AFMC - S&P 500: Federal Reserve Signals Bumpy Ride Ahead

2023-03-08 10:40:37 ET

Summary

- As Federal Reserve Chairman Jerome Powell visits Capitol Hill this week, he reinforces his determination to get inflation back to 2%.

- Fed Fund futures are already factoring in a 50bp move at the next FOMC meeting, with a terminal rate as high as 5.75%.

- The S&P 500 seems rather expensively priced, comparing earnings yields to Treasury yields in anticipation of a recession.

- After the meeting, the yield curve, specifically the spread between 2-year and 10-year treasuries, inverted to a multi-decade low and shot past the -100 bp mark.

- Much of the next Fed decision hinges on economic data which is being released this Friday and next week.

Investment Thesis

Federal Reserve Chairman Jerome Powell is visiting Capitol Hill this week for his semiannual monetary policy report to Congress. In his prepared remarks, he hammered home the usual message: They're determined to bring inflation back to their 2% target.

However, what this means for equity markets and the economy, he also hinted, is that there's a bumpy ride ahead. We look at the key indicators the Federal Reserve Chairman mentioned, and give our views on what this means for equity markets going forward, particularly the S&P 500 ( SPY ), and why we think equity markets are priced rather expensively in the current environment.

And, of course, we also discuss the data that will be released in the coming weeks that will determine the Fed's policy decisions because, as usual, they are "data dependent." One thing is certain: There's more work to be done.

Over the past year, we have taken forceful actions to tighten the stance of monetary policy. We have covered a lot of ground, and the full effects of our tightening so far are yet to be felt. Even so, we have more work to do . (Jerome Powell, Testimony )

First, Jerome Powell began his remarks in a rather bearish tone, pointing to some of the recent January data that came in hotter than expected. In doing so, he pointed to the trend reversal in the previously softening data.

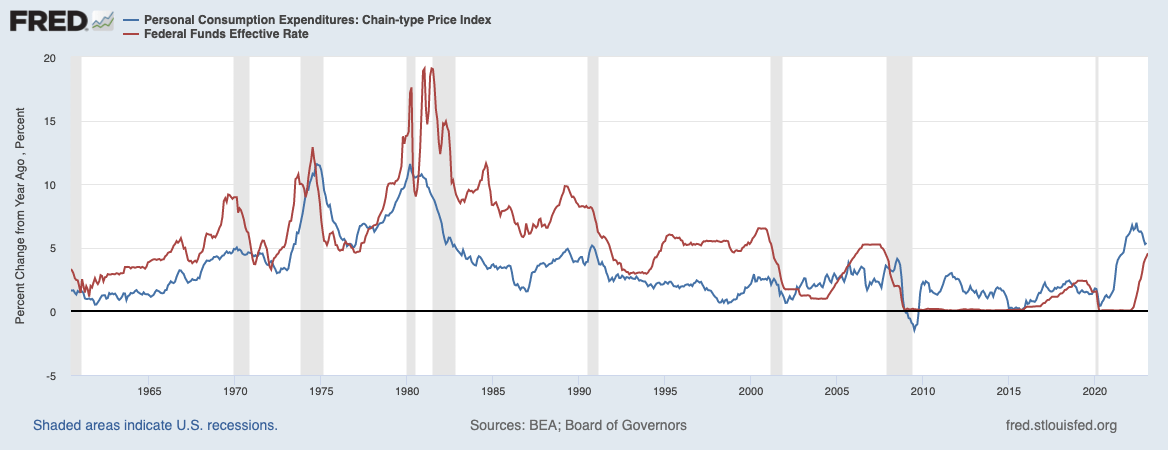

More specifically, he cited employment, consumer spending, manufacturing production and inflation as the higher-than-expected data. One of the Fed's favorite gauges, personal consumption expenditures (PCE), has seen a slowdown over the past 12 months, citing falling energy prices and the resolution of supply chain bottlenecks. Nevertheless, the measure still remains around 5.4%, which is considered well above target.

In the chart below, we have shown this measure along with the current Fed Funds rate, to show that in the past the Fed has raised the Fed Funds rate significantly above the desired PCE metric, to get a grip on inflation.

