RYAOF - Ryanair: Seeing New Heights In The Post-Pandemic Era

2023-12-14 13:27:23 ET

Summary

- Ryanair’s revenue and EBITDA have grown impressively. The company operates an innovative business model that has allowed for aggressive market share growth and limited competitive pressures.

- We expect a continuation of its trajectory, as its cost model delta to peers has widened following an extended period of inflationary pressures.

- The company’s recent performance has been impressive, with double-digit revenue growth and margin improvement. Macroeconomic conditions remain an uncertain factor in its near-term trajectory.

- Ryanair is significantly outperforming its peers, with impressive margins and a materially higher ROE. The company’s financials do not align with its industry. We expect distributions to return soon while capex expansion remains.

- Ryanair is trading at a deep discount to its historical average, and even its peers, which implies significant upside in our view (>30%).

Investment thesis

Our current investment thesis is:

- Ryanair (RYAAY) is positioned well for long-term success. Its conservative capital allocation and strong business model have allowed the business to return to “business as usual” post-pandemic rapidly, at a time when its peers are struggling and raising debt. This will allow the company to widen its competitive position and operate flexibly based on market conditions.

- This should allow for market share growth and margin appreciation, which at its FCF conversion will mean industry-leading returns for shareholders. Despite this, the company is trading at a significant discount to its historical average, implying impressive upside.

Company description

Ryanair Holdings plc is a leading European low-cost airline headquartered in Dublin, Ireland. Founded in 1984, the company has grown to become one of the largest and most successful low-cost carriers in the world. Ryanair operates more than 1,800 flights daily and serves over 200 destinations in 40 countries.

{kind=link}

Share price

Ryanair’s share price performance is unbelievable given its industry, with market-comparable returns during the last decade. The airline industry has materially struggled and is notorious for destroying shareholder capital, with Ryanair seemingly the exception. This is a reflection of its revolutionary business model and market share growth.

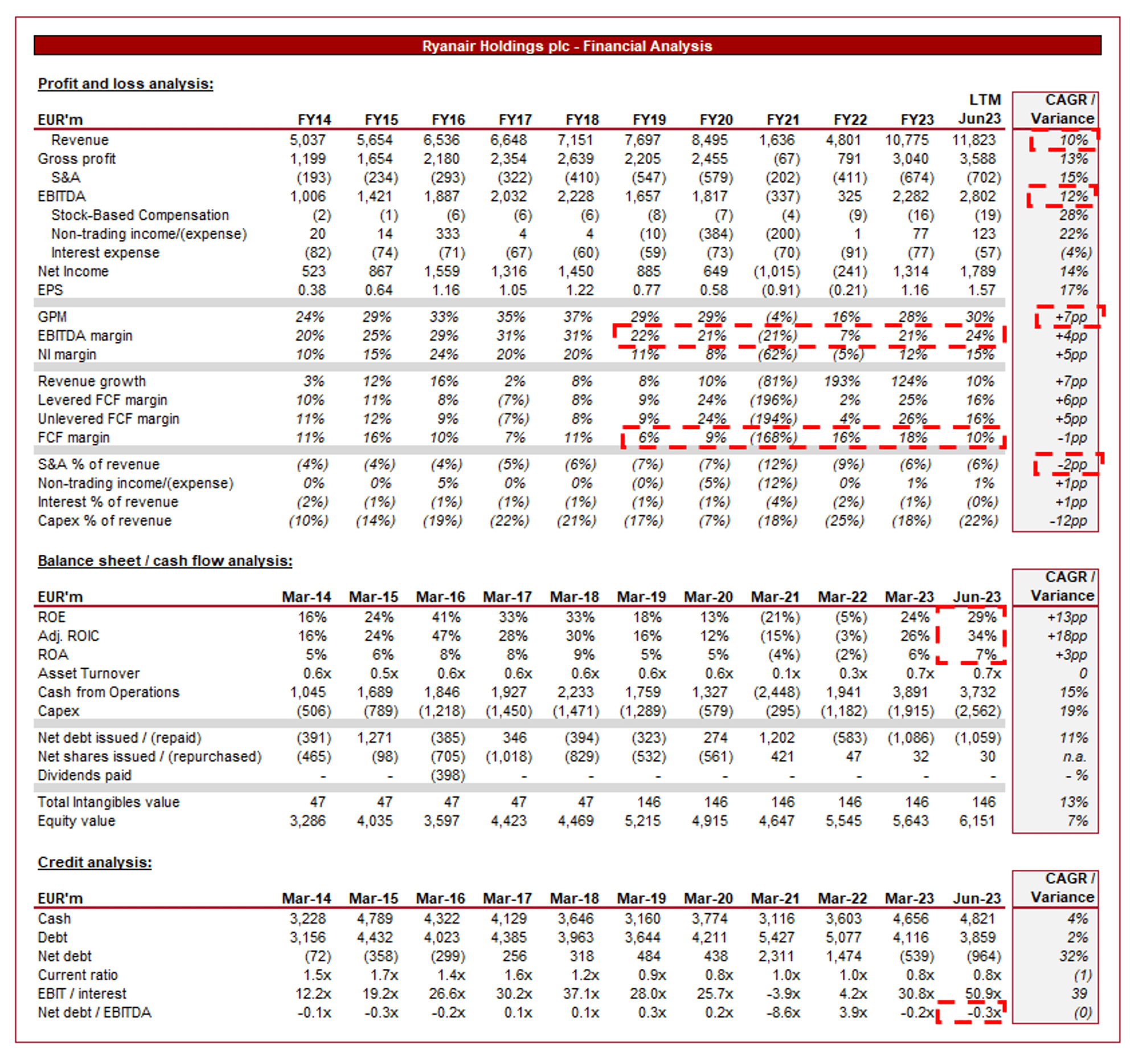

Financial analysis

Ryanair financials (Capital IQ)

{kind=link}

Presented above are Ryanair's financial results.

