BIZD - Runway Growth Finance: You Really Should Consider This 12+% Yield For Your Portfolio

2023-09-28 03:52:10 ET

Summary

- Business Development Companies (BDCs) have performed well during rate hikes, unlike REITs, due to their high yields.

- Runway Growth Finance is a lesser-known BDC that focuses on technology, life sciences, healthcare, and select consumer services.

- RWAY has a growing and diversified portfolio, a strong management team, a conservative balance sheet, and a high dividend yield of over 12%.

- 99% of RWAY's loans are first-lien and 100% of its investments are floating rate. Additionally, they have a conservative balance sheet with no debt maturities until 2026.

- The company also currently trades at a discount to its NAV, making it attractive right now.

Introduction

Since the start of rate hikes Business Development Companies better known as BDCs have held up well. They've flourished during the rise of interest rates while REITs have tanked. Why? Because they typically offer high yields compared to the latter. As the REIT sector ( VNQ ) has dropped over 6% in the last year and 7% in the last month, the BDC ETF ( BIZD ) has done quite well returning roughly 16% in the last year, and is up 1.4% in the last 30 days. This is because many investors are now looking for higher-yielding investments while they wait out the decision of the FED as to when interest rates will be cut.

That brings me to Runway Growth Finance ( RWAY ). I've talked about this BDC with a few of my readers and it honestly doesn't get a lot of coverage here on Seeking Alpha. Currently the stock only has 1.33k followers, which is very low compared to some of its more popular peers, Ares Capital ( ARCC ) and Main Street Capital ( MAIN ), who have more than 72k and 68k respectively. To be fair, RWAY is a fairly new BDC having IPO'd in 2015, just 8 short years ago. In my eyes this BDC is a sleeper, so let's get into why you should consider this high-yielder for your portfolio.

Who Is Runway Growth Finance?

RWAY is a BDC that prefers to make investments in companies engaged in technology, life sciences, healthcare, product sectors, and information, business, & select consumer services. The reason they prefer investing in these sectors is because these organizations are intent on shaping the way we live, work, and do business. Since 2015, RWAY has backed more than 60 companies in these sectors, and funded more than 72 companies for a total loan commitment of $2.3 billion. In short, the BDC borrows debt at fixed rates and loans at floating rates to companies in their portfolio. That's the reason BDCs have thrived in the high rate environment while REITs have done the complete opposite. Many BDCs have floating rate portfolios, meaning while rates remain high, this is extra income for the them.

The difference between RWAY and other BDCs is that it focuses on late-stage and growth companies, providing risk mitigation across economic and market cycles, which in turn generate consistent portfolio yields with low credit losses. These companies also have strong insider ownership and provide unique portfolio expansion opportunities. RWAY typically invests in companies with loans from $10 to $100 million.