{kind=link}

Higher For Longer

Like many other economists, we believe that the Federal Reserve is most likely aiming to get the Fed Funds back well above PCE this time around, which also indicates that there's more work to be done, with the Fed possibly raising interest rates above 5.5% if this PCE index remains sticky.

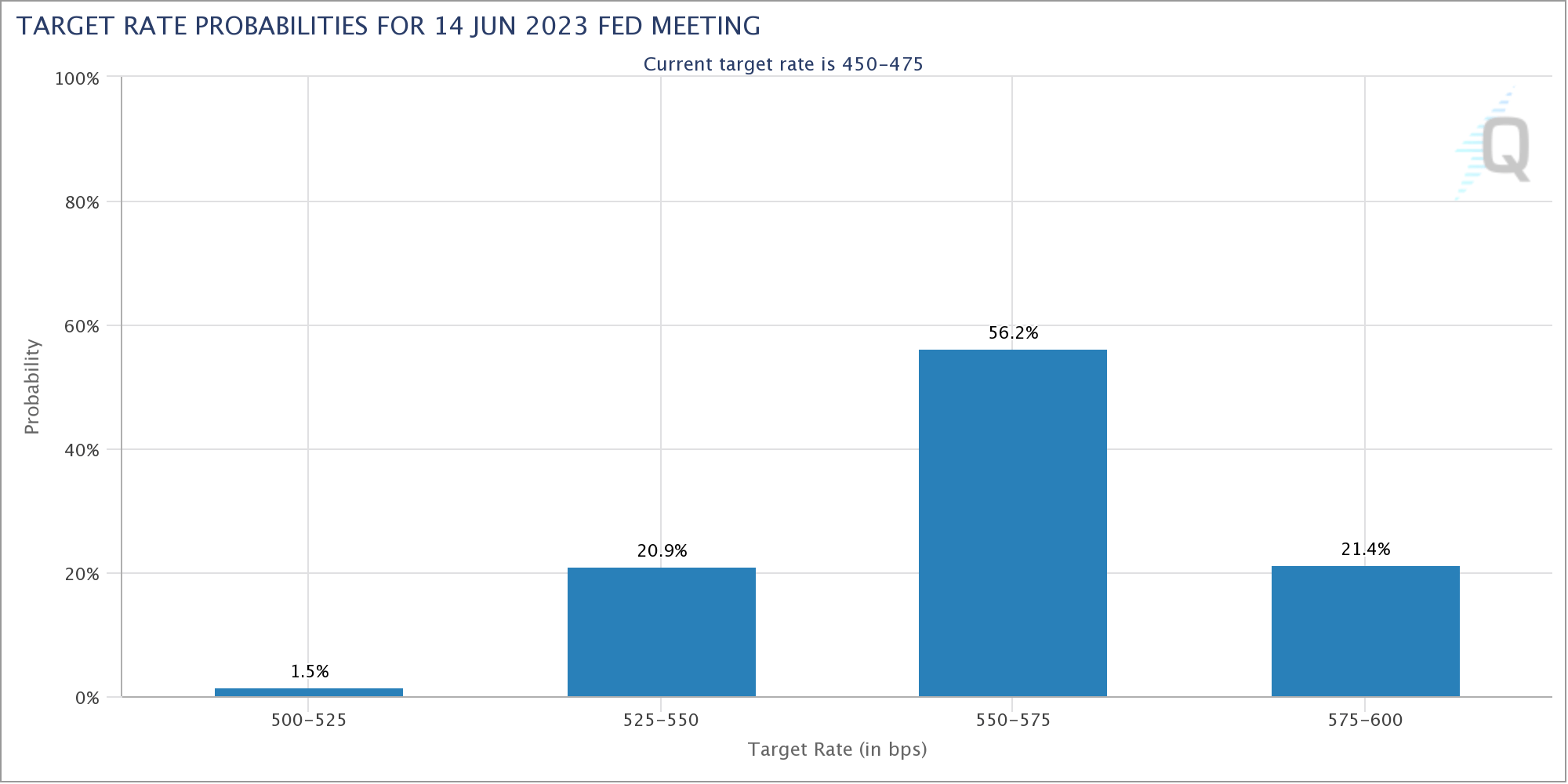

Currently, Fed Funds futures also have aggressively priced this in, with a 50bp rate hike as the most plausible outcome at the next meeting later this month. Futures also are currently implying a terminal Fed Funds rate of around 5.75% to be reached this June. Contrary to previous expectations, the first expected rate cuts have also been pushed back to January 2024.

