RYAAY - Ryanair: Upside On The Horizon

2023-11-14 19:33:50 ET

Summary

- Ryanair will distribute its first ordinary dividend in its history, and we see significant scope for shareholder returns.

- Q3 higher yield, conservative guidance, and clear upside on costs vs. competitors.

- Ryanair valuation is extremely attractive and implies a material deterioration in the operating environment. Strong near-term demand supports our investment thesis.

Last week, Ryanair Holdings ( RYAAY ) released its H1 results, providing a solid set of numbers. Consequently, the company shares positively reacted to the consensus upgrades thanks to Q3 fare expectations and a new dividend policy. Ryanair has always been ' Our Bet On Travel Recovery ' thanks to the company's Gamechanger Strategy and the latest Boeing maxi order, recently approved by an extraordinary Annual General Meeting (see our publication Ryanair Is Equipped For A Decade Of Growth ).

Starting with the payout changes, Ryanair will distribute the first ordinary dividend in its history (DPS at €0.35). The Irish low-cost airline plans to remunerate shareholders in two tranches: an interim dividend payment of €200 million in February and an additional €200 million in September 2024. Therefore, Ryanair is budgeting a total outflow of €400 million after reporting an increasing profit of 59% to €2.18 billion in H1. At the current stock price, the company is yielding 2.15%.

{kind=link}

Source: Ryanair H1 Results Presentation - Fig 1

New Upside

In our forward-thinking analysis, there are four considerations that we believe will likely drive earnings recovery and upgrade on consensus estimates:

- Q3 Yield Strength . The company forecasts fare up around 15% between October and December 2023 (Q3) (Fig 2). This far exceeded Wall Street consensus. Even if visibility remains low in Q4, Q3 results might again surprise the upside (considering the Christmas pick). Here at the Lab, reverse engineering sell-side and Ryanair's estimates, we believe numbers are too conservative. In detail, the company set a net profit between €1.85 and €2.05 billion, having already recorded a net income of €2.18 billion in H1. This would imply a €300 million Q4 net loss, assuming break-even estimates in Q3. Looking back, the company reported a net loss of €313 and €211 million in Q4 2021 and Q4 2022, respectively. However, these were periods affected by COVID-19 pandemic outbreaks with depressed load factors and fares. Therefore, in our view, we might have further upgrades in early 2024;

- Lower Fuel estimates . Q1 2024 is forecasted to see a fuel headwind of approximately €1.3 billion year-over-year. This is due to the recent oil price environment. Despite that, looking ahead, we see net profit taking another increase thanks to the easing of cost headwinds. In detail, the company almost hedged 53% of fuel at a price below $79 per barrel in 2025 (Fig 3), which is well below the current spot. In addition, the company hedged 75% of fuel for the upcoming 2024. Although there was no guidance, we might forecast an expected savings of approximately €500 million with hedging protection and inflation easing. The company predicts a €300 million fuel price saving. Still, we are above the internal guidance due to a $65 long-term price per barrel (estimated in 2025) and the ongoing intake of new plane deliveries. With the new 26 B737 already arrived in H1, the Gamechangers is moving on thanks to " 4% more seats and 16% fewer fuel consumption" ;

- Upside vs. Competitors . Key to note is the Ryanair release on the Pratt & Whitney development. In the press release, the company reported an " inspection program to substantially curtail competitor and lessor capacity between 2024 and 2026 ." This evolution, combined with " the large backlog of OEM aircraft deliveries is also likely to constrain capacity in Europe for the next 3 or 4 years, " will likely create traffic and profit growth opportunities for the Irish operator. In number, the company expects an uplift of 300 million per year by 2034;

-

Upside in shareholders remuneration . We have already commented on dividends; however, there is significant scope for shareholder returns beyond the common dividend. We estimate a 2.15% and 3.2% yield for 2024 and 2025, respectively. Despite that, for the upcoming years, management plans to return approximately 25% of prior-year profit after tax to shareholders. In our number, we model €1.8 billion in shareholders remuneration until 2026. This implies a potential return of almost 10% based on the current market capitalization and is calculated on net profit estimates of €1.82/$2.5/$2.9 billion in 2024/2025/2026.

