RYAAY - Ryanair: Back To Profitable Growth

Summary

- Ryanair is back to profits thanks to the Christmas holidays.

- The last three months net profit reached €211 million.

- 2023 guidance was confirmed and so we confirm our valuation.

Yesterday, Ryanair ( RYAAY ) ( RYAOF ) released its quarterly numbers. Despite the negative stock price reaction, here at the Lab, we positively welcomed the three months account. As already mentioned, in Q3, the low-cost operator returned to profit. In the three months just ended, the Irish airline delivered an adjusted profit after tax of €211 million against a loss of €96 million versus the 2021 same period and exceeding the pre-COVID-19 result of €88 million. The figure also was above the group's expectations of €200 million and was supported by air traffic between Christmas and New Year's and by its cost containment. Looking at Wall Street analyst expectations, despite the goals achieved, it appears there is still work to be done.

Q3 Results analysis

Looking at the company's P&L, the company closed its third quarter with top-line sales of €2.3 billion which were up by 57%. The group also accelerated capacity compared to the pre-pandemic period, operating at 112% of capacity. In detail, the most significant gains were recorded in Italy (from 26% to 40%), Poland (from 27% to 38%), Ireland (from 49% to 58%) and Spain (from 21% to 23%). Our most devoted readers know that the Italian landscape was one of our key supportive catalysts.

Ryanair Q3 in a Snap

Source: Ryanair Q3 press release

As already mentioned, Ryanair expects a loss in the fiscal year's fourth quarter due to the absence of the Easter holidays in March. Furthermore, it appears that some equity research analysts view the increase in operating costs with suspicion. The operating costs item grew by 36% to $2.15 billion on a yearly basis, due to inflationary pressures from rising wages and aviation fuel. Without considering the increase in fuel prices, operating costs would still have grown by 26% due to more traffic growth. However, we believe that Ryanair is on the right track to regaining pre-COVID-19 demand levels and normalizing cost spending.

Conclusion and Valuation

Concerning our buy case recap , we reported the following:

- Ryanair is raising air ticket prices at a lower pace than competitors (thanks to its Gamechanger strategy competitive advantage). In detail, Q3 fares were up by 14% versus 2019 numbers;

- The company's investment in fuel-efficient aircraft should pay off. B737 fleet reached 84 aircraft. As a reminder, the new Gamechanger fleet consumes 16% less fuel and has 4% more seats;

- With specific investments for a total amount of €200 million, Ryanair expects to reduce fuel consumption by 1.5% in the remaining owned fleet;

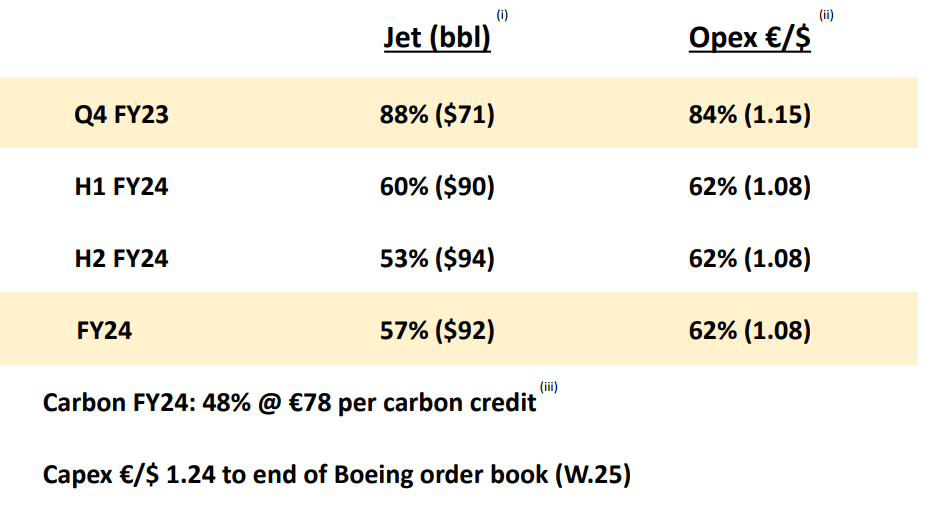

- The company's jet fuel hedged is approximately 88% with FX also covered. To quote the company's words, these strong hedge positions help insulate the low-cost operator " from spikes in fuel prices and give our Group airlines a significant cost advantage over our EU competitors for the remainder of FY23 and into FY24" (Fig 1) ;

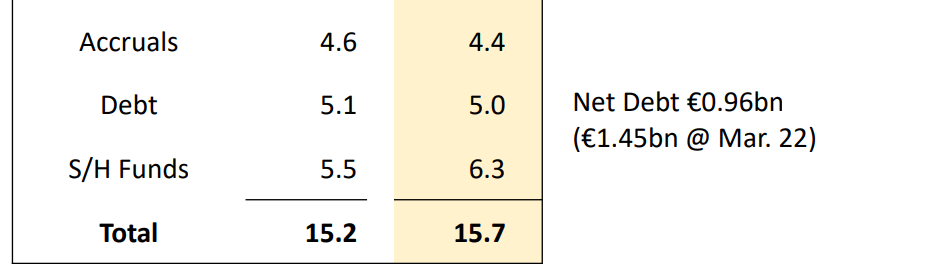

- The European low-cost champion has the strongest balance sheet within the industry. Credit ratings are positive, and almost all of the company's fleet is fully owned. Despite growth CAPEX, net debt stood at €0.96 billion from €1.45 billion and the company aims to a net zero debt position by April 2024 (Fig 2);

- The group confirmed the 2023 guidance with an adjusted net profit between €1.33 and €1.43 with travelers’ numbers at 168 million. In the quarter just ended, 38.4 million passengers flew with Ryanair compared to 31.1 million in the same period of 2021;

- We are already ahead of Wall Street estimates, with the latest positive numbers, in line with our previous expectation, we reiterate our target price at €19 per share .

{kind=link}

Fig 1

{kind=link}

Source: Ryanair Q3 results - Fig 2

For further details see:

Ryanair: Back To Profitable Growth