In our view, this also shows that the market did not yet believe that the Federal Reserve is willing to hold rates higher for longer.

{kind=link}

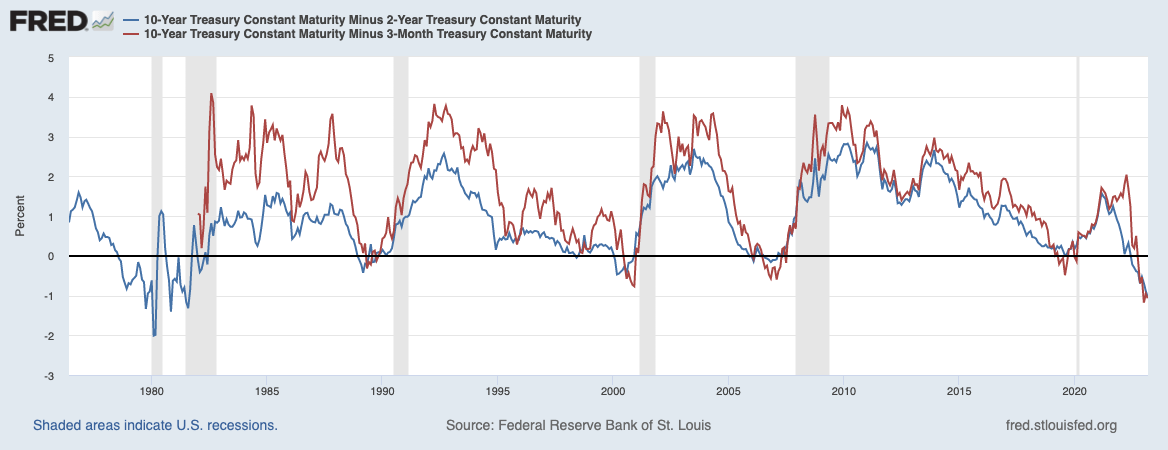

The bond market gave the same signal. While the 10-year rate did not move much and still remains around 4%, the two-year rate went up dramatically. The result: An even deeper inverted yield curve.

{kind=link}

Currently, the inversion of the yield curve is literally testing records of several decades, going all the way back to 1981. Currently, the most popular measure, the 2-10 curve , is inverted by as much as 107 bps.

An inverted yield curve is notoriously problematic in the economy because in the past it almost always indicated recession. More so, at this level of inversion, it technically always means a recession. Yet earnings forecasts still seem to indicate that all will be rosy.