{kind=link}

Fig 2

{kind=link}

Fig 3

Change to Estimates

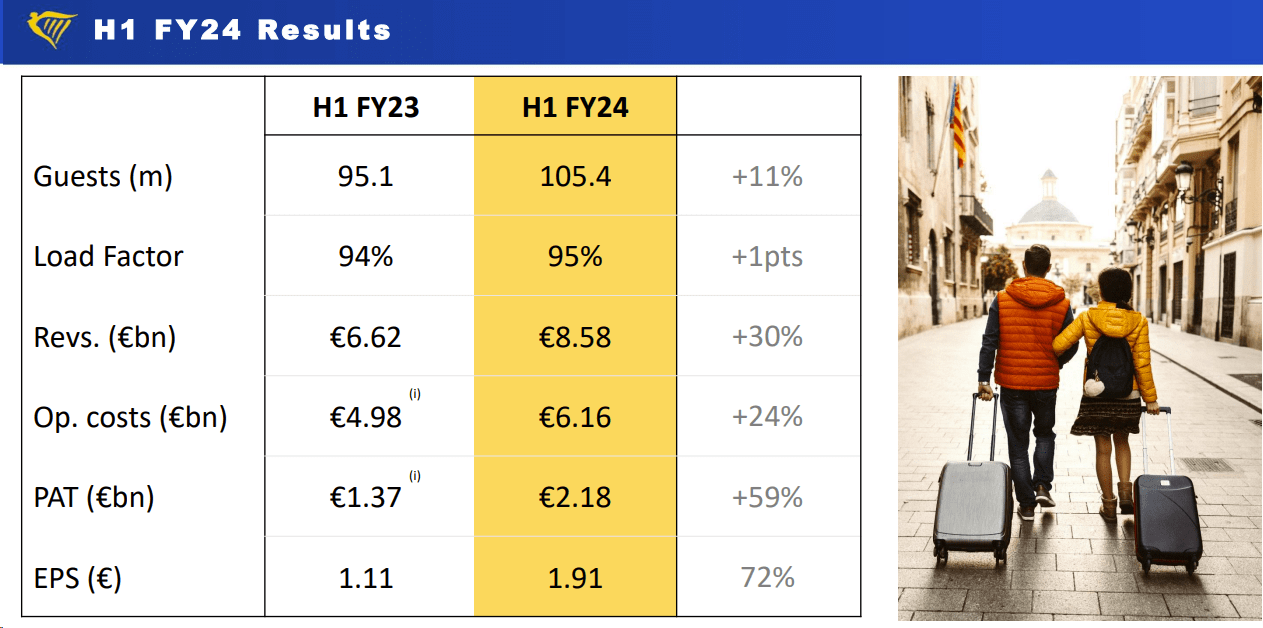

H1 results were impressive, with top-line sales of €8.58 billion, up 30% annually, and 105 million passengers transported in the period, signing a plus 11%. Total OpEx increased by 24% to €6.2 billion due to higher staff costs and fuel. Despite that, the company's cost advantage continues to widen. Here at the Lab, we are modeling 183.9 and 205 million passengers to be transported in 2024 and 2025 with a load factor of 94% and 94.4%. This leads our total sales at €13.2 and €14.52 billion per year, with an EBIT of almost €2 billion in 2024 and €2.5 billion in 2025. Our core operating profit per passenger is forecasted at €10.69 and €12.35 in 2024 and 2025, respectively. Our Fiscal Year estimates net profit increase by 10% and 8% for the following period, leading to an increase in our target price from €19 to €21 per share.

Ryanair H1 Financials in a Snap

{kind=link}

Fig 4

Conclusion and Valuation

A solid set of results, a new dividend policy, and a supportive Q3 yield. A potential net income increase on alleviated fuel costs makes Ryanair's valuation extremely attractive on both short-medium-term horizons. Thanks to the company's cost advantage over peers and potential market share gains in the future, we decided to increase our target price to €21 per share. This is based on a 2025 EPS of €2.05 and a P/E of 10x. Ryanair traded at a median P/E of 14x in the period between 2004 and 2019. Our target price has an upside of 25% on the current stock price, and combined with Ryanair's dividend policy, we arrive at a potential shareholder return of 34.5% (including the dividend). In our estimates, in Fiscal Year 2024, the company has a net cash position that offers downside protection. Downside risks include B737 order delay, Brexit higher restrictions, higher fuel prices, and a stronger US dollar.

For further details see:

Ryanair: Upside On The Horizon