Revenue & Commercial Factors

Ryanair’s revenue has grown impressively, with a CAGR of +10% during the last decade. In conjunction with this, EBITDA has grown +12%, underpinning its fantastic trajectory.

Business Model

Ryanair operates on an ultra-low-cost carrier model. It focuses on reducing operational costs to the bare minimum. This includes flying to secondary airports, quick turnaround times, high aircraft utilization, and fuel-efficient aircraft. By keeping costs low, it can offer incredibly competitive ticket prices. This is an approach taken by many but not to the degree and success of Ryanair, allowing the company to differentiate itself through pricing. The company has assessed every facet of its operations for cost-cutting measures and drills this heavily into its employees. Michael O’Leary, Ryanair’s CEO, famously suggested (possibly in jest) that Ryanair should charge passengers for toilet use , playing on its reputation and ability to monetize.

Ryanair primarily operates point-to-point routes, bypassing hubs. This allows for direct flights between smaller airports, reducing travel time for passengers. It's a model that caters to travelers looking for convenience, partnering well with its low-cost approach. The business is essentially a no-nonsense operator.

Ryanair also maximizes ancillary revenues through various services like priority boarding, in-flight refreshments, and seat reservations. These additional services allow the business to upsell on lower ticket prices, that are used to initially win customers.

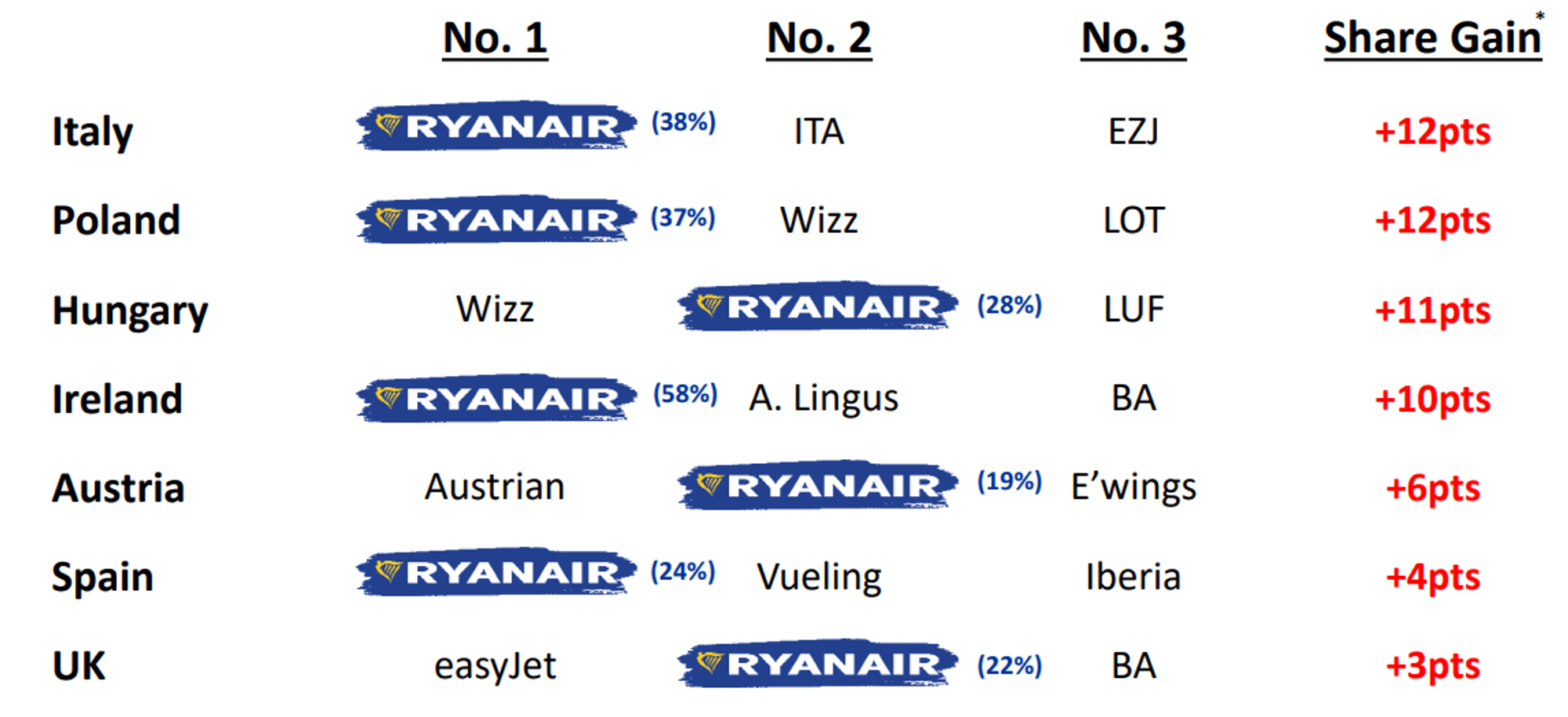

Ryanair has strategically expanded its route network, principally in Europe, targeting both primary and secondary airports following market share growth. By being the dominant player in many regional airports, it often enjoys favorable agreements and incentives, further reducing operational costs.

