XLK - RWO: Underplaying Commercial Real Estate's Growth Potential

2023-08-10 08:27:26 ET

Summary

- Certain areas of commercial real estate like warehouses and data centers had a strong first half and are well-positioned for growth in the coming periods.

- Macroeconomic trends like economic uncertainty and downturn have made commercial real estate a risky domain, yet competition within the space continues to grow.

- I rate RWO a sell, as its top holdings are already well-diversified and capable of greater momentum than this ETF itself.

The United States real estate market fought an uphill battle during the first half of 2023 amid rising interest rates and economic uncertainty . Despite this struggle, certain areas of real estate managed to gain more momentum than others, and I think this trend still has the potential to invigorate before the end of the year. Relatively successful sectors include but are not limited to residential properties like multifamily properties . In regard to residentials, factors like falling mortgage rates , strong demand from millennials , and a limited supply of homes are contributing to rising home prices. Office and retail properties haven't had as much luck, as remote and hybrid work continuously prove effective, dampening the need for certain physical workspaces. Ultimately, the United States real estate sector has struggled to keep up with the broader market so far this year.

The SPDR Dow Jones Global Real Estate ETF ( RWO ) could in the coming periods allow investors to hedge downturn in the United States markets while also geographically diversifying their real estate exposure. As seen below, RWO has slightly outperformed the Vanguard Real Estate Index Fund ETF Shares (VNQ), one of RWO's U.S.-focused alternatives.

As opposed to rental properties, real estate investment trusts (REITs) provide investors with more passive, remote income, allowing them to invest overseas with much less trouble. However, RWO struggles with momentum compared to its top holdings, namely Prologis (PLD), Equinix (EQIX), and Public Storage (PSA). Investors might therefore achieve greater returns without additional expenses by avoiding RWO. I rate this ETF a Sell.

Strategy and Holdings Analysis

This ETF tracks the Dow Jones Global Select Real Estate Securities Index and uses a representative sampling technique. This index consists of REITs and real estate operating companies (REOCs). Individual holdings must be of at least $1 billion market capitalization and, despite being rebalanced quarterly, are removed if they fall below this threshold. RWO's portfolio is weighted toward the commercial real estate sector, including office, retail, and industrial properties. This ETF also contains residential properties but in lesser quantities than peers like the iShares Residential and Multisector Real Estate ETF ( REZ ) and the SPDR S&P Homebuilders ETF (XHB). Securities within RWO are all of investment-grade credit, reducing the risk of default among individual holdings.

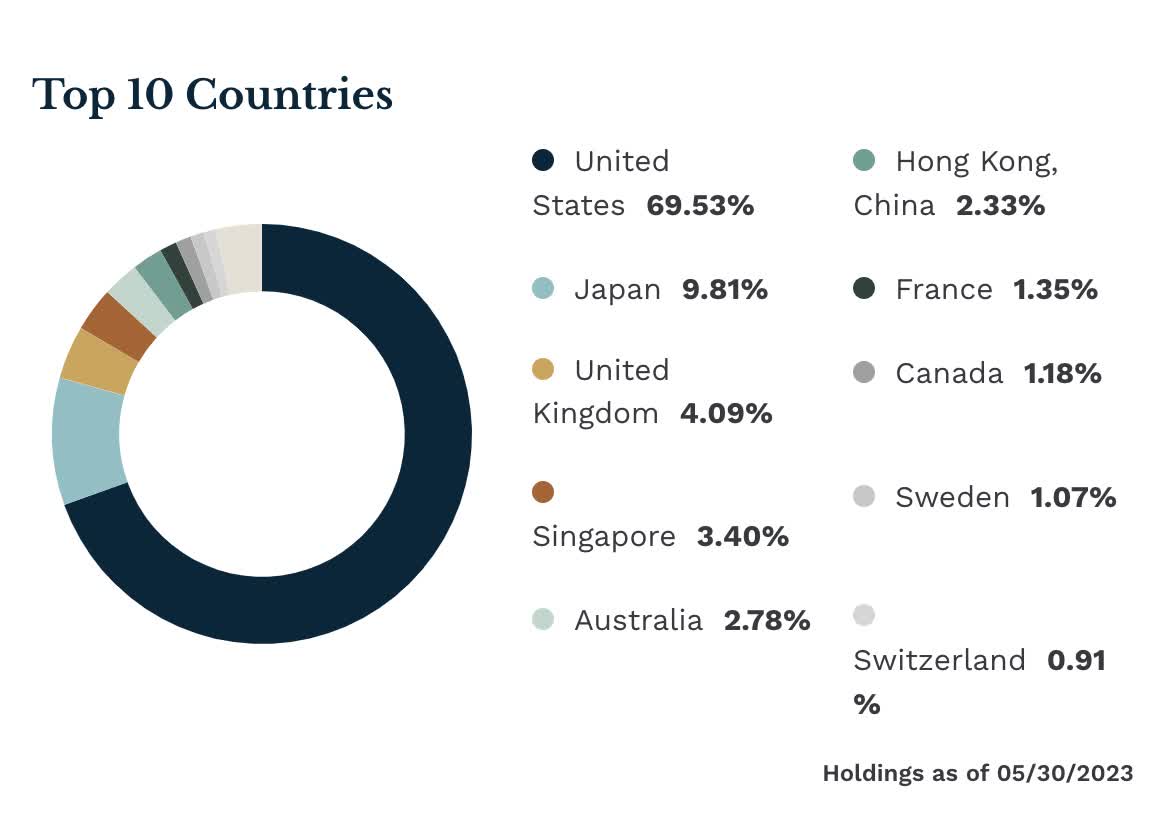

RWO invests primarily within the United States, which accounts for almost 70% of this fund's geographical breakdown.

