RUBSF - Rubis: We Don't Like The Renewable Plans

2023-12-04 02:06:15 ET

Summary

- Rubis has concerns about the sustainability of its dividend due to the major CAPEX burden in the renewable business.

- Gross margins and volumes are growing in primary businesses, but the investments in renewable generation assets are poor alternatives to shareholder payout.

- The plan for renewable generation will take years to generate significant revenue, while the company's own shares yield higher earnings.

- We don't like the company's direction at all anymore and have rating downgraded in agreement with the ailing price.

Rubis (RBSFY) (RUBSF) may have had perplexing performance to some, including to ourselves who have had a bullish view in prior periods. But some months ago we realised that Rubis has a major issue. There are concerns about the sustainability of the dividend by analysts, which is creating an overhang on the stock due to institutional concerns with income, all related to the major CAPEX burden slated for the renewable business, whose forecast returns offer a suboptimal prospect compared to buying back their own shares or even investing in their defining infrastructure. While concerns around their super-resilient primary businesses have good reasons to have now dissipated, what we believe is an ill-fated foray into renewable generation assets, an overcrowded markets, has disqualified this stock from being a buy by our standards.

Brief Quarterly Comment

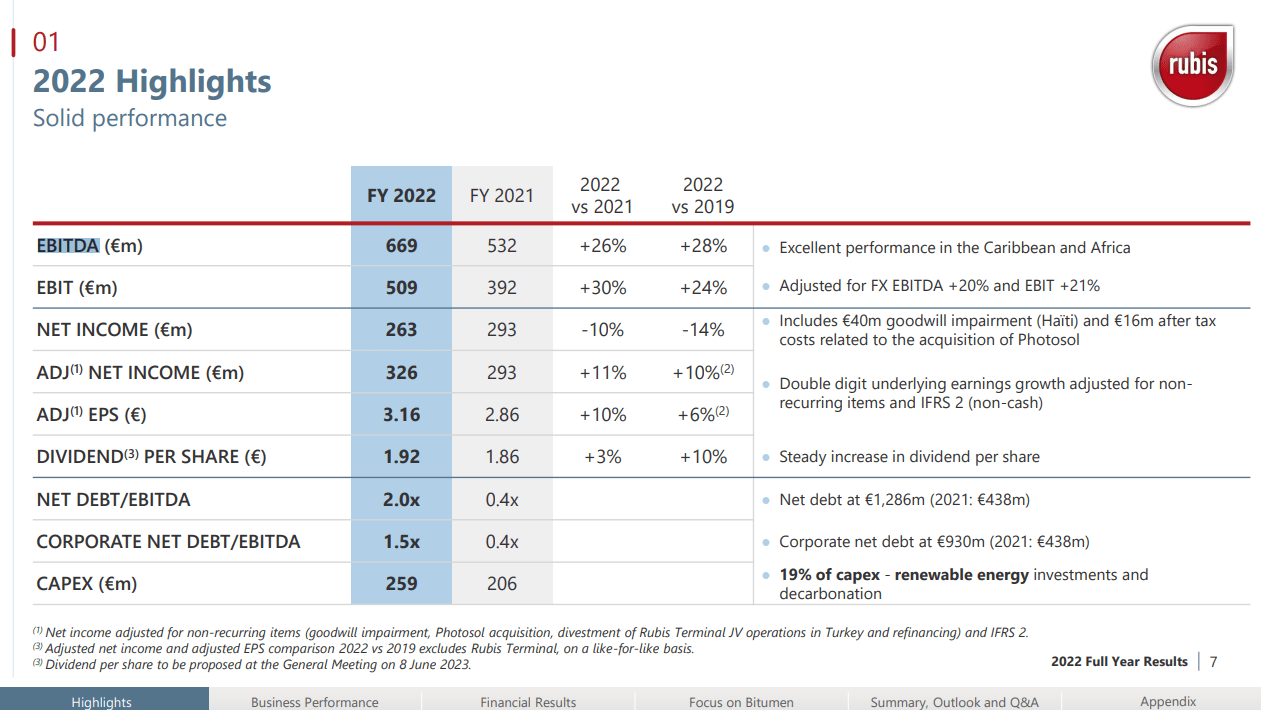

The trading update is in . Gross margins are growing, and volumes are coming up across the board. Bitumen is resuming its secular strength associated with substantial development investment going on in Nigeria and West Africa.

SARA has a totally mandated economic profile due to a deal with the French Antilles authority, and the energy shipping business remains strong. Bulk liquid storage remained strong with focus still on agriproducts and other energy needing storage for strategic reasons.

Really, the results look good and concerns around demand destruction in the retail businesses are seemingly behind us as energy prices in general, maybe not oil as much though, start calming down.

Our Issue

We don't like the investments in the renewable business at all. Their primary infrastructure is attractive, exposed to markets that will take forever to electrify, and with infrastructure earning highly stable economics. The PE is low at less than 8x, and the dividend is ample at above 8%. But instead of buying back their shares, which have a current earnings yield of around 12%, they are instead investing in renewable generation assets whose return profiles look quite weak.

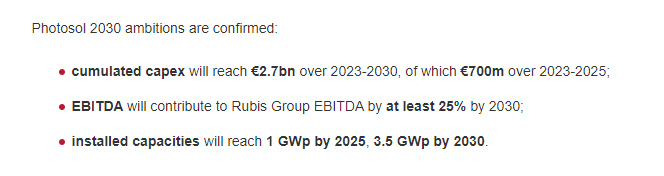

The plan is for renewable generation, including solar farms and so forth in Europe, to generate around 120-130 million EUR annually by 2030, still in a very long time. Cumulatively the investment to get there will be 2.7 billion EUR. It will take years for the revenue here to ramp. Currently, it is only a little more than 1% of annual figures.

The terminal yield on these investments is 10% pre-tax, not much more, and obviously less post tax, and this yield only comes in 2030, scaling up from here. That's simply not a good prospect when its own shares yield 12% in earnings today!

Photosol Plans (Trading Update Q3)

{kind=link}

What's more is that institutional analysts are concerned with the dividend's sustainability. Annualised CAPEX on just renewables is around 200 million EUR per year. Annualised net income is around 300-350 million EUR per year , and the payout ratio is already around 60%. Then there is another CAPEX that might be needed for the other businesses in excess of depreciation, although it seems that they are happy to leave their primary infrastructure to stall at current scale, which would also not be news we'd welcome. Indeed, in 2021 only a small portion of CAPEX was for the renewable projects, so there still seems to be some CAPEX excess of depreciation for current assets, which is still an issue for the dividend though.

{kind=link}

While the trading update recently doesn't provide much financial detail, the H1 does , and net debt is rising consistent with the unsustainability of the dividend burden, which management wants to raise to assuage concerns by institutional investors who are swayed by income.

Conclusion

We think these renewable investments are anti-economical relative to options like paying a more sustainable dividend and buying back shares while CAPEXing as necessary on current infrastructure. We don't want net debt to rise at current rates at all. Interest expense had already doubled YoY as of H1 2023. The risk of the dividend being reduced just means another possible hit on prices, and we don't agree with the core of management's capital allocation policies. Pass.

For further details see:

Rubis: We Don't Like The Renewable Plans