This has allowed Ryanair to rapidly gain market share across Europe, which it continues to improve.

{kind=link}

Given the developments in the last decade, we do not believe Ryanair’s competitive position can be challenged. The company’s techniques, although not proprietary, are not easily replicable and the company has sufficient scale and managerial excellence that replication would no longer be sufficient anyway. Ryanair also benefits from floundering competition. easyJet ( EJTTF ) and Wizz Air ( WZZAF ) are performing well but beyond this, others are struggling to keep up. IAG ( ICAGY ) and Lufthansa ( DLAKF ) are stuck in between price and quality, while ITA and Iberia lack comparable scale.

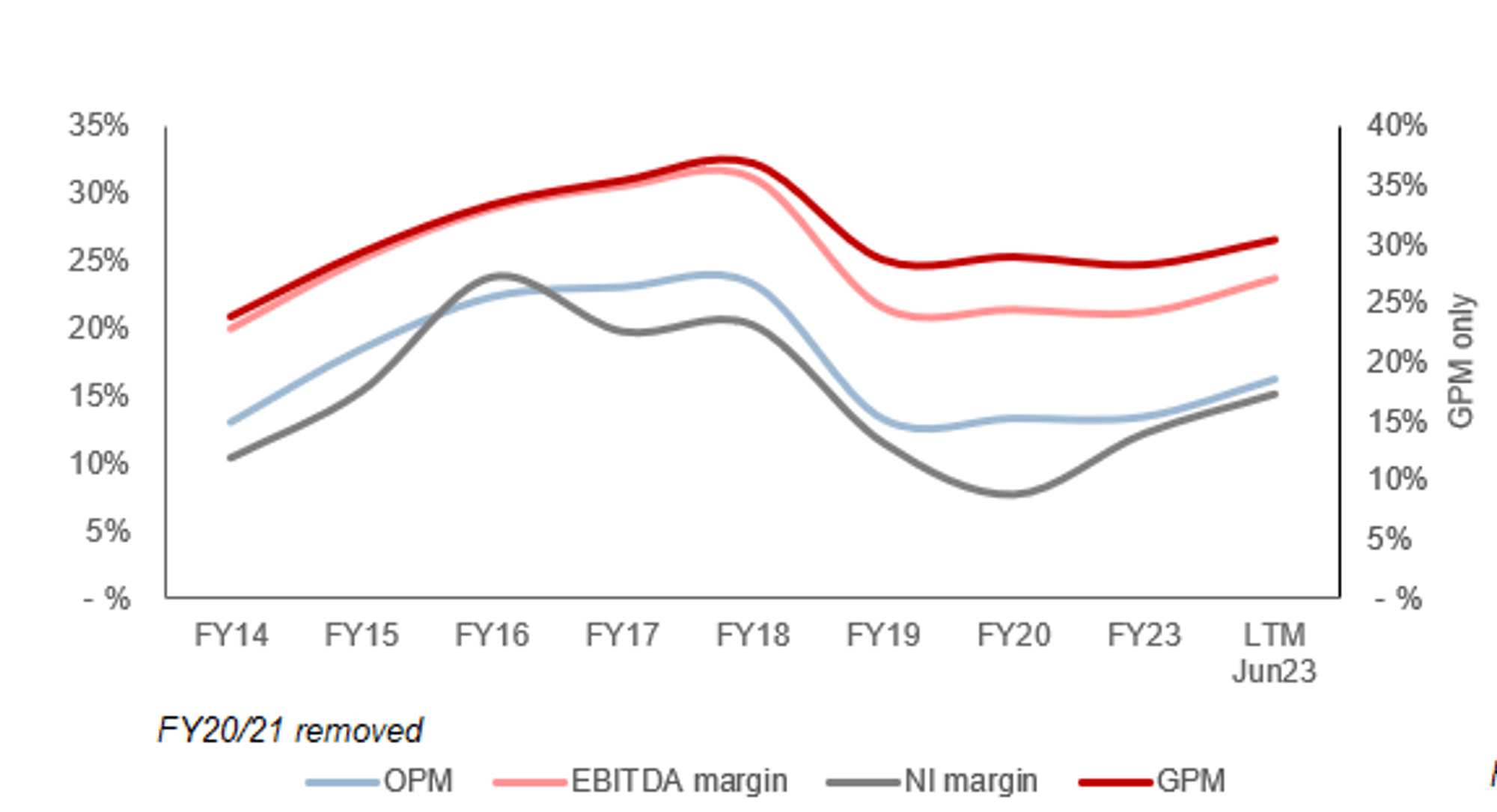

Margins

{kind=link}

Ryanair’s margins have trended positively throughout the last decade, only derailed by the pandemic. The company is currently on a rapidly improving trajectory, although we believe it will be difficult to return to its FY17-FY18 level.

Competition has increased since this period, owing to concerns about customer retention and weak demand post-pandemic. Further, the industry has experienced material wage inflation with pilots, following historically depressed compensation. Although Ryanair has been less impacted than others, it has agreed to consistent pay increases with various geographical pilot groups .

