VNQ - Ryman Hospitality: Expanding On The Grand Ole Opry

2023-07-26 10:15:00 ET

Summary

- Hotel REITs are making a steady comeback, up a modest 4.93% in 2023, despite taking a significant hit during the pandemic.

- Domestic travel has recovered to 100% of pre-pandemic levels, all COVID restrictions have been lifted from international travel, and gasoline prices are down sharply, providing strong tailwinds for hotel demand.

- Ryman Hospitality Properties is achieving high double-digit revenue growth in both its hotel segment and its entertainment segment, driving its Debt/EBITDA down to an excellent 4.2.

- Growth like this usually comes at a premium price, but Ryman's FFO multiple remains far below the REIT average.

- This article examines growth, balance sheet, dividend, and valuation metrics for this group-oriented luxury resort Hotel REIT.

It is no secret that Hotel REITs took a ferocious beating during the pandemic. What is less widely known is that Hotel REITs are making a steady comeback. As of this writing, Hotel REITs are up 4.93% in 2023, good for a middle-of-the-pack 9th-place standing among REIT sectors, and just slightly off the 5.35% pace set by the average REIT. Meanwhile, REITs as a whole are lagging the NASDAQ and the S&P indexes.

Hoya Capital Income Builder

Airline travel, which is highly correlated to hotel demand, has fully returned to pre-pandemic levels.

Hoya Capital

According to the U.S. Energy Information Administration, gasoline prices are down more than 20% from a year ago, providing another summer travel tailwind.

{kind=link}

Hoya Capital's latest sector report on Hotel REITs reads, in part:

Hotel REITs are pacing for a second-straight year of outperformance after punishing early-pandemic declines, buoyed by steady post-pandemic operating improvement and the long-awaited return of dividends.

According to the International Air Transport Association ("IATA")

International traffic climbed 68.9% versus March 2022 with all markets recording healthy growth, led once again by carriers in the Asia-Pacific region. International RPKs reached 81.6% of March 2019 levels while the load factor at 81.3% exceeded the March 2019 level by 10.1 percentage points.

The final pandemic-era travel restrictions were lifted in May, so further recovery is expected over the coming months.

Meanwhile, hotel operating performance is sturdy. RevPAR (Revenue Per Available Room), occupancy, and ADR (Average Daily Rate) all remain at or above 2019 levels, after reaching all-time highs in 2022.

Hoya Capital Income Builder

CBRE ( CBRE ) forecasts RevPAR growth of 5.8% in 2023 driven by a 4.2% increase in ADR and a roughly 100 basis point improvement in occupancy.

The forecast is best for Economy, Mid-Scale, and Upper-scale hotels, and markets in the southern half of the country.

CBRE Hotels Research

This article examines growth, balance sheet, dividend, and valuation metrics for Tennessee-based group-oriented luxury resort hotel REIT Ryman Hospitality Properties.

Meet the company

Ryman Hospitality Properties

Founded originally in 1925 and headquartered in Nashville, Ryman Hospitality Properties ( RHP ) went public as Gaylord Entertainment in 1991, and reorganized as a REIT in 2012. The company owns and operates:

- the Grand Ole Opry,

- Ryman Auditorium, and

- WSM radio station in Nashville, along with

- Block 21 in Austin, and

- Ole Red, a live music venue and restaurant/bar chain with 5 locations (2 in Nashville).

The company also owns:

- 6 Gaylord hotels,

- the AC Hotel (Washington, DC),

- Gaylord Springs Golf Links (Nashville),

- The General Jackson Showboat (Nashville), and

- The Wildhorse Saloon (Nashville)

all of which are operated by Marriott International.

The majority (69%) of room bookings for Ryman are groups, broken down as follows:

Company investor presentation

Such groups tend to book far in advance, making RHP revenues more stable and predictable than the average hotel.

Company investor presentation

Unlike hotels in Las Vegas, Ryman's portfolio tends to provide all the entertainment under one roof. As a result, customers spend about $1.50 outside the room for every $1.00 of room revenue. This results in the highest RevPAR in the Hotel REIT sector.