{kind=link}

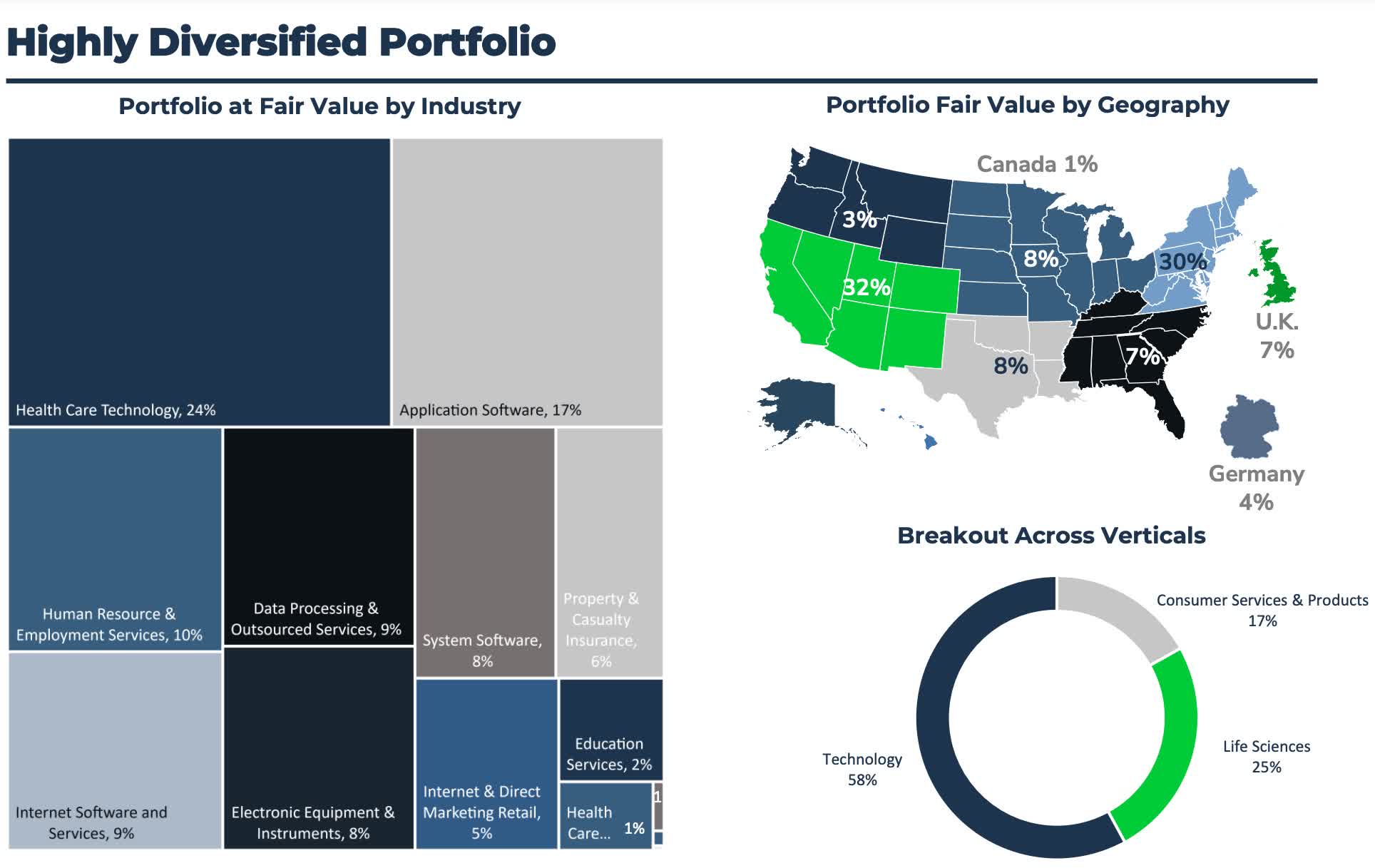

Growing & Diversified Portfolio

The company's biggest sector is in Healthcare Technology at 24%, with application software and human resource & employment services coming in second & third at 10% and 9% respectively. Since the company is based out of California, it makes sense most of its life sciences portfolio is based in the Western region of the United States. Besides its diversification, another thing I like about RWAY is that 100% of their loans are floating rate investments and 99% are invested in first-lien loans, with the remaining 1% in second-lien loans. This is in comparison to popular peer and largest BDC, Ares Capital, who has 42% invested in first-lien loans, and 68% floating rate debt investments.

{kind=link}

So, the company seeks out and prefers to invest in first-lien loans, which is an important factor, especially considering the current macro environment. Reason being, although BDCs have enjoyed a rise in net income over the last year, some have also had a rise in non-accrual loans during the same time. As rates rise, they demand more income because of their floating rate portfolios, and tenants have a higher tendency to default on loans. That in turn means less money collected from tenants, equaling less income for the BDC, and that eventually trickles down to reported earnings. Investing in first-lien loans gives RWAY head of the line privileges over all other debt holders, making it less likely this will happen.