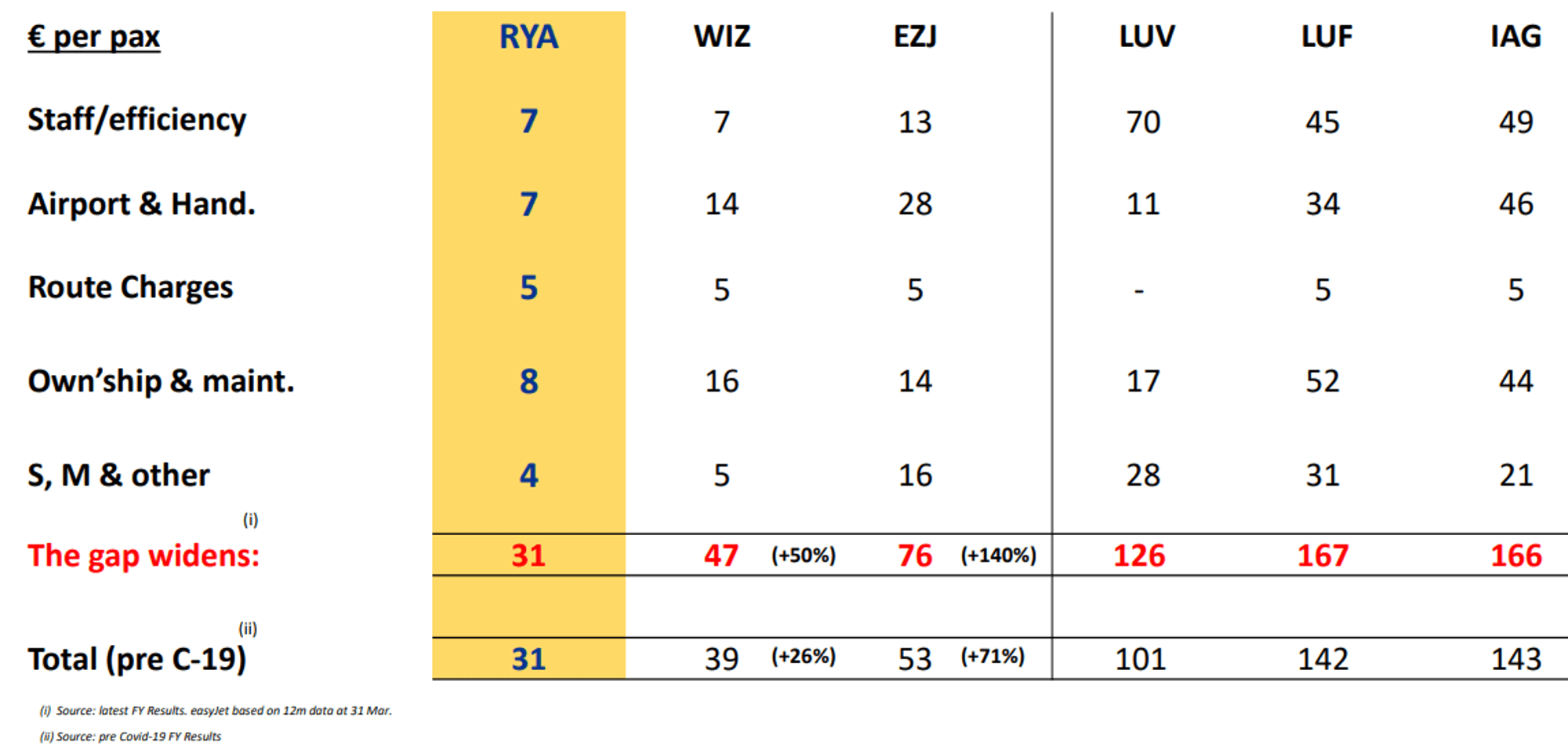

This said, the company’s relative performance is where it shines. Ryanair has continued to widen the gap between itself and its directly comparable peers. Not only is this good for investors but its ability to maintain its growth trajectory, as the company can continue to price aggressively.