Company investor presentation

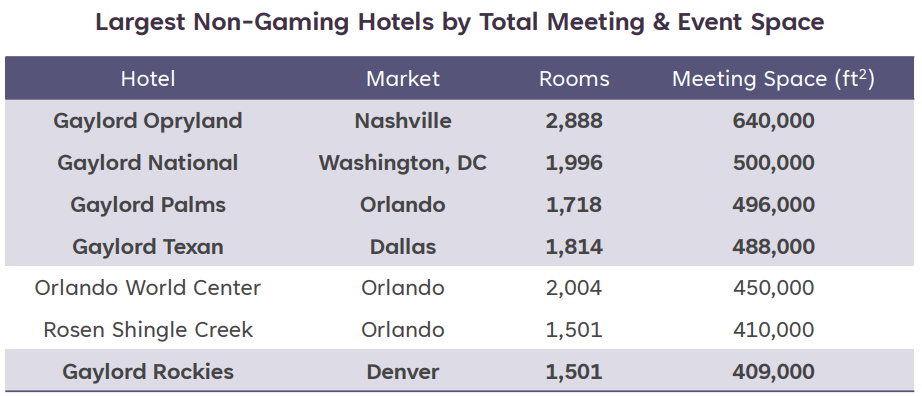

These tend to be very large hotels, and the supply of new, competing hotels this size is very constrained.

{kind=link}

Ryman posted the strongest occupancy rate of all Hotel REITs in Q1, at 72.3%. ADR is up 18.3% from pre-pandemic levels, and RevPAR is up 13.5%.

Hoya Capital Income Builder

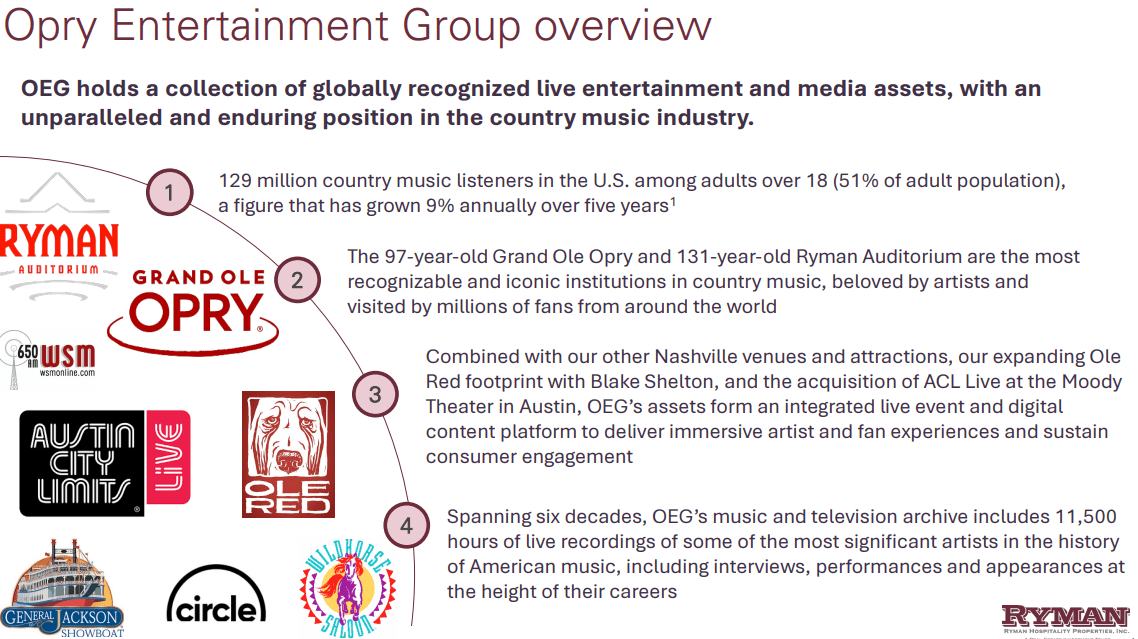

Apart from their hotels, RHP also owns a 70% interest in some of the most iconic, high-quality live music venues in the country, particularly with the acquisition last year of Block 21 in Austin, where Austin City Limits originates.