Strong Management Team

One thing to note is RWAY is externally managed, similar to ARCC. This is important because investors typically prefer internally managed companies as they are more aligned with shareholders. There are also extra fees associated with outside management that investors must be aware of.

But besides being a fairly new BDC, the RWAY management team remains strong. In the current state of the economy, a stellar management team is very much needed to successfully navigate economic downturns. Especially if the country does enter into a recession.

The company's founder and CEO, David Spreng, is currently on a temporary leave of absence to undergo treatment for a medical procedure. Their founder has served on the board of 11 public companies prior to his role at RWAY. Runway Growth Finance Corp. is now headed by its former CIO Greg Greifeld, who's been with the company since 2016. Greifeld had several prior roles at JPMorgan ( JPM ), including Technology, Media, and Investment banking and the Special Investments Group. So while their interim CEO is new in the seat, he has plenty of experience working for companies like the behemoth that is JPM.

Conservative Balance Sheet

As BDCs enjoy increases in their income, they typically reward shareholders with supplementals and dividend raises. But one thing investors have to be aware of are debt maturities. If rates do remain higher for longer as stated, some may have to refinance their debt at higher rates. And although inflation is trending down from last year, it still remains sticky. This may prompt the FED to raise rates further, but markets believe the FED will hold rates steady through the rest of the year. I don't have a crystal ball so I can't say whether they will or not but I think it's all data dependent. If inflation remains sticky and CPI creeps back up, I can see another raise at the next meeting.

