RWEOY - RWE Is Not Doing Enough

2023-10-16 11:55:29 ET

Summary

- Germany’s largest power generator has had a good first six months.

- Its green transformation though is progressing in fits and starts.

- Such dawdling, when competitors are charging ahead, will continue costing RWE in market value.

My initial article about RWE AG (RWEOY) was essentially a thesis about the future benefit of its transformation agenda. Since then, the company, historically Europe's second-largest emitter, has made progress on sustainability. Or so it may seem.

For the longest time, RWE was known for its coal mines and nuclear reactors. But the company has been working to shed its image of a big polluter, although not for that long yet. For investors, the change could not come soon enough.

The backpedalling on some coal exit timelines and attaching provisions on others has been disappointing, even though a boost in earnings in 2022 and so far this year. Lingering exposure to thermal generation - at least till 2030 and possibly beyond - will keep constraining RWE in terms of debt capacity, cash flows and valuation.

Financial update

After last year's bumper results, the first half of 2023 continued to impress. Group EBITDA increased from €2.1b a year ago to €4.5b, in large part thanks to outperformance by Hydro/Biomass/Gas. These flexible generation assets, in addition to Supply & Trading, are projected to deliver consistently moving forward. Adjusted net income climbed to €2.6b (H1 2022: €950m).

RWE

Another highlight is a bump-up in the renewables generation portfolio by as much as 5.1GW, most of it acquired from Con Edison's Clean Energy Businesses. This has made RWE the fourth-largest renewables player in the USA and the second largest in photovoltaics. The development pipeline has added 7.2GW, bringing the green capacity under construction to an all-time high.