{kind=link}

RHP's entertainment segment revenue, which naturally took a heavy blow in 2020, has skyrocketed since, and stood at 46.4% above pre-pandemic levels at the end of last year.

Company investor presentation

The company expects their entertainment segment to grow by about 18% this year, and account for about 17% of the company's operating income. They expect hotel revenues to leap even faster, at 22.7%.

Company investor presentation

Growth metrics

Here are the 3-year growth figures for FFO (funds from operations), and TCFO (total cash from operations). Despite the pandemic, RHP has managed to grow FFO per share by 7.0% per annum and cash from operations at 5.8%.

| Metric |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| 3-year CAGR |

| FFO (millions) |

| $325 |

| (-$237) |

| $31 |

| $335 |

| -- |

| FFO Growth % |

| -- |

| NA |

| NA |

| 908.1 |

| 1.0% |

| FFO per share |

| $6.25 |

| (-$4.29) |

| $6.01 |

| $7.65 |

| -- |

| FFO per share growth % |

| -- |

| NA |

| NA |

| 27.3 |

| 7.0% |

| TCFO (millions) |

| $355 |

| (-$162) |

| $111 |

| $420 |

| -- |

| TCFO Growth % |

| -- |

| NA |

| NA |

| 278.4 |

| 5.8% |

Source: TD Ameritrade, Hoya Capital Income Builder, and author calculations

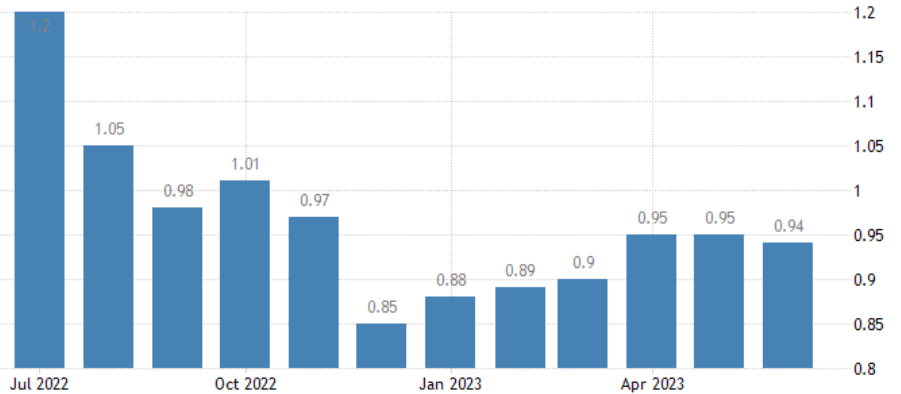

Meanwhile, here is how the stock price has done over the past 3 twelve-month periods, compared to the REIT average as represented by the Vanguard Real Estate ETF ( VNQ ).

| Metric |

| 2020 |

| 2021 |

| 2022 |

| 2023 |

| 3-yr CAGR |

| RHP share price July 24 |

| $31.33 |

| $79.41 |

| $81.82 |

| $92.41 |

| -- |

| RHP share price Gain % |

| -- |

| 153.5 |

| 3.0 |

| 12.9 |

| 43.4% |

| VNQ share price July 24 |

| $77.92 |

| $105.82 |

| $94.02 |

| $86.89 |

| -- |

| VNQ share price Gain % |

| -- |

| 35.8 |

| (-11.2) |

| (-7.6) |

| 3.70% |

Source: MarketWatch.com and author calculations

RHP shares have outperformed the VNQ in each of the past three 12-month periods. If you had bet on Ryman in the dark days of the pandemic, you would be sitting on 43.4% average annual returns since then, whereas the VNQ has averaged a gain of just 3.7%. Kudos to Seeking Alpha Contributor Thomas Lott for seeing and calling this in June of 2020.

