RWNFF - RWE: Not The Most Common Play On Energy But A Solid One

2023-10-16 22:01:31 ET

Summary

- RWE is a large energy company and one of the 400 largest companies globally.

- I view RWE as a safe long-term investment and have specific upside targets for the company.

- I am providing an update on RWE as it enters the 3Q23 reporting period, and consider the company a "BUY" here. I update my PT for the company.

Dear readers/subscribers,

RWE Aktiengesellschaft (RWEOY) is a company I've been writing about for over a year, and invested in for about the same timeframe. This is not a large investment for me, nor is it likely to become one in the near term. But it's an interesting diversification for my utility/energy portfolio on the basis of what they actually own.

The company, after all, remains one of the largest energy companies on the planet - even if it's only the second-largest in the country of Germany. It's however also one of the 400 largest companies on the planet, with roots going back over 100 years, and I tend towards such companies because I view them as being fairly safe investments for the long term. And the long-term is where I look.

My own goal is usually owning a company for 3-5 years or more, and I have very specific upside targets I'm looking for. Each company I buy comes with a share price target, and when I expect this to materialize. Things can change, but there should be a reason for theses to change.

In this article, I'm going to provide you an update going into the 3Q23 period, which we're actually closing in on here in terms of reporting.

RWE - What remains of legacy coal?

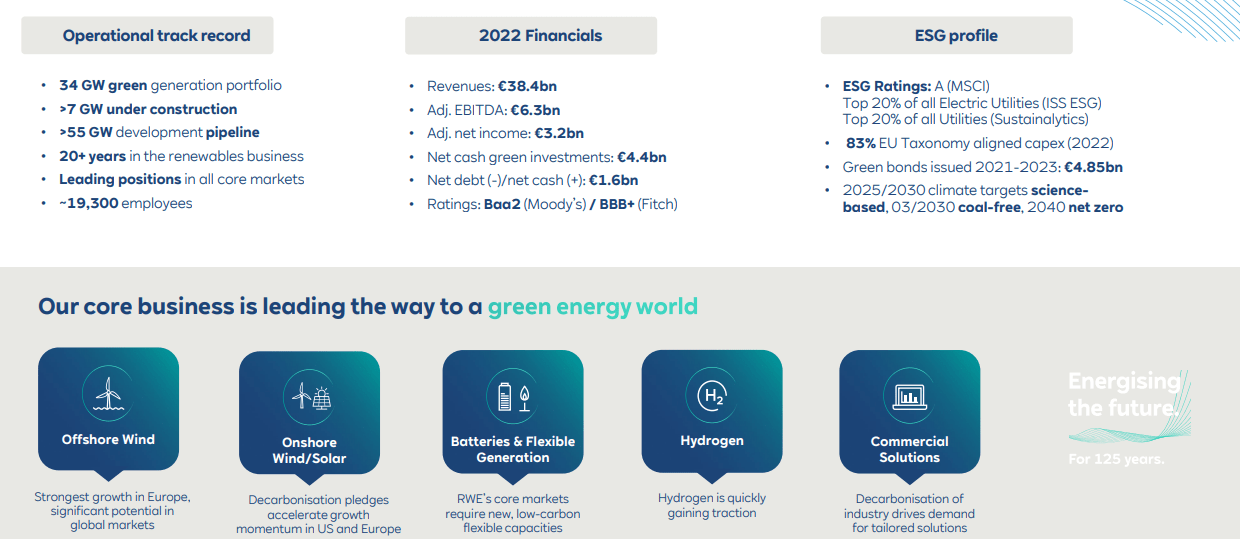

Just because the company is primarily a coal player in the legacy field, does not mean that the company does not do renewables. RWE is actually fairly heavy in renewables and is about to go even deeper. What was once considered RWE, even by people with knowledge in the industry, is no longer what the company "is" today. The company has a very attractive set of renewable assets that seems to be growing year over year.

RWE, as odd as it may sound for someone who knows where the company "came from", has become a market leader in US solar as well as US Wind/Solar.

RWE is still a lot of coal - but the current plan, which by the way lines up with another utility in Germany that I've been writing about, Uniper ( OTCPK:UNPRF ), has already decided to leave coal behind in 2030 at the latest. This sort of concerted effort amongst several market players makes it unlikely that there be a significant variance or difference from this plan.

