RYAAY - Ryanair Is Winning Buy Confirmed

2023-07-25 08:00:40 ET

Summary

- Thanks to the Gamechanger Strategy, Ryanair is winning market share while increasing profits.

- Best-in-class profitability with a solid balance sheet (able to support the company's CAPEX growth).

- A summer season rebound coupled with higher winter bookings. Our buy is then confirmed.

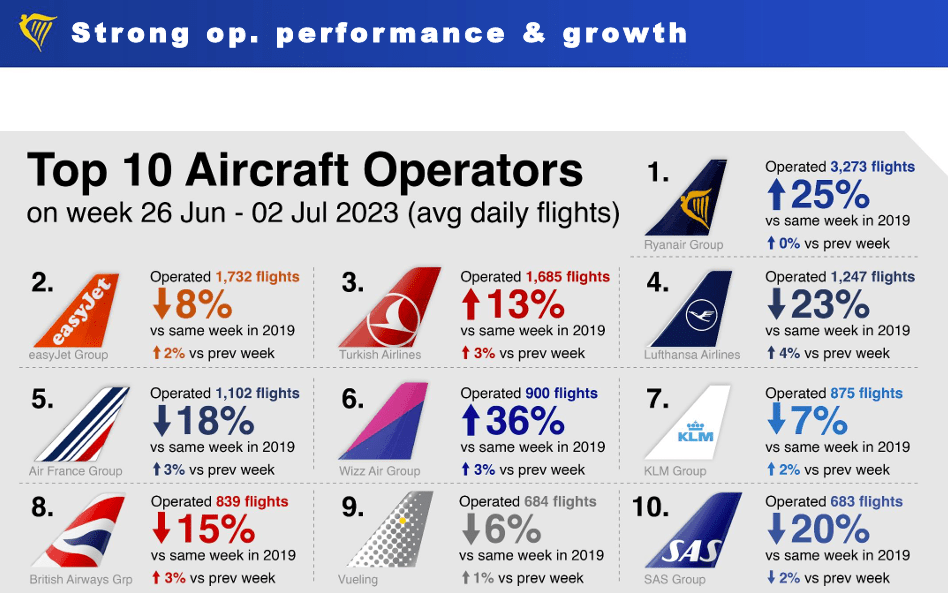

Ryanair Holdings plc ( RYAAY ) just released its Q1 trading update. Last week, we already commented on EasyJet's results with a supportive view for this upcoming winter. Here at the Lab, we have a long-standing buy rating in the Irish low-cost operator. This is based on MACRO to MICRO factors: 1) a " Back To Profitable Growth " path; 2) the company's " Gamechanger Strategy " on a CAPEX development plan to increase seats by 4% and reduce fuel consumption by 16%; 3) air traffic growth that is getting closer and closer to pre-COVID-19 levels; 4) best-balance sheet within its peers; and 5) higher market share penetration (Fig 2).