{kind=link}

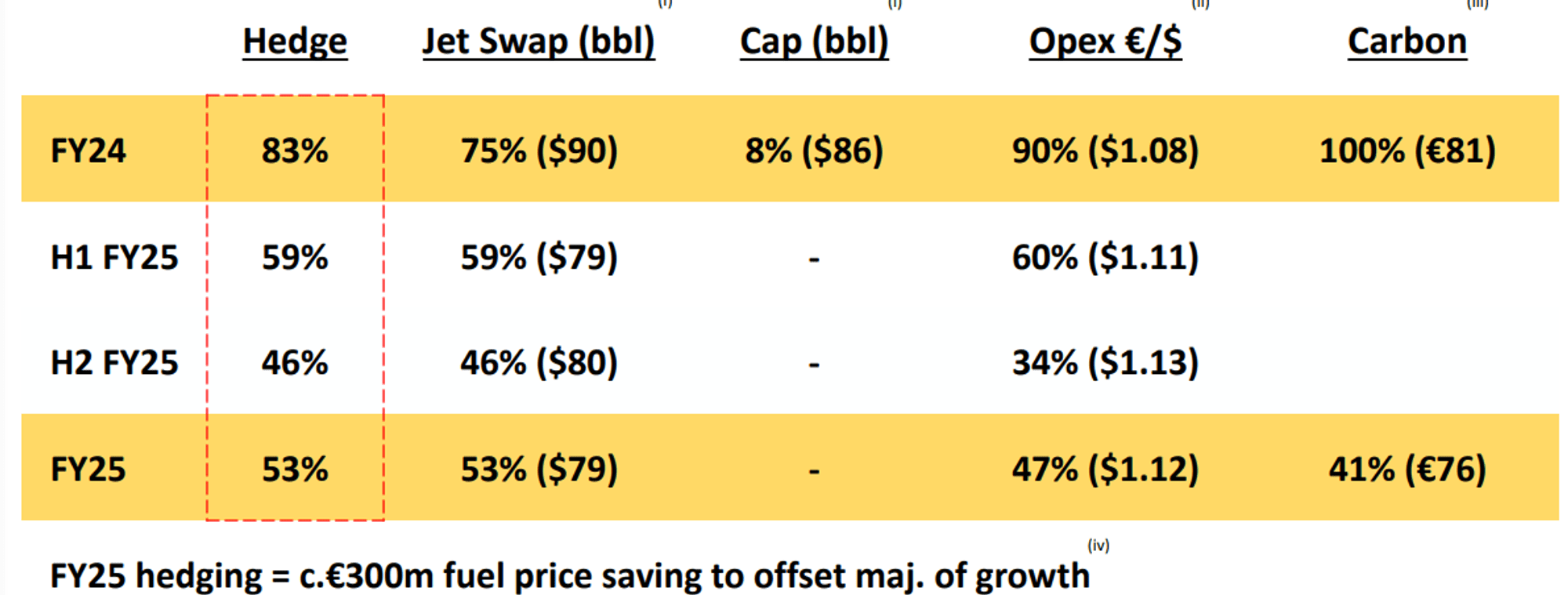

Fuel prices are a key factor to its near-term performance given the current elevated oil prices. Ryanair is currently hedged (~83%) for FY24, with reasonable visibility into FY25. This should limit margin impact while giving some scope to benefit if prices do decline.

{kind=link}

Quarterly results

Ryanair’s recent performance has been impressive, with top-line revenue growth of +57%, +57%, +40%, +23% in its last four quarters. In conjunction with this, margins have improved.

The company’s performance is a reflection of increasing travel post-pandemic, with a consistent incremental improvement. Guests in H1’24 were up +11% compared to H1’23, with a load factor of 95%. Further, Ryanair is benefiting from inflationary price increases, with European flights up an average of 16% compared to 2019 . As the guest numbers illustrate, consumers are willing to pay the increased prices, contributing to PAT growth of +59% in H1’24.

Looking ahead, we see reasonable scope to suggest a continuation of its double-digit growth is achievable, although the current macroeconomic environment is creating material uncertainty. Demand for discretionary activities is softening and with price inflation in the airline industry, consumers could be dissuaded. The benefit of Ryanair is that it is materially more price competitive, allowing it to be more flexible to retain customers.

