RYI - Ryerson Holding: Challenging Near-Term Outlook Still Headwind For Shares

2023-12-12 03:04:58 ET

Summary

- Ryerson Holding Corporation receives a "Hold" recommendation due to potential headwinds from lower prices and sales volumes.

- The company has expanded its product offering and sees opportunities in government spending on infrastructure and green technologies.

- The company's financial position is stable, but near-term challenges in the metal fabrication industry may still impact profitability and stock price.

A "Hold" Recommendation Rating Assigned to Ryerson Holding Corporation

This analysis gives a "Hold" recommendation on shares of Chicago, Illinois-based metal products processor and distributor Ryerson Holding Corporation (RYI), as profitability, considered the key driver of the stock's price, is likely to face additional headwinds from lower prices and sales volumes.

Recently, the company has expanded its future product offering with the acquisition of Hudson Tool Steel, a supplier of tool steels and high-speed, carbon, and alloy steels in the United States, leaving the company much better positioned when the cycle rolls strong again.

With this transaction, the company sees many more opportunities to capitalize on the robust outlook for its metal products. This is driven by significant government spending on public infrastructure, energy transition projects and incentives for the adoption of greener technologies, including electric vehicles and those that enable the exploitation of renewable energy sources.

Moreover, the overall financial position seems stable enough to withstand further challenges and not cause major concerns among shareholders.

Furthermore, as headwinds from the threat of a worsening economic cycle persist, there may be an opportunity to gain greater exposure to the sector's long-term growth prospects at a lower share price. Its stock also pays a dividend, which doesn't appear to be at risk should the economy enter a recession.

Therefore, it is believed that a Hold rating is currently the most appropriate rating for Ryerson Holding Corporation stock.

Ryerson Holding Corporation in the First 9 Months of 2023 and Near-Term Challenges to Growth Expectations

The immediate future of the metal fabrication industry remains bleak for its operators, and Ryerson Holding Corporation is not spared.

The sector has not been spared from the recent deterioration in business conditions. Due to the well-known problems of high core inflation and tighter credit conditions affecting consumers’ purchasing power, lower orders are currently affecting the entire US manufacturing sector and also posing challenges for Ryerson Holding Corporation and other operators.

Anticipating weaker demand for metal products in the near term, Ryerson Holding and other manufacturers are running down inventories and may focus on additional labor reduction initiatives. Labor accounts for approximately 70-80% of total operating costs.

Manufacturing companies bottomed out in November 2023, recording three consecutive months of declining activity. Operators also currently have to contend with an unfavorable selling price environment.

The consequences of this negative trend were felt in Ryerson's quarterly results, which posted a 7.2% sequential decline and a 19.2% year-over-year decline to $1.2 billion in the third quarter of 2023 , reflecting lower sales volumes and selling prices as most manufacturers did. Due to the same issue, total revenue for the first nine months of 2023, which amounted to $3.996 billion, was down 20.6% year-on-year.

The company sells carbon steel, aluminum, and stainless-steel products to various industries. The total amount of metal products shipped in the third quarter of 2023 was 478,000 tons, down 3.6% quarter-on-quarter and 6.6% year-on-year. In the first 9 months of 2023, the company shipped 1.493 million tons, down 4.5% year-on-year.

In the third quarter of 2023, metal products were sold at an average price of $2,608 per ton, down 3.7% quarter-over-quarter and 13.5% year-over-year. The average selling price was $2,677 per tonne of metal in the first nine months of 2023, down 16.9% year-on-year.

Margins are also currently affected as follows:

Excluding the effects of LIFO, the gross margin increased 110 basis points year-over-year to 17.3% in the third quarter of 2023 but decreased 140 basis points quarter-over-quarter. In the first nine months of 2023, the gross margin fell significantly by 250 basis points to 18.4%.

Excluding the effects of LIFO, the Adjusted EBITDA margin declined 150 basis points year-over-year, and it declined 160 basis points quarter-over-quarter to 3.6% in the third quarter of 2023, and in the first nine months of 2023 the Adjusted EBITDA margin declined significantly by 590 basis points to 5.1%.

Undoubtedly, the continued cooling of inflation could provide some relief. If anything, the risk of demand shifting to competitors is reduced if the company tries to pass on higher costs to customers to a lesser extent than before.

However, business expectations continue to point to subdued growth prospects for demand in the coming months and therefore prices are unlikely to improve from the first nine months of 2023.

Due to an economic recession, as suggested by the inverted US Treasury yield curve (currently: 10-year return of 4.2441% versus 1-year return of 5.155%), and predicted by economists , whose views recently welcomed the Swiss bank giant UBS Group AG (UBS), demand will continue to be characterized by weak conditions for the foreseeable future.