{kind=link}

The top 10 holdings in this ETF account for just over a third of the whole portfolio, with the top 5 comprising roughly a quarter.

{kind=link}

Finding Momentum In RWO

PLD and EQIX have this year performed significantly better than RWO, EQIX even delivering greater returns than the S&P. PSA exhibits a similar lack of momentum to RWO, but I believe could still encounter some important catalysts further on, which are discussed in greater detail in the following sections.

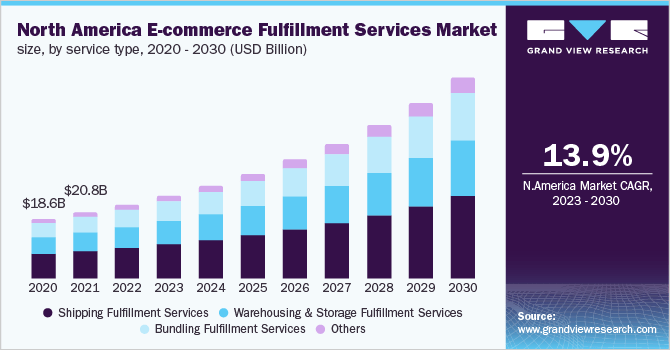

Prologis is well-positioned to benefit from growth in the warehouse market. Such growth stems primarily from expansion in spaces like e-commerce , omnichannel retail , and third-party logistics (3PL). Furthermore, EQIX is likely to capitalize well on growth in cloud computing , artificial intelligence ((AI)) and the Internet of Things (IoT) given its strong focus on data centers. I dive deeper into these particular industries in my piece on the Technology Select Sector SPDR Fund ETF (XLK).

BlueWeave Consulting

{kind=link}

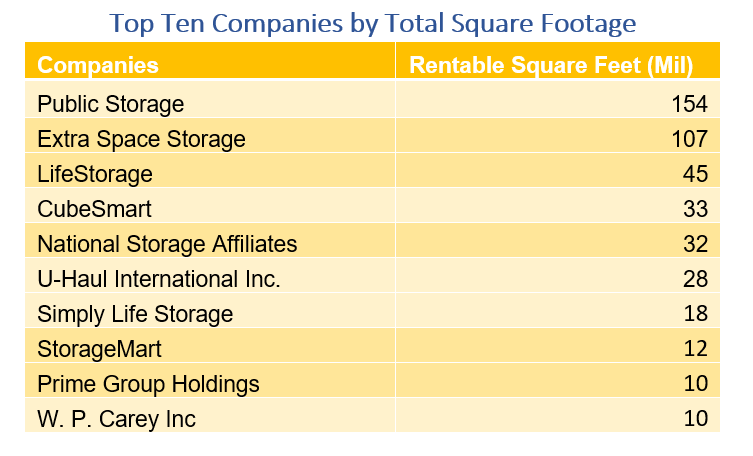

Though PSA hasn't displayed the same growth as PLD and EQIX, this company is likely to benefit from trends like shrinking apartment sizes in the United States and the increasing popularity of personal storage units as investments . Personal storage units have become quite popular this year as they offer low operating costs, decent profit margins, and economic durability during times of uncertainty. As seen below, PSA is a leader in its realm.

{kind=link}

Future Considerations and Possibilities

Declining Demand in Office Spaces

Following the COVID pandemic, office spaces incurred a decrease in Demand For Office Space Could Fall 13% By 2030 -And That's Not The Severe Forecast when many employees shifted towards remote work. In 2023, this trend has held up, and rising interest rates and tighter Concerns Grow as Tighter Lending Threatens Commercial Real Estate practices have only made it harder for those in the office spaces REIT domain.

NAIOP

Commercial Real Estate Competition

Commercial real estate investing has proved quite lucrative during the past few years, leading to augmented competition for the best properties on the market. As more investors enter this space, price volatility could worsen, while rents and occupancy rates also decline for the properties held within RWO. Though more activity could catalyze growth and increase the amount of cash flowing through this space, finding value in this space could become more difficult in the near future.

{kind=link}

Conclusion

RWO's portfolio has shown quite powerful towards the top, but the general fund lacks momentum. Since REITs such as PLD, EQIX, and PSA hold multiple properties themselves, this ETF's extra layer of diversity likely has more costs than benefits. Therefore, investors may find more momentum in individual REITs. I rate RWO a Sell.

For further details see:

RWO: Underplaying Commercial Real Estate's Growth Potential