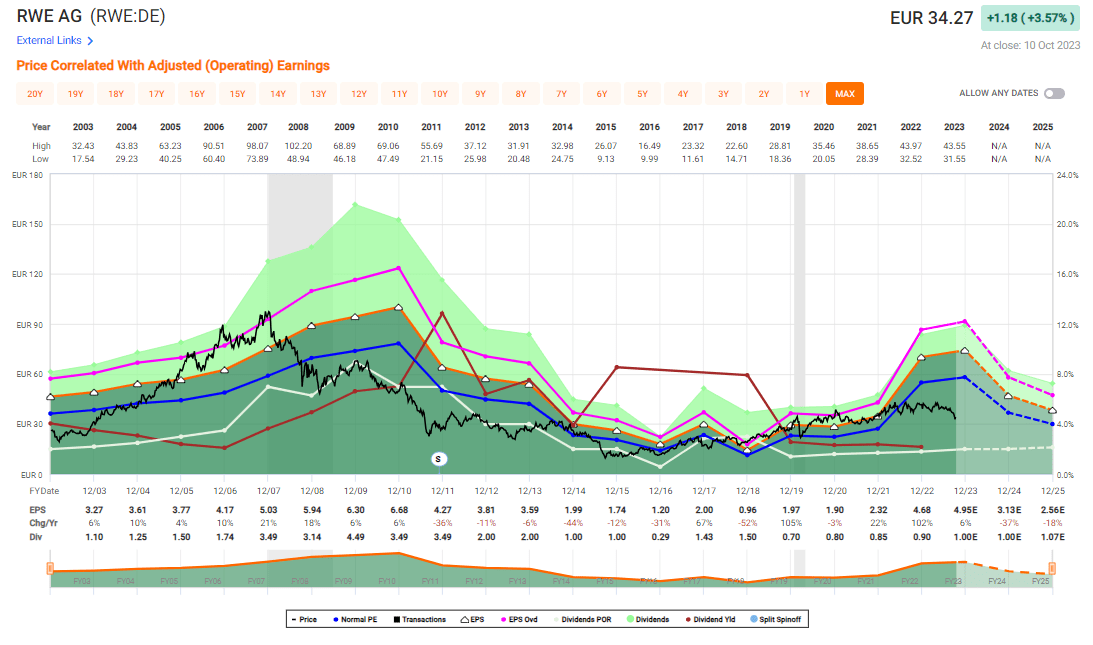

This company is safe. Fundamentally at least. I'm not talking about a high yield, because RWE does not offer that. The company's current yield is a whopping 2.63%, which makes it the lowest-yielding utility I currently hold a position in. The last 20 years of performance for RWE makes it clear why the company isn't exactly an investment favorite. Let's just say that it's been through its share of changes.

{kind=link}

Every relevant piece of investor information is focused on the "transition to green". It's the first picture you're met with if you visit the company's homepage.

{kind=link}

The company's focus is on being different in 2020-2040 than it was from 2000-2020, and given what we see above, this would obviously be a welcome change. As it stands, you would have been better off being a bond investor in RWE , raking in coupons, as opposed to taking the loss that common share investments would have given you.

That's not anything against bond investors by the way - I invest in bonds myself. What I'm saying is that you need to know at what level of the capital stack you invest in, and different companies have different risk profiles and opportunities here.

For RWE, I believe an investment in the common is no longer as abysmal an idea as it once might have been.

Why is that?

Because the company's plan is working.