Balance sheet & Cash Flows

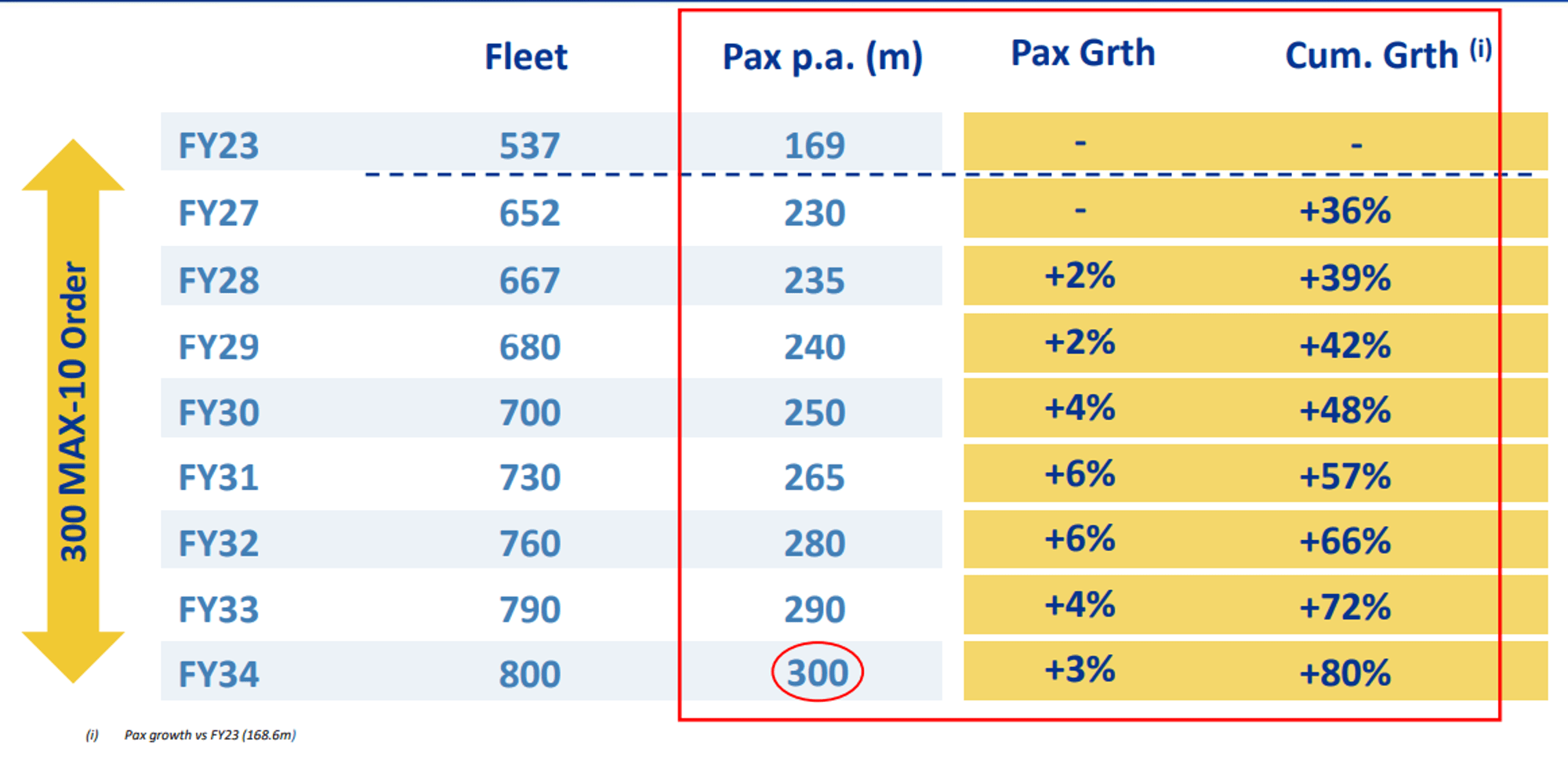

Unlike many of its peers, Ryanair is conservatively financed, with a net cash ratio of (0.3)x. This has allowed the business to limit the damage caused by the pandemic, allowing it to expand aggressively now. Capex has materially exceeded pre-pandemic levels on a € basis while boasting FY17 levels relative to revenue. As the following illustrates, capacity and pax growth is forecast to be strong in the coming years.

{kind=link}

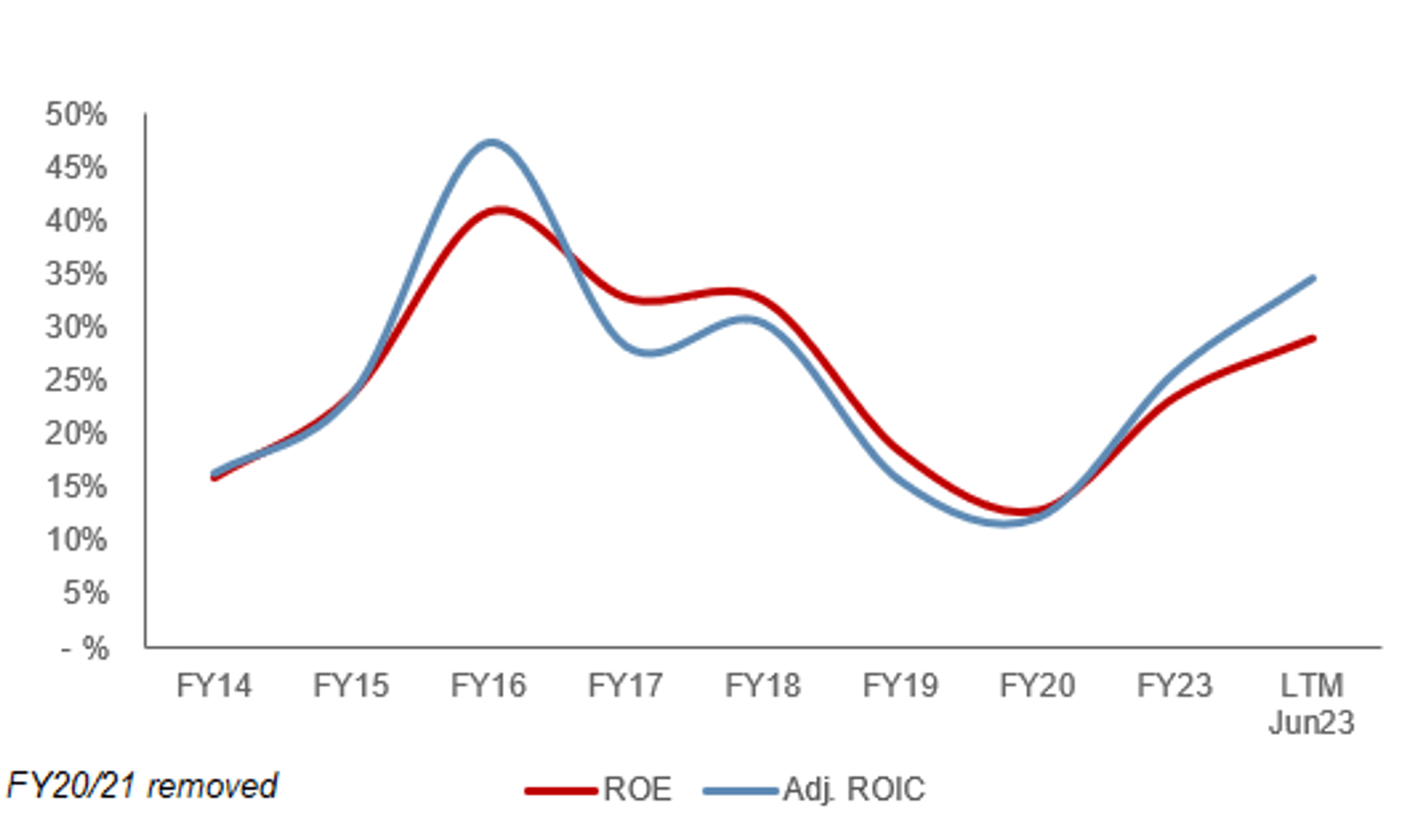

This has allowed the business to historically repurchase shares aggressively, which is something we expect to return in the not-too-distant future once revenue growth stabilizes. At a ROE of ~29% currently, investors are positioned to win with Ryanair.

