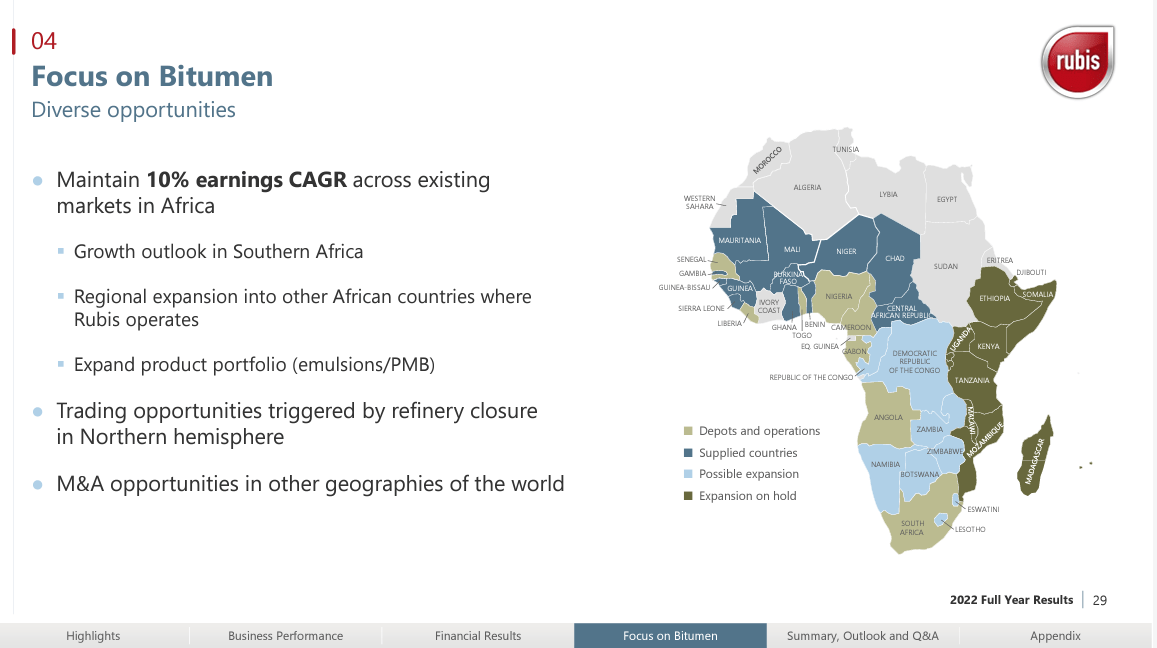

Bitumen

The relatively new area of bitumen was shown in detail during the earnings call as one of the future areas to develop. Rubis seems to have captured a competitive advantage by controlling the integrated supply chain between reliable Mediterranean refineries and an ever-increasing number of African countries. They have discovered yet another niche product that they can rapidly establish a dominant position in by controlling the supply. This is displayed by the >50% market share in operating regions and an amazing >20% ROIC.

The addressable market is huge and growing, and road expansion in Africa is understandably growing more than in other parts of the world; management claims that African oil is not able to produce bitumen and no sustainable replacement products are available (yet).

I believe Rubis is highly capable and experienced in finding smaller niche markets with some barriers to entry and this is another example. This should be the growth engine for Rubis Energie in Africa for the coming years.

{kind=link}

Rubis "Renouvelables"

The renewables part of Rubis maintains the growth course although, as discussed previously, experiencing already delays in the start due to grid connections and permits, explains the management. I can also guess that the "chaotic" macro environment didn't help, these projects need stability because of the long duration. This circumstance delays the project's cash flow more into the future, but it also delays the expansion CAPEX necessary to complete the project. They seem to be able to increase the future growth rate to compensate for the delays making the 2030 end goal the same.

While I don't think this changes materially Photosol value, that is not the case for the different economic cycle we are in when compared to late 2021. The acquisition date was at the end of the low-interest rate cycle at a corresponding price, cash flows long into the future are worth much less now plus the cost of capital has also reflected this change. While management would probably counter with the argument that electricity prices should follow, I'm afraid that those prices can only go up to a point, electricity is critical to people and businesses alike.

One of the advantages of Photosol's integration is the potential synergies and cross-selling opportunities between legacy businesses, solar, and hydrogen. I'm happy to see this is now being mentioned in the presentation with bundled solutions now being offered, Renewstable Barbados is an example. Profitability is yet to be determined.

Path Forward and Risks to Consider

It's safe to assume that Rubis renewable will drain cash for the coming years due to heavy investments in building up capacity while the other departments should provide steady low-growth cash to feed the future. The amount of cash needed shouldn't be significant since most of the "lifting" is going to be done through non-recourse debt, consequently reducing the equity investments necessary.

While I do trust the route forward chosen by the management team, the risks especially for the renewable segment are noteworthy. The HDF position is a highly uncertain bet and Photosol is operating in a highly competitive market, dependent on government support and very sensitive to outside conditions, namely interest rates. I don't see a competitive advantage outside France and consider it hard for them to obtain 20/25-year project stability in Africa anywhere soon to enable these PV projects. Plus, the significant leverage involved means there is little room to maneuver.

I have to add the cash flow statement mismatch and stagnation to the risks to be watched out for. A quality business and quality statements are the ones that show free cash flow similar to operating income and I like to see that in the companies I own, or at least be able to explain the reason why it's not. For the 2022 results, there are a lot of adjustments, including the (unexplained?) decrease in D&A.

Bottom Line

It's my opinion that Rubis is a very well-managed company that has consistently performed, with ups and downs, in its relatively short history. The recent price does not do justice to the business in my view. Yes, I know that it's not a high growth "sexy" area nor does it deliver high returns on capital, but at this price range, it's well worth the risk for me. If nothing more, the close to 8% dividend yield should be a good reward to wait and see what type of future they can provide with the renewable segment and bitumen business, if nothing more.

For further details see:

Rubis: On Track In A Volatile Environment