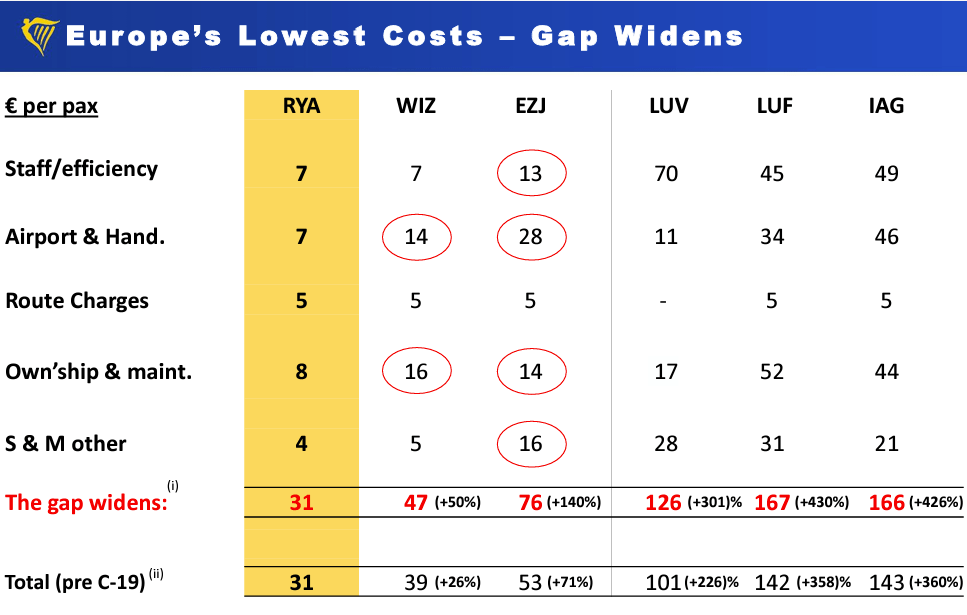

Looking back, providing a supporting buy rating was an excellent call. Indeed, during the period , Ryanair recorded a positive stock price appreciation of more than 46% (Fig 1). In a nutshell, we consistently reported how the company is adding " more seats," consuming "less," and having "higher capacity loads." This led to a competitive advantage with " lower tariffs and more clients, bringing more profit " in a continuous positive circle (Fig 3). The just-released numbers go in this direction and fully confirm our thesis.

{kind=link}

Fig 1

{kind=link}

Fig 2

Ryanair best-in-class profitability

{kind=link}

Fig 3

Q1 Results

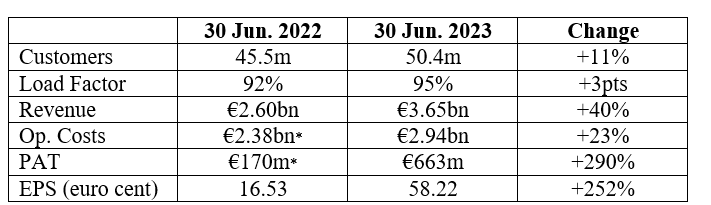

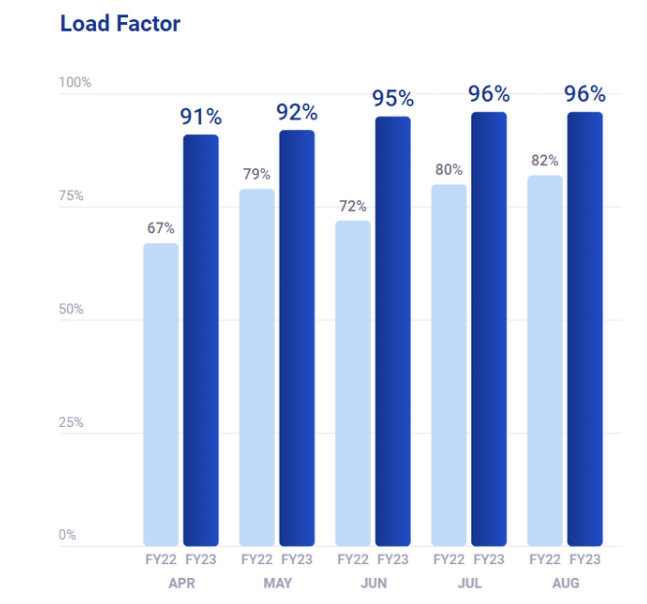

Despite the Ukraine war, the Irish low-cost operator benefited from the Easter holidays and closed its Q1 with a growing net profit of €663 million. In numbers, the company reported top-line sales of €3.65 billion (with a plus 40% on a yearly basis) and passenger growth of 50.4 million (plus 11%). This positive performance was recorded thanks to 1) higher ticket prices with an average fares increase of 42%, 2) higher ancillary revenue signing a plus 15%, and 3) three new bases with over 190 additional routes. Key to report is the company's load factor evolution which increased from 92% to 95% (Snap of 2022 vs 2023 performances).