{kind=link}

Outlook

{kind=link}

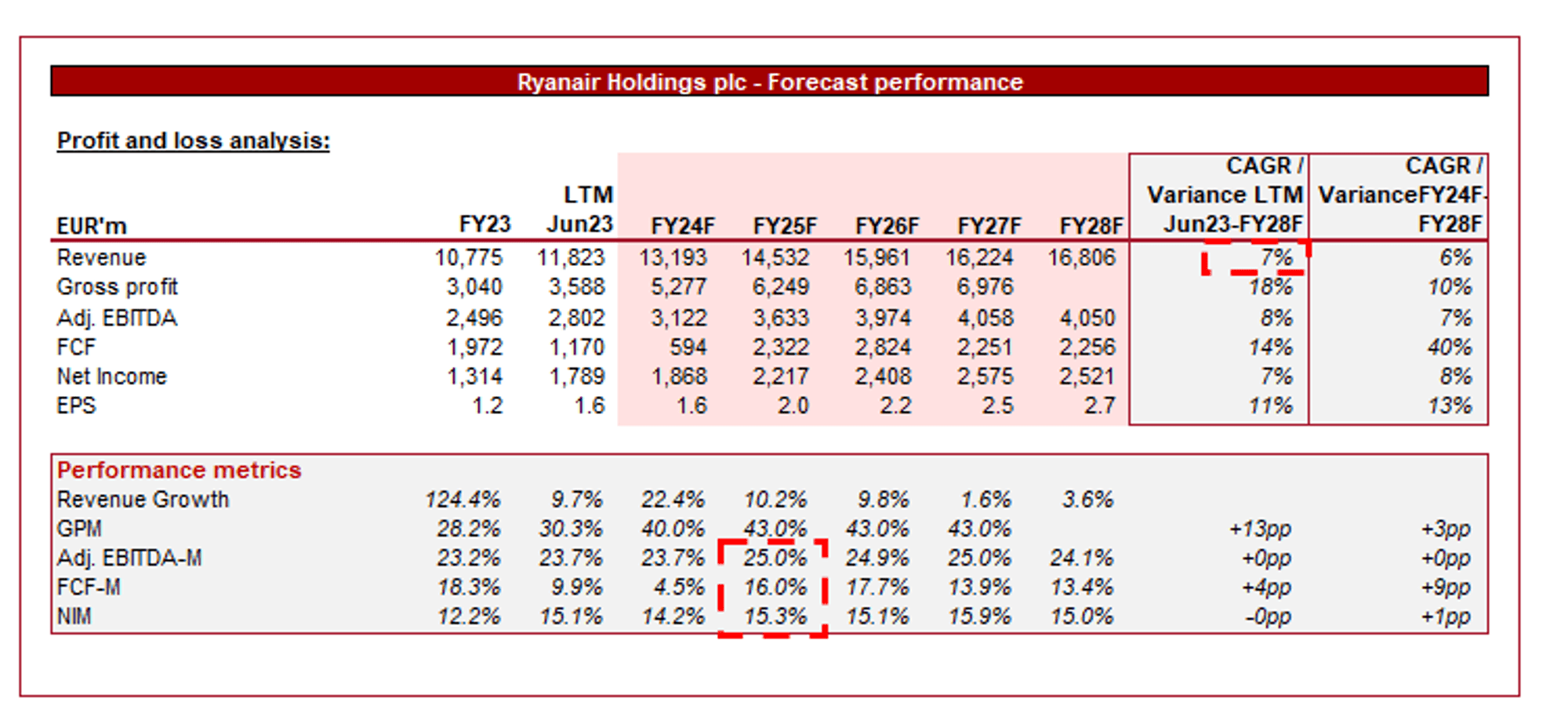

Presented above is Wall Street's consensus view on the coming years.

Analysts are forecasting a continuation of its healthy growth into FY26F, with a CAGR of +7% into FY28F. In conjunction with this, margins are expected to improve further, although remain below the FY18 levels.

We consider these assumptions to be reasonable. Macroeconomic conditions will weigh heavily, and increasingly so in FY24, but the offsetting impact of pricing and normalizing travel levels should be sufficient.