Demand from international customers will also be no better than domestic demand due to the economic problems in the EU and China, the USA's most important trading partners. The EU economy is facing similar problems to the US: the European Central Bank had to raise interest rates to counteract rising inflation, but now these two factors are affecting consumption and investment.

In China, the economic cycle, already in trouble after three years of strict lockdowns and restrictions to contain the spread of the COVID-19 virus among the population, is now facing deflation problems . Chinese consumers are putting off purchases of several categories of goods and services and companies are doing the same with investments because they believe they can benefit from lower prices if they just wait, putting further pressure on demand. In addition, the real estate industry – a pillar of the Chinese economy – continues to suffer from the inability of real estate developers such as China Evergrande Group ( OTC:EGRNQ ) and Country Garden Holdings Company Limited ( OTCPK:CTRYF ) ( OTCPK:CTRYY ) to meet their financial obligations offshore.

Due to the expected downward pressure that the described demand challenges will place on prices, a significant recovery in the company's profit margins is unlikely for the time being, limiting the chances of an uptrend in the stock price from current levels.

Looking ahead to the fourth quarter of 2023, Ryerson expects a 4% to 7% sequential decline in shipments with net sales of $1 billion to $1.15 billion versus $1.29 billion last year . The company also expects average selling prices to decline 3% to 5% sequentially. Excluding LIFO, the adjusted EBITDA is expected to range between $28 million and $32 million, compared to $28.7 million in the fourth quarter of 2022 . Excluding LIFO, the adjusted EBITDA margin is therefore expected to be approximately 2.8% in the fourth quarter of 2023, versus 2.2% in the fourth quarter of 2022 .

The Financial Condition

A strong financial position will help the company to continue to weather the headwinds described.

In the third quarter of 2023 , Ryerson Holding Corporation generated an operating cash flow of $79.3 million, down 47.7% year-over-year and down 31.2% quarter-over-quarter. Operating cash flow was $275 million for the first 9 months of 2023 compared to $319.6 million for the same period in 2022. Although free cash flow declined, it was still positive at $56.9 million in the third quarter of 2023, compared to $69.1 million in the previous quarter and $124 million in the year-ago quarter.

For the first 9 months of 2023, free cash flow fell 30.3% year-over-year to $178.6 million. However, the company continued to finance growth with the acquisition of a company mentioned earlier in this article, the payment of the dividend, and the share repurchase program, which signal a strong financial condition.

As of the third quarter of 2023, Ryerson's balance sheet totaled $37.4 million in cash and short-term investments, little changed from $39.2 million at the end of 2022. The company had a potential of $699 million invested in the inventory.

Total debt was $365.9 million as of September 30, 2020, up from $367 million as of December 30, 2022. The financial burden creates obligations that the company appears to be able to cover with the income it can generate from business operations.

In fact, the solvency ratio of interest coverage ratio, which is calculated as operating income divided by interest expense, indicates that on a 12-month basis, the former exceeds the latter by 4.6 times as of Q3-2023 .

If you scroll down to the risk section on this page of Seeking Alpha, you'll find the Altman Z-Score of 3.68, indicating that Ryerson's balance sheet is in safe territory and the risk of bankruptcy within a few years is virtually zero.

Therefore, the continuation of dividend payments is not at risk, nor is the financing of other activities that support the share price.

In the third quarter of 2023, the company committed $4 million to repurchase 133,094 shares under an open market share repurchase program through April 2025, for an aggregate amount of up to $100 million with 45.7% remaining to be repurchased.

Ryerson Holding Corporation will also pay a quarterly dividend of $0.185 per common share, with the next payment on December 14, 2023, representing 1.1% growth from the last payment in September and 15.625% growth from December 2022. In the third quarter of 2023, Ryerson Holding Corporation paid quarterly dividends of $6.3 million.

The payment results in a forward dividend yield of 2.41% as of this writing, while the S&P 500 yields 1.50%.