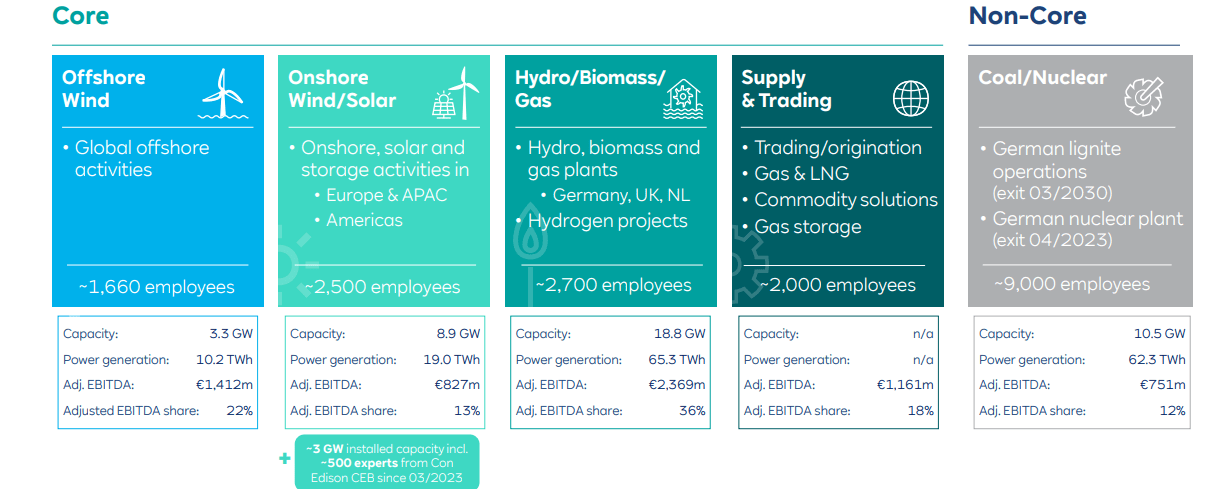

The business model is already fully in line with the new targets. It's #2 in Global offshore, #2 in US solar, #4 in US Wind/solar, #3 in UK/Wind Solar, and #4 in Europe Wind/Solar.

While the entire renewable sector is currently under pressure because project IRRs are no longer making sense due to changed interest rates and cost of debt, I view this as nothing less than an opportunity to buy assets at a discount.

RWE is one of those asset holders.

{kind=link}

You can see that the company is crystal-clear in its communication. Coal/Nuclear is out. All the way to the right over there, despite the fact that it has almost as many employees as the other sectors have combined at this time, and over 10.5 GW capacity.

Net zero is a target until 2040 or earlier. RWE is perfectly positioned for its green tech and has a strong market presence in growing industrial markets. Despite current challenges in renewables, the company is putting its money where its mouth is. €50B worth of gross investments are planned until 2030 to bring this plan to fruition.

To put it in another way, RWE intends to add more than 2.5x as much capacity in net additions than is being lost by the coal assets being taken offline.

Where I'm seeing risks isn't in the execution of that. I believe RWE will actually manage that pretty well. I'm just worried that the internal rates, or the actual rates of return both for the company and for shareholders won't be as great as we expected or as the company expected. The reason is that it's exactly this we're seeing in other companies that recently have taken significant hits on renewable project returns, including leading European renewable businesses like Orsted. What needs to happen here, and what's obviously already happening is for the companies involved in the projects to charge or calculate in accordance with a 5-6% interest rate/cost of capital. The legacy projects are the issue here - and RWE is moving forward.

{kind=link}

This business will accelerate the non-EU growth that's estimated to take RWE to the next level. We're expecting a 500+ MW buildout in USA per annum, with a 24 GW combined US development pipeline between Solar, Offshore wind and battery with a clear weighting towards solar, expecting a green portfolio that looks like this.

RWE IR (RWE IR)

This is, on paper, a very attractive portfolio and upside. And perhaps most important or interesting, is that this M&A and organic growth is already fully-funded at this particular time.

{kind=link}

With the acceleration of the company's decarbonization, the company is actually leaving coal behind 8 years earlier than expected. This is an agreement with the federal government as well, which entails a full exit from Lignite. Only in a period of 3 years, the company's ESG ratings and metrics have seen superb improvements.

Company fundamentals, speaking to net debt, is now at €5.9B, not worrying, with 37% bonds, 15% commercial paper, and 48% to banks, with 96% denominated in Euro.