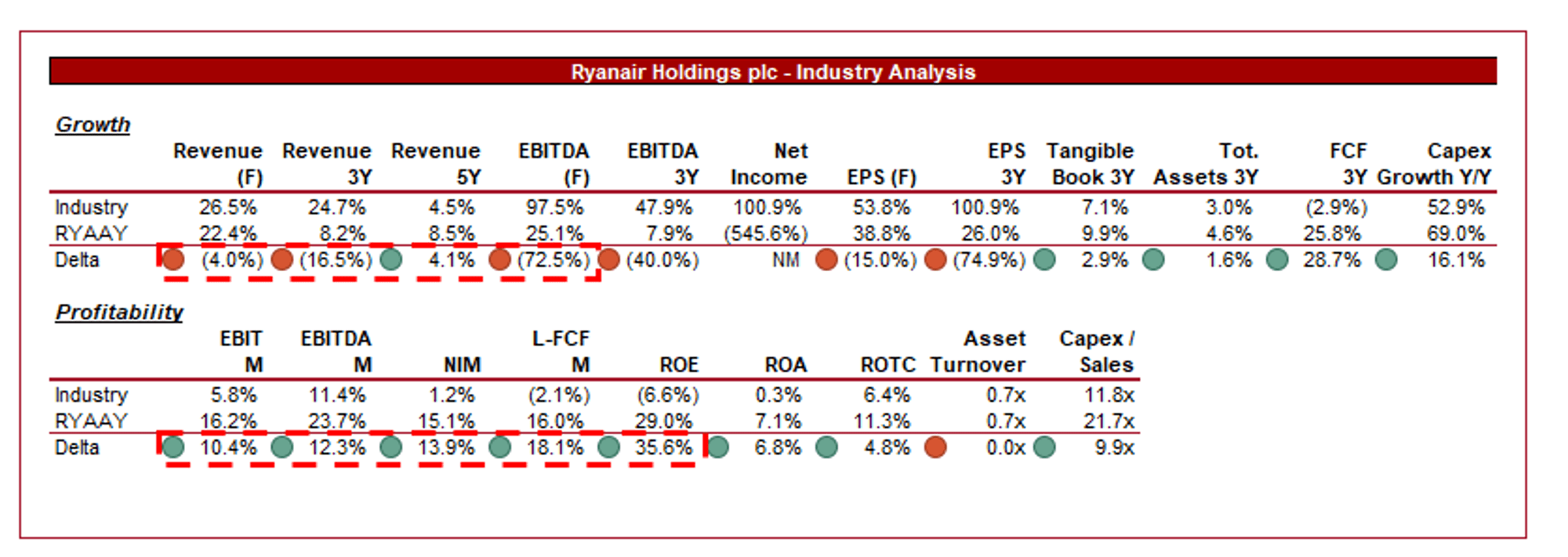

Industry analysis

{kind=link}

Presented above is a comparison of Ryanair's growth and profitability to the average of its industry, as defined by Seeking Alpha (20 companies).

Ryanair’s performance relative to its peers is impressive. The company has grown well during the last 5 years, although its peers’ metrics are distorted by revenue bouncing back later than Ryanair. From an overarching growth perspective, Ryanair is a leader.

Further, the company’s margins are significantly above its peers, which translates to FCF and ROE. This is the true value driver as growth will inevitably soften. When considered in conjunction with a bulletproof balance sheet, Ryanair’s profile is completely different (in a good way) compared to the airline industry.

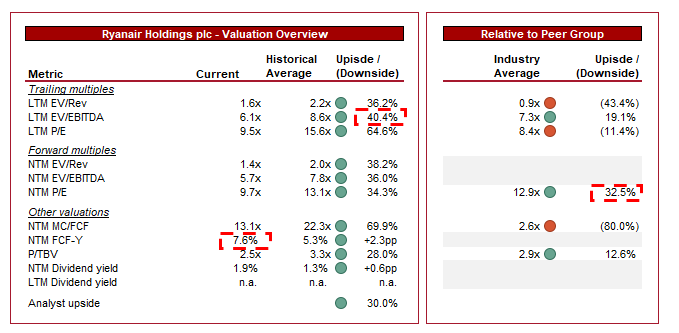

Valuation

{kind=link}

Ryanair is currently trading at 6x LTM EBITDA and 6x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is appropriate in our view, although not to a material level, primarily due to the heightened margins the business had during FY15-FY18, as well as the macroeconomic risk. This said, we would not suggest a discount beyond 10%, and even this is conservative. The company’s competitive position has improved and is on a clear upward trajectory. This suggests upside of ~30% on an EBITDA basis, although we see closer to 40% if resilience can be shown (which we expect).

Further, Ryanair is bizarrely trading at a discount to its peer groups on an LTM basis (~20%) and NTM P/E basis. This is completely unjustifiable in our view, and is likely reflective of negative sentiment in Europe relative to other geographies. This to us implies an absolute minimum upside of ~26%, which unjustifiably suggests Ryanair is in line with its peers. Realistically, this again implies upside of >30%.

Conversely, Ryanair’s valuation has trended down during the last decade, likely a reflection of investors pricing in a declining competitive position as its competitors attempt to replicate its strategy. Although we do not think this has necessarily succeeded, it is a fair criticism. Nevertheless, at a discount of >30%, investors have a sufficient margin of safety.

Key risks with our thesis

The risks to our current thesis are:

- Prolonged economic slowdown.

- Intense competition leading to fare wars.

Final thoughts

Ryanair is a high-quality business, which is rare in its industry. The company has an impressive business which we believe is still positioned to allow for market share growth, with its cost advantage widening post-pandemic.

With strong quarterly results and an outperformance relative to its peers, we believe now is a good entry point, regardless of macroeconomic concerns. Compounding this is its valuation, which is undeniably well below its fair value. Even if there is near-term pain, the long-term position of the company is impressive.

For further details see:

Ryanair: Seeing New Heights In The Post-Pandemic Era