{kind=link}

Fig 4

{kind=link}

Fig 5

Going back to our investment thesis, we positively reported the following:

- The EU airlines are in a consolidation process (ITA Airways with Deutsche Lufthansa), and the TAP sale is underway. There is a CAPEX capacity growth constraint for the next four years, and in our estimates, Ryanair will likely increase market share penetration. This is also based on consumer willingness to travel despite inflation and rising costs;

- Even with a modest cost increase, the company has further enlarged its competitive cost advantage over its closest European competitors. This is remarkable, given the higher operating costs and pandemic outbreaks (Fig 2);

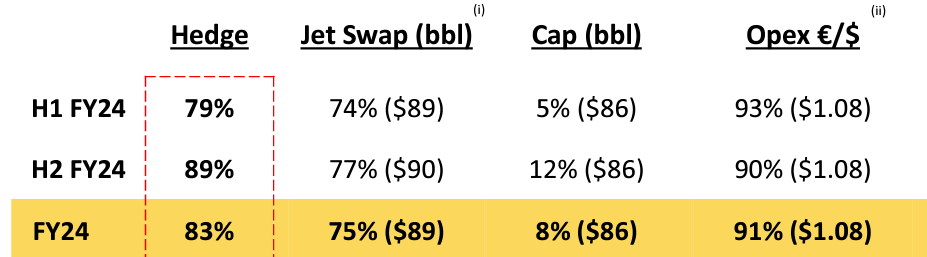

- The company hedged in place for almost 83% of its fuel consumption for the Fiscal Year 2024 (Fig 6) and also has downside protection on its CAPEX aircraft order book;

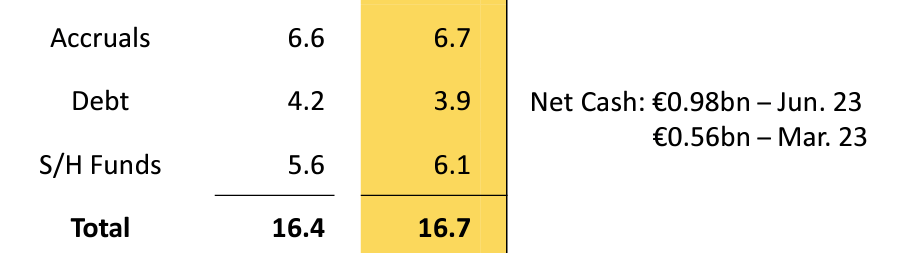

- And again, with the supportive Q1 release, the company's balance sheet is excellent. BBB+ credit rating with a net cash position of €0.98 billion from €0.56 billion in March end (Fig 7). The company will repay its €750 million bond in August and has cash resources for its 2024 CAPEX.

{kind=link}

Fig 6

{kind=link}

Fig 7

Conclusion and Valuation

On a negative note, Ryanair now forecasts a reduction in traffic growth from 185 million passengers (+10%) to approximately 183.5 million passengers (still up 9% on a yearly comparison). This is lower than expected and is mainly due to Boeing delays . Despite that, the cost gap with competitors continues to widen, and even considering wage inflation at €2 in staff cost (Fig 2), during the Q&A analyst call, Ryanair's CEO anticipates fuel savings of €1 billion if oil prices continue to fall. Regarding Q2, Ryanair reported solid bookings with higher fares than last year. Therefore, here at the Lab, we anticipated a net income of at least €700 million with an H1 profit estimate of €1.36 billion. H1 EPS reached €1.11, and considering a worst-case scenario of H2 €0.5, we arrive at a valuation of €19 per share, valuing Ryanair in line with its P/E historical average (12x). With a supportive outlook for the Winter recently confirmed by easyJet and best-in-class profitability, we confirmed our target price , maintaining a buy rating.

For further details see:

Ryanair Is Winning, Buy Confirmed