{kind=link}

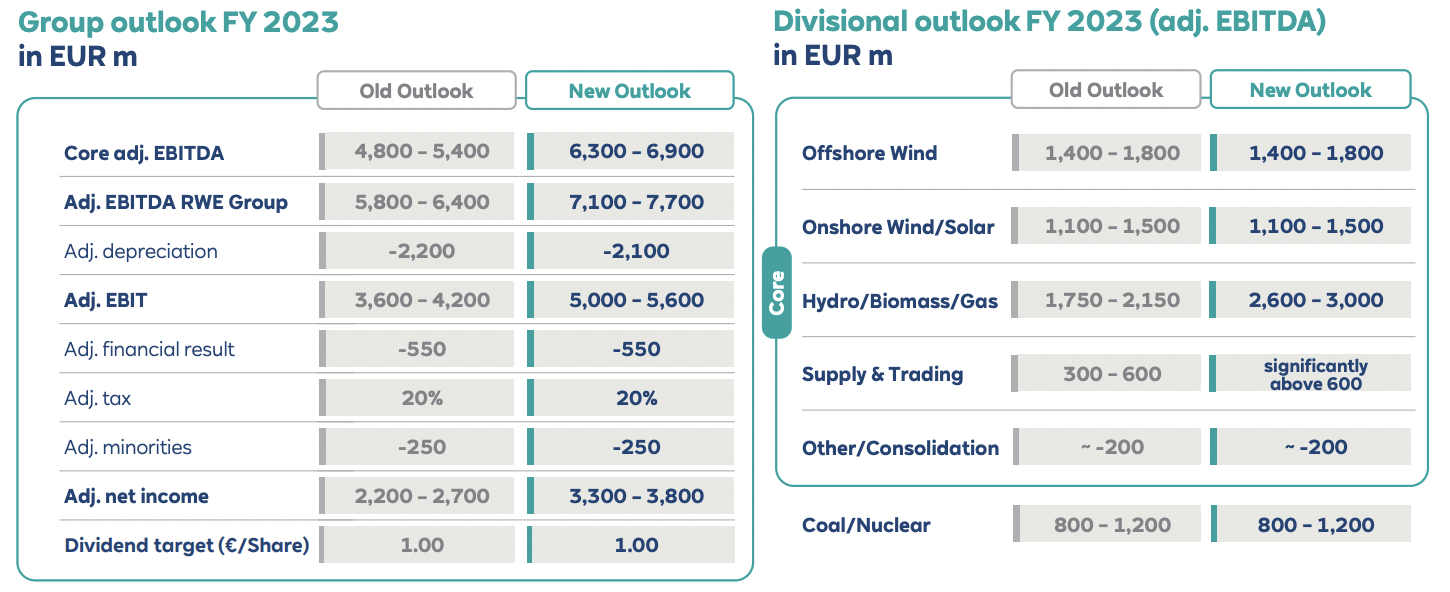

The strong performance so far has allowed the management to lift the full-year guidance for adjusted EBITDA to a minimum of €7.1b (from €5.8b previously) and adjusted net income to €3.3b (€2.2b). In the following years, however, a noticeable "normalization" in price levels is being predicted.

On the balance sheet side, RWE continues to accumulate debt to supplement funds for acquisitions. In the six months to 30 June, these included the Dutch gas power plant Magnum and JBM Solar, a UK developer. Net debt, as a result, went from negative territory (meaning more cash than debt) to €5.9b.

Although net debt is still reasonable, debt-to-equity has jumped up considerably over the past five years, from 18% to 58%. The real concern is that operating cash flow covers less than 8% of debt, even with a late boost in earnings. RWE has been scrambling to put more money into the green transition - leading to progressively more negative free cash flows - and the competition is tough.

More greening?

The big news is that coal exit from the Rhenish region of Germany - which concerns three lignite-fired plants with a combined capacity of 3.1GW - will take place eight years earlier, in 2030. There are, however, caveats: one allows the government to extend the plants' lifetime to 2033, and another to keep live two other power stations (1.2GW) that were scheduled for decommissioning in 2022.

These concessions in the name of energy security may be short-term, but they surely made RWE ever less popular. The drama earlier this year over the destruction of Lützerath , a German village adjacent to the company's Garzweiler mine, only intensified the negative rhetoric. There is some truth to the criticism.

The fact is the group's coal capacity has not changed much at all recently . Coal still generates more power than any other segment individually and delivers roughly a fifth of total revenue (excluding any extraordinary price effects). RWE remains the largest producer in the EU, according to the Global Coal Exit List .

This is in contrast to European peers with bigger ambitions. While RWE is increasing renewables capacity from 25GW to 50GW by 2030 (with an investment of €50b), Spanish utility Iberdrola (IBDSF) aims to reach 95GW (€150b) and Italian Enel 129GW (€70b). Iberdrola exited coal completely in 2017; Enel (ENLAY) will do so by 2027.

Weighed down by a legacy business, RWE has been playing catch-up, and that is not a good look for a company trying to reinvent itself in the green space.

Stock

Neither has this done any good for the stock. Valuation continues to be low, even through profitable growth periods and some price returns. The result is overpaying: at 11x EV/EBITDA , RWE bought CEB at a much higher multiple than its own.

RWE on XETRA , a trading platform by the Frankfurt Stock Exchange, is valued at 4.29x EV/EBITDA and 9.64x trailing P/E. Compare these numbers to Iberdrola's [IBE.MC] 8.01x and 14.67x respectively, and Enel's [ENEL.MI] 5.94x and 14.31x.

RWE returned -12% over the past year (-10% with dividends) underperforming German renewables and the overall market (12% and 17%). In the last three years, price has inched 0.1%, so investors are understandably upset. At least dividends have been coming, growing slowly; the present yield is lowish 2.6% (3-year forecast: 3.1%).

One minority shareholder has been particularly vocal. Activist fund Enkraft put forward that RWE could realize significant value - adding as much as €30 to the share price, currently at €34 - if the firm split off its lignite business. As long as RWE hangs on to thermal assets, it will continue to be more sensitive to investor sentiment.

Conclusion

RWE remains defensive , naturally. Admittedly, the geopolitics of energy since the events in Ukraine have really made it more difficult for the group to make good on its green pledges. But the current remission is a clear liability, for the market value as well as credit rating . The company will eventually clean up because it has to. In the meantime, expect more of the same from the stock: volatile prices and dividends with little upside potential.

For further details see:

RWE Is Not Doing Enough