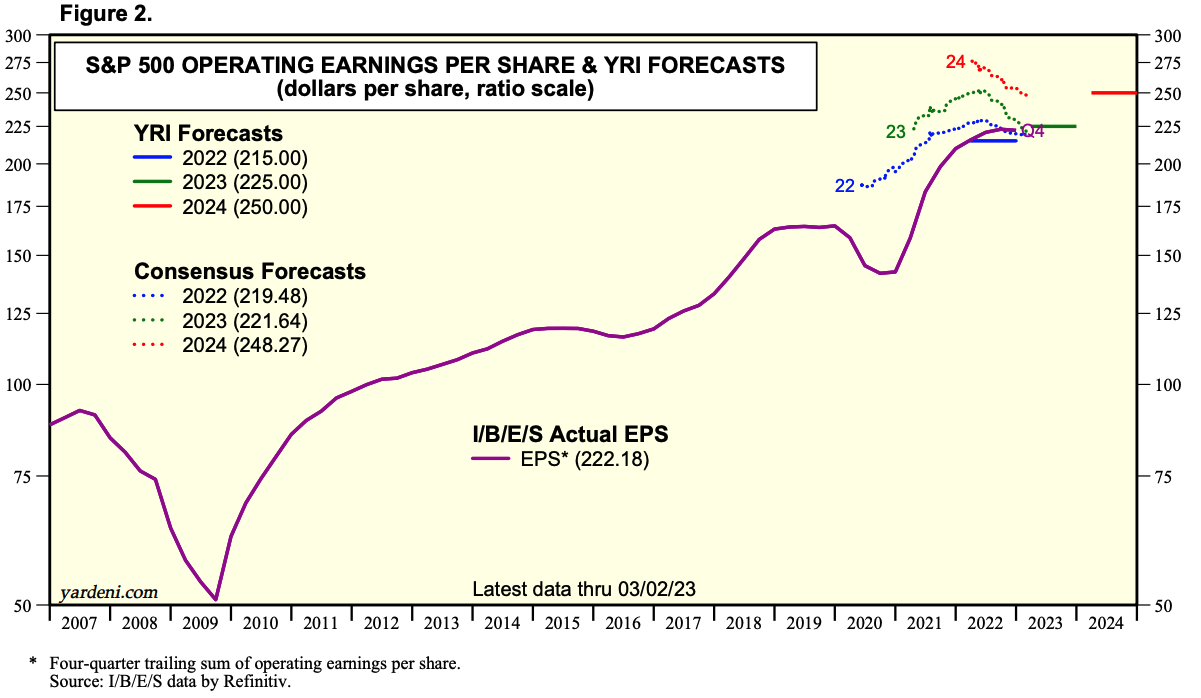

Although expectations for 2023 and 2024 have already been revised downward in recent months, profits are expected to remain the same in 2023 and rise sharply in 2024.

{kind=link}

For example, in 2008, after the yield curve was inverted less than it is now, profits plummeted completely two years after the inversion, to 50%. Now, we're not suggesting that things are the same now as they were in 2008. But the inverted yield curve still stands in stark contrast to the earnings growth of over 10% predicted for the next two years.

Hiking Until Something Breaks

On the contrary, we think that, as in 2008, the Fed is more likely to raise interest rates and keep them at the high level until something breaks. And the Fed has plenty of reasons to maintain this position.

There are still sectors where inflation is running high, the labor market is still too hot, and the Fed's biggest nightmare right now is a repeat of the 1970s , and cutting interest rates too early. In fact, they have said this over and over again at previous meetings , virtually glorifying their predecessor Paul Volcker.

This also is where it usually goes wrong: The labor market is a lagging indicator, and usually doesn't bottom out until the economy is already through the recession. Which means: If the Fed ends up waiting for the labor market to show signs of a crack, which we believe they will, they will probably end up causing a recession.

{kind=link}

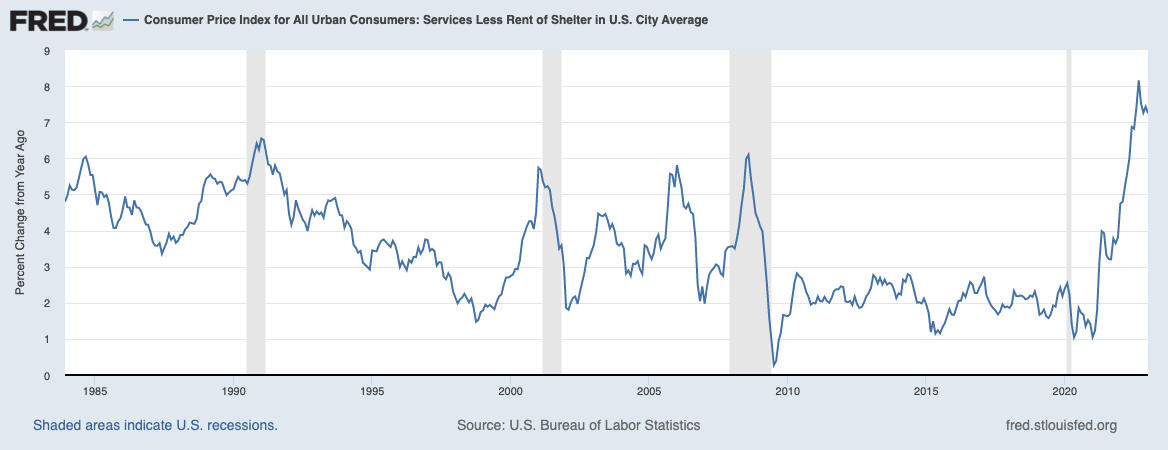

And although Jerome Powell mentioned the cooling to 4.7% in core PCE inflation, which does not include volatile food and energy prices, he particularly mentioned the very high and persistent inflation in the services sector. Even after deducting housing, which is particularly sticky and still running hot, this services index is still running as high as 7.2%.