Meanwhile, RHP sits squarely in the market cap sweet spot , at $5.5 billion.

Balance sheet metrics

Here are the key balance sheet metrics. Despite having liabilities that almost equal assets, RHP has an investment-grade balance sheet. While its debt ratio is typical of the recovering Hotel REIT sector, RHP sports an exceptional Debt/EBITDA ratio of 4.2, which suggest the company can maintain its dividend easily, and grow out of some of its indebtedness.

| Company |

| Liquidity Ratio |

| Debt Ratio |

| Debt/EBITDA |

| Bond Rating |

| RHP |

| 1.03 |

| 40% |

| 4.2 |

| B |

Source: Hoya Capital Income Builder, TD Ameritrade, and author calculations

This company was holding $319 million in cash and equivalents through Q1, over against $2.87 billion in debt. With $755 million available in their revolver, total liquidity is a little over $1 billion.

RHP faces a formidable $800 million in debt maturities this year, although it is all extendable until 2026. The company will probably take that option, as maturities for the three years from 2024 through 2026 total only $506 million.

company investor presentation

Dividend metrics

RHP pays a 4.33% yield currently, which is well above the REIT average of 3.72%. Ryman suspended its dividend payout after Q1 2020, and did not resume paying dividends until Q3 2022. However, as of Q1 2023, Ryman has completely restored its dividend, and even raised it a little, compared to 2020.

| Company |

| Div. Yield |

| 3-yr Div. Growth |

| Div. Score |

| Payout |

| Div. Safety |

| RHP |

| 4.33% |

| 152.0% |

| -- |

| 50% |

| -- |

Source: Hoya Capital Income Builder, TD Ameritrade, Seeking Alpha Premium

Dividend Score projects the Yield three years from now, on shares bought today, assuming the Dividend Growth rate remains unchanged. Due to the slashing of dividends during the pandemic, the 3-year dividend growth figures are distorted at levels that cannot possible be sustained going forward. Dividend scores for Ryman and for the Hotel REIT sector are therefore not shown above, because they would be misleading.

Suffice it to say that barring another major catastrophe, RHP is a strong dividend payer, and its expected revenue growth bodes well for a continuation of strong cash payouts to investors.

Valuation metrics

Growth like this usually comes at a premium price, but Ryman's FFO multiple of 11.2 remains far below the REIT average of 17.2. Thus, there is something here for both growth investors and value investors.

| Company |

| Div. Score |

| Price/FFO '23 |

| Premium to NAV |

| RHP |

| -- |

| 11.2 |

| (-12.0)% |

Source: Hoya Capital Income Builder, TD Ameritrade, and author calculations

Growth investors expect to pay a premium valuation for quality, and indeed, RHP's FFO multiple is the highest of all the hotel REITs. Yet, from a value investor's perspective, the stock sells for a "bargain" valuation, 600 basis points below the REIT average, while paying an above-average dividend.

What could go wrong?

Hotel REITs are the single most economically-sensitive REIT sector. A recession, or even the lingering broad-based expectation of a recession, could adversely affect share prices for Hotel REITs.

Because so much of Ryman's portfolio is concentrated in Nashville, changes affecting the local economy could have an outsized impact on profitability.

Investor's bottom line

Skyrocketing revenue growth in both of the company's segments, exceptionally low Debt/EBITDA, and above-average yield, all at a price that is well below the REIT average, make RHP an attractive proposition for both growth and value investors. I rate this company a solid Buy, despite its somewhat marginal balance sheet.

Seeking Alpha Premium

The Seeking Alpha Quant ratings system loves everything about RHP except its valuation, and rates it a Hold.

The Street and Ford Equity Research both rate the company a Buy, and Zacks gives it a Strong Buy. Five of the seven Wall Street analysts covering the firm rate it a Strong Buy, versus one Buy and one Sell. The average price target is $110.29, implying 19.3% upside.

As always, however, the opinion that matters most is yours.

For further details see:

Ryman Hospitality: Expanding On The Grand Ole Opry