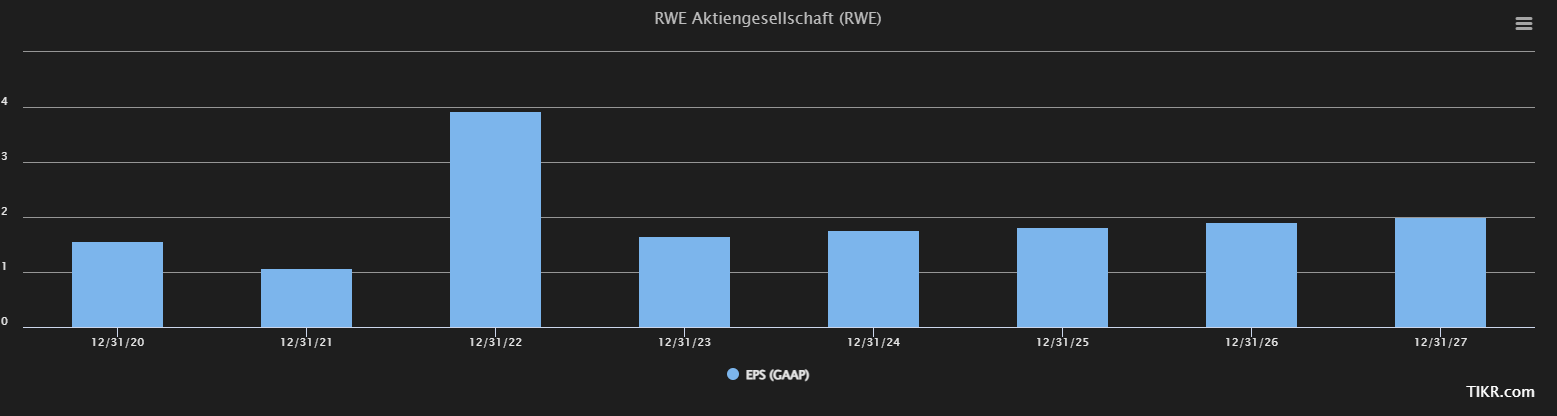

One of the problems we're currently facing is comps. 2022 was a very strong EPS year. 2023E is going to see a significant decline, and the step-up is going to be slow - very slow. But I do believe we're going to see solid improvements over time here, and with a much better mix than RWE has seen at any point in the last 40 years.

{kind=link}

Let me show you what sort of valuations are implied by this sort of trend and what RoR you can expect from the company here.

RWE - A lot to like, but only for the long-term

RWE is a very long-term play, but it might be one of the safer long-term plays in renewable energy that exists, given the company's very clear plan. We have a €25B market cap focused on becoming one of the leading renewable players out there, and this company is now trading at a blended P/E of 7x, based on current adjusted earnings (Source: FactSet).

Valuation targets for the company from other analysts are considered it far more favorable. Out of 18 analysts, 15 are at "BUY" or equivalent, and not a single analyst considers RWE to be a "SELL" or an underperformer here. The low-range target is €45/share, which means that at €34/share, we're more than €10 below the current lowest estimate for RWE. The high target is €59, and the average comes to €52/share. That's an upside of 54% based on the current share price.

I would not go that high.

Based on discounting for unfavorable return trends in the renewables sector, I would discount the company by 10-15% here, but anything more than that would be disingenuous for a company that based on a projected FCF analysis might be worth, at least in theory, over €90/share (Source: GuruFocus). A discount of 15% to the average comes to €44/share, which I consider to be a fair change to my previous PT and takes into account the potential lower RoR and ROIC from legacy projects.

I believe RWE is a superb potential investment - that is why I invest - but it's one for the very long term. 5 years at the very least.

Thesis

- RWE is among the class-leading renewable companies on earth, though with a still-existing legacy portfolio with exposure to lignite and other non-friendly (in environmental terms) fuel. The company is working to reduce this, and exit coal by 2030. It's BBB+ rated, has a well-covered yield of over 2%, and is set, as I see it, to stabilize its earnings in the next couple of years.

- Because of this, I view RWE as a "BUY" with an appealing conservative PT of €44/share for the native, updated for October of 2023 - below even the analyst average, but still enough to interest potential investors.

- I own RWE here - and I intend to slowly build more as time passes and earnings come in.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I even view the company as cheap now, which means RWE fulfills every metric I look at for businesses to invest in.

For further details see:

RWE: Not The Most Common Play On Energy, But A Solid One