That said, there is little sign of disinflation thus far in the category of core services excluding housing, which accounts for more than half of core consumer expenditures. To restore price stability, we will need to see lower inflation in this sector, and there will very likely be some softening in labor market conditions. (Jerome Powell, Testimony)

Even in this statement, the Fed hints that the labor market will very likely have to deteriorate before we see this kind of inflation back to the 2% target. The key factor here is also that one thing is certain at every meeting: The Fed does not even want to initiate the discussion of higher than 2% inflation .

{kind=link}

Nor is it that the Federal Reserve is blind to the slowing economy while raising interest rates so quickly. It's thereby acknowledging the slowdown in economic growth, which was also mentioned during the statement.

The U.S. economy slowed significantly last year, with real gross domestic product rising at a below-trend pace of 0.9 percent. Although consumer spending appears to be expanding at a solid pace this quarter, other recent indicators point to subdued growth of spending and production. (Jerome Powell, Testimony)

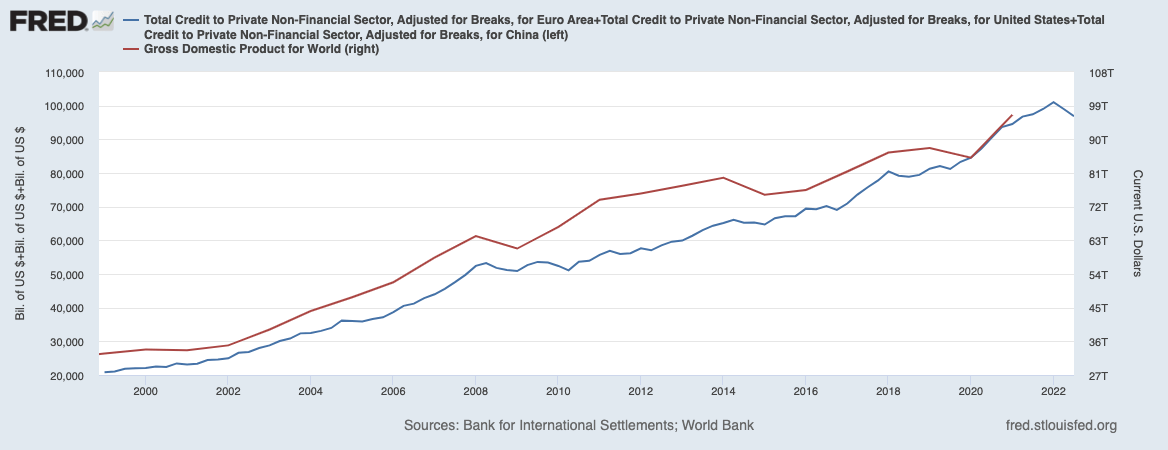

Another important metric, which we believe is sometimes overlooked, is credit growth for the private sector. Since 2022, credit growth in the largest five countries has slowed dramatically and declined in recent quarters, indicating a possible global economic slowdown. If you look at the credit impulse of all G5 countries, it is currently the weakest since 2008.