The Stock Valuation

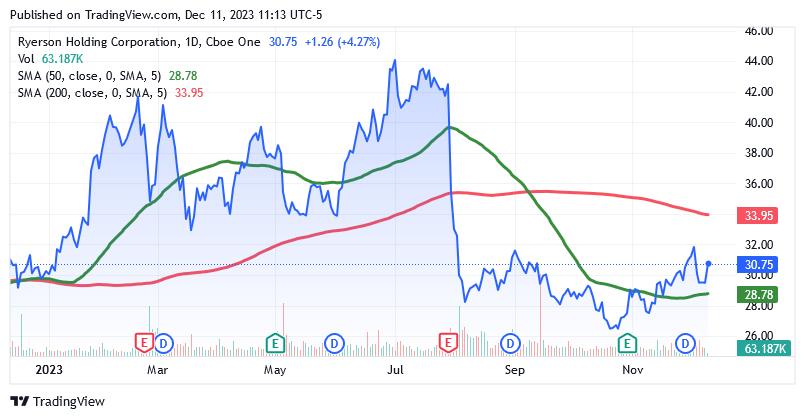

Shares of Ryerson Holding Corporation were trading at $30.75 per unit giving it a market cap of $1.01 billion.

{kind=link}

Shares don't look expensive as they trade well below the 200-day simple moving average of $33.95 but just slightly above the 50-day SMA of $28.78. Furthermore, shares are also below the midpoint of $35.425 in the 52-week range of $26.15 to $44.70.

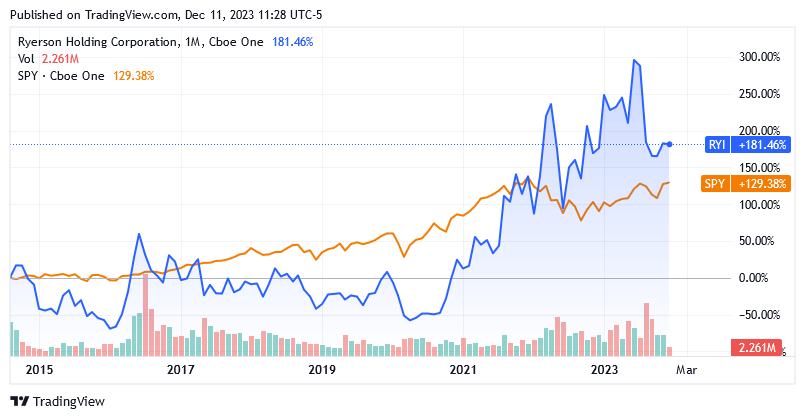

Within the growing metal processing industry, shares of Ryerson Holding Corporation proved to be an effective candidate to beat the US stock market. As a benchmark for the U.S. stock market, the SPDR® S&P 500 ETF Trust ( SPY ) grew 129.38% over the past several years, while shares of Ryerson Holding Corporation rose 181.48%.

{kind=link}

Thanks to a solid financial condition and resilient business, this stock is well positioned for the recovery of operating conditions in the industry driven by several programs to grow the economy in a sustainable manner, such as electrification and green projects. The stock price is currently low compared to its recent past, but this analysis suggests not buying shares of this stock now to increase exposure to the long-term growth prospects of the metal fabrication industry.

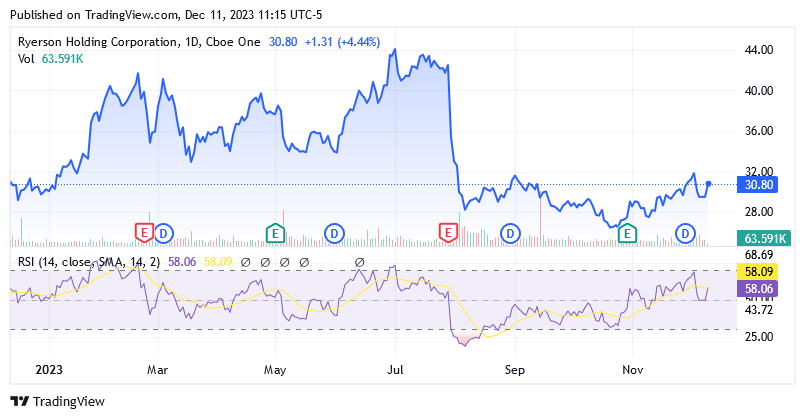

Shares will face greater headwinds given the looming recession, which will probably further weigh on the company's profitability. The 14-day relative strength indicator at 58.06 suggests a large margin to the downside if shares start to decline from current levels.

{kind=link}

This analysis suggests holding the shares for now, with the possibility of strengthening the position in the near future as the market is likely to propose more favorable entry points if the recession sets in.

Conclusion

Ryerson Holding Corporation is well positioned to benefit from the growth prospects for the metal fabrication industry that remain strong over the long term. As the current challenging period is over, the stock will benefit from a solid balance sheet and resilient operations. Lower demand and lower selling prices may continue to weigh on the company's profitability and affect the share price. This analysis does not suggest increasing exposure to the industry through this stock now, but rather wait, as lower share prices are certainly possible at this point.

For further details see:

Ryerson Holding: Challenging Near-Term Outlook, Still Headwind For Shares