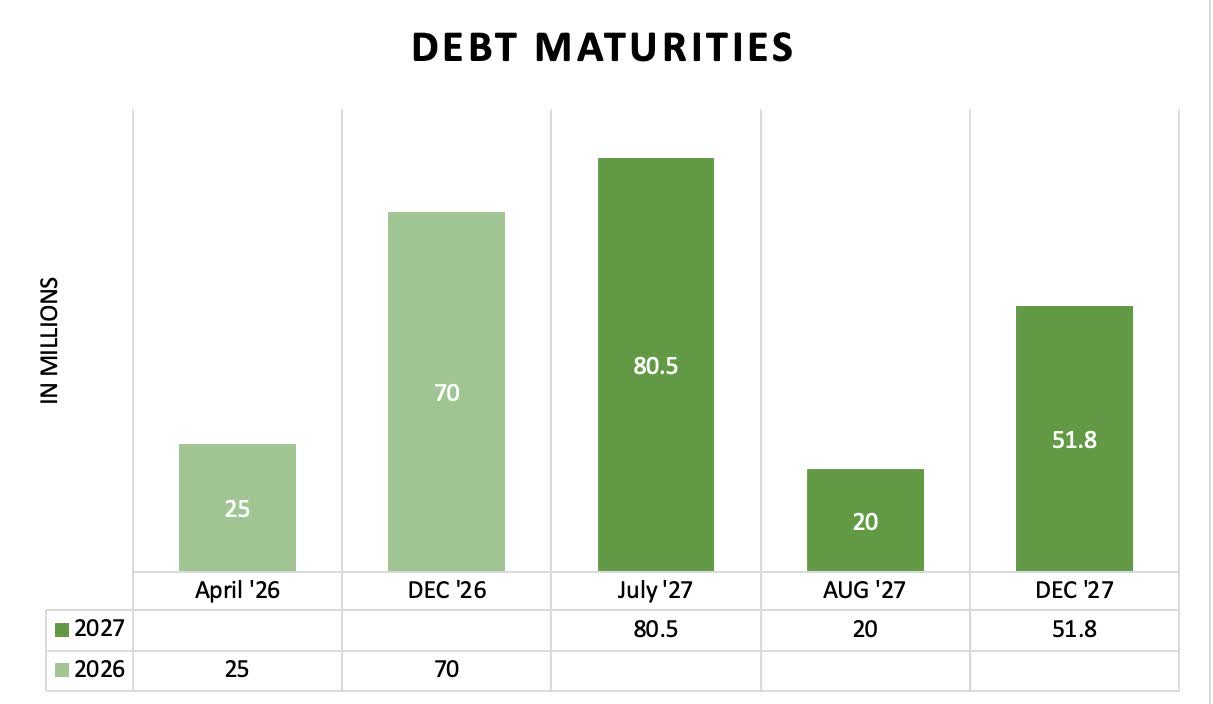

If so, companies will definitely feel more pain in the near-term. That's why a strong balance sheet is important when researching current high-yielding investments. Unlike peers ARCC and popular monthly payer MAIN, RWAY doesn't have any debt maturing until April of 2026. MAIN & ARCC both have debt maturing in 2024 & 2025. Below I've created a schedule of RWAY's debt maturities from now until the end of 2027.

{kind=link}

The BDC has $25 million in notes maturing in April. These have an average interest rate of 8.54% and $70 million maturing at the end of the year. These have an average interest rate of 4.25% bringing their total to $90 million due in 2026. I think it's safe to say interest rates will be lower by then so this is not of the slightest concern to me. Additionally, the company had more than enough cash on their balance sheet to cover this with $228 million in liquidity including unrestricted cash & cash equivalents. RWAY has a total of $152 million in notes maturing in 2027. These have an average interest rate of 7.5%.

Furthermore, RWAY has been decreasing its leverage and has among the industry's lowest ratio within the D/E target of 0.8-1.1x. They also managed to decrease leverage quarter-over-quarter to 0.97x from 1.04x, and increase asset coverage to 2.03x from 1.96x which is impressive given the environment. All investments in Q2 were funded with leverage as part of their strategy to generate non-dilutive portfolio growth going forward.

The Dividend

RWAY is currently yielding more than 12% at time of writing. The BDC currently pays a dividend of $0.40 and during Q2 earnings , management declared a supplemental of $0.05 per share, payable with the regular dividend for a total of $0.45. They also beat on both the top and bottom line with NII of $0.49 and revenue of $41.9 million. During the quarter, total investment income and net investment income grew 67% and 36% respectively year-over-year. Net investment income grew to $19.7 million from $14.5 million Additionally, they managed to increase their NAV to $14.17 from $14.07 quarter-over-year, but is a decrease from $14.22 at the end of '22.

As seen by the rise in investment income, the BDC is highly sensitive to the rise in interest rates, serving the company well, and been a plus for shareholders. To put this into context, the company has raised the dividend a total of 5 times since rates began to rise from $0.27 to current of $0.40. Furthermore, they've declared a supplemental a total of 3 times since the beginning of 2023.

{kind=link}

Risks

The biggest risk BDCs face currently are rises in non-accrual loans. These are loans from tenants that have not been paid and been on a non-accrual status for at least 90 days. Since rates have risen rapidly, several BDCs have reported a rise in non-accruals over the last few quarters. RWAY reported 0 credit losses in 2023 YTD. And with recession talks seeming to pick up recently, management expects volatility to continue in the second half of this year which has already been happening. The company plans to actively manage their portfolio due to tightening financial conditions. At the end of the quarter, RWAY only had one company on non-accrual status. If rates continue to rise and stay elevated, the BDC could see more companies placed on a non-accrual status.

Final Thoughts

Although this BDC is fairly new and unknown, the company seems to be on the right track and looks like it could be a potential long-term investment for those focused on dividends. The BDC is poised for growth in my opinion and offers investors a safe, high-yield over 12% currently. Furthermore, they have a growing portfolio that focuses on first-lien loans and a conservative balance sheet with well-laddered debt maturities. If rates do remain higher, RWAY will continue to benefit due to their sensitivity to interest rates. The company also trades at a discount to NAV which is rare currently as many trade at a premium to their NAV. Investors looking for high-income, and a potential star in the BDC space should consider adding RWAY to their portfolio.

For further details see:

Runway Growth Finance: You Really Should Consider This 12+% Yield For Your Portfolio