{kind=link}

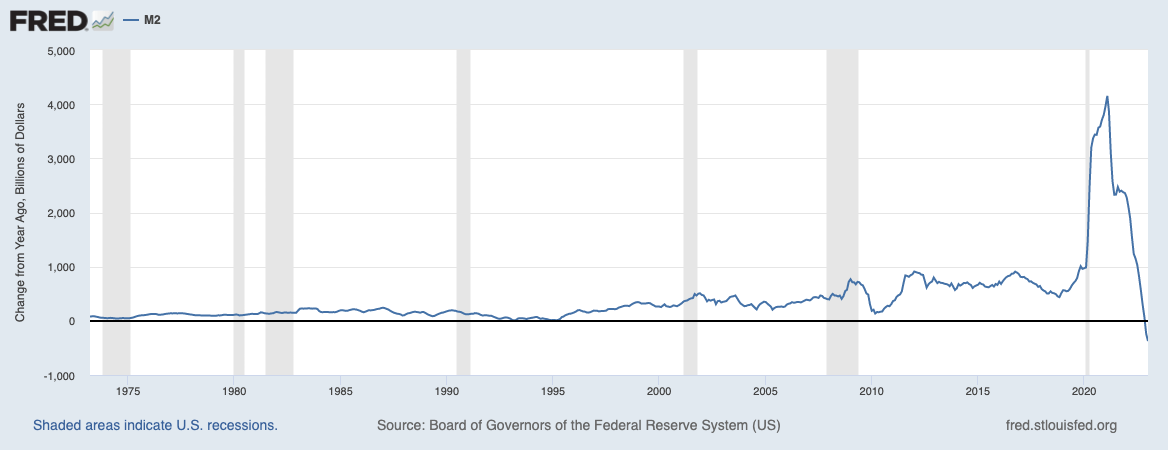

And speaking of monetary phenomena, other indicators such as the M2 money supply are also coming up with shocking numbers. After record M2 money supply growth in 2020, it has turned deeply negative for the first time.

While much attention was focused on a rate hike by the Fed of 75 bp, 50 bp or 25 bp, meanwhile they have let about $625BN of assets roll off their balance sheet since they started QT. This pace will continue at $95 billion a month, with little being said about it.

{kind=link}

All in all, we have not changed our view of the markets, and still believe that, looking at the yield curve, the Fed's relentless commitment to raise interest rates and keep them there, along with the lagging effects of monetary policy, the US economy is likely to fall into recession by the second half of 2023 to early 2024.

In our view, some of the subtle, early indicators already are starting to emerge, including the housing market, more layoffs, such as yesterday at Meta , price cuts at Tesla and a -4.6% year-over-year decline in fourth quarter earnings.

The Main Show

While Powell's comments are informative, the most important data will still be the data soon to be released for the next FOMC meeting that begins March 21. This is mainly because the Fed depends on data, and the Fed has not yet made a decision on the next rate hike.

We will continue to make our decisions meeting by meeting, taking into account the totality of incoming data and their implications for the outlook for economic activity and inflation. (Jerome Powell, Testimony)

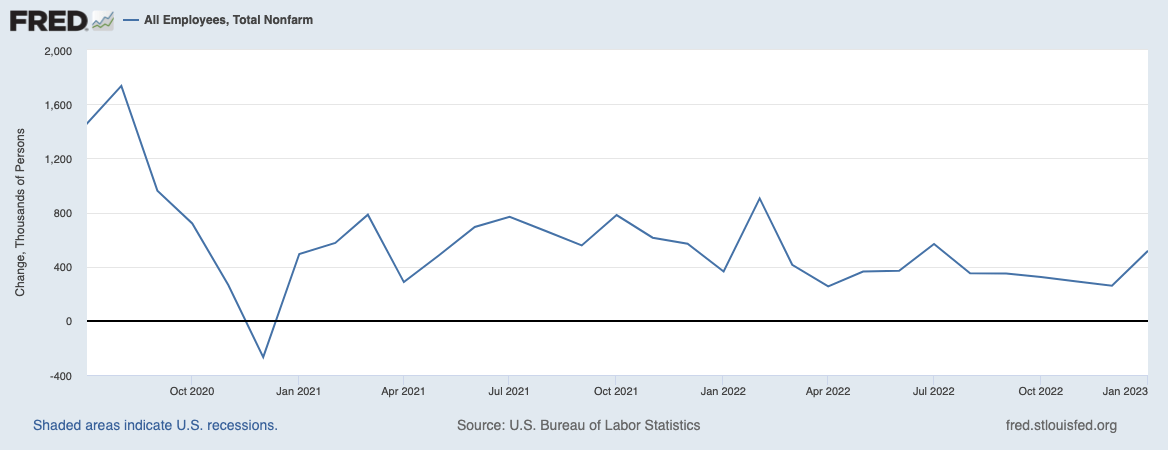

With the key word in that sentence being "totality." One such key item is total Nonfarm employment , which will be released this Friday. Last time, this figure surprised enormously, adding 517,000 jobs in January. The main question is whether this was an anomaly, as the jobs market was expected to start slowing down now that interest rates have already been raised so high.

This time the number is expected to come in at 203K. If this figure is again higher than expected, it could give the Fed more reasons to raise interest rates and hold them longer, as weaker number would be a reason to lower or slow interest rates, as the Fed has a dual mandate: Maximum employment and price stability.

{kind=link}

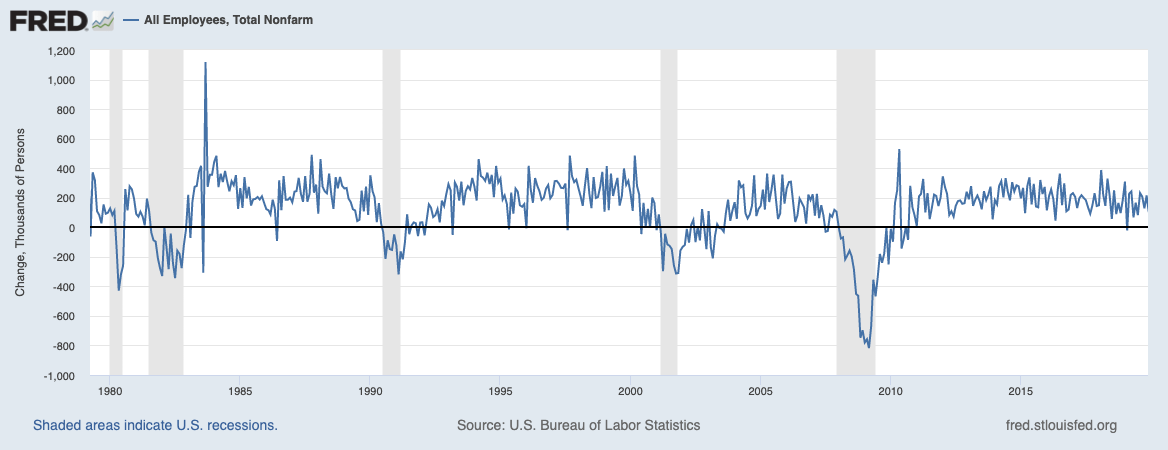

In our opinion, this reading was probably an anomaly. It also would not be the first time that employment figures have given a dubious reading, as in March 2000, for example, 485K jobs were added in the US, although there was also an inverted yield curve.

However, about three months later, in June, an initial negative reading appeared, quickly reversing the previously strong data. Again, the Fed will also consider the "totality" of the data, not just look at 1 print.

{kind=link}

Several other figures also are scheduled next week, the most important being: CPI and Core CPI on Tuesday, retail sales and PPI on Wednesday and housing data on Thursday. All of these data should be interpreted by the Fed and factored into their decision at the next meeting.

The Bottom Line

The Federal Reserve has sent a clear message about bringing inflation back to target. Nevertheless, the market still seems quite positive on earnings, in our opinion, despite several indicators pointing to a recession.

Although inflation has been moderating in recent months, the process of getting inflation back down to 2 percent has a long way to go and is likely to be bumpy. (Jerome Powell, Testimony)

In recent history, equity markets have had the Federal Reserve on their side, with long-term interest rates falling to lower and lower levels over the past 40 years, combined with generous monetary policies such as QE. This time, we're pretty sure that the Federal Reserve will continue to side with Main Street rather than Wall Street, and will not budge until inflation reaches the 2% inflation target again.

Shockingly, the earnings yield for the S&P 500 is currently only 4.69%. In the past, when there was no alternative, buying stocks at high multiples could be justified. But as it stands now, the 2-year yield is at 5.07%, providing a very attractive alternative to stocks. Not only is the front end of the yield curve cheaper priced than stocks, they're also considered risk free, compared to equities that usually suffer from earnings pressure during a recession.

In short, we would be extremely cautious about buying stocks at current levels, as we expect both earnings pressure and multiple pressure in a slowing economic environment, which forecasts do not appear to have priced in.

For further details see:

S&P 500: Federal Reserve Signals Bumpy Ride Ahead