QVML - S&P 500 Resumes Downtrend In Another Volatile Week Of Trading

Summary

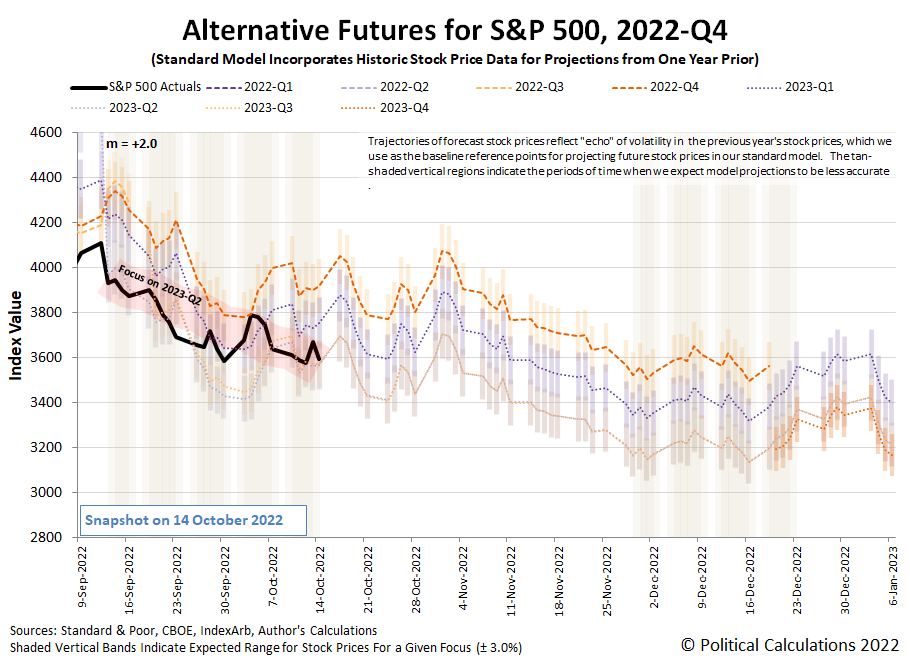

- With another higher-than-expected inflation print during the week, the S&P 500 (Index: SPX) experienced another surge of volatility during the week that was.

- But by the end of the week's trading, the index closed at 3,592.76, down 46.90 points or 1.3% from the previous week's close.

- It also ended the week right in the middle of the most recent redzone forecast range we added to the alternative futures chart several weeks ago.

With another higher-than-expected inflation print during the week, the S&P 500 (Index: SPX ) experienced another surge of volatility during the week that was.

But by the end of the week's trading, the index closed at 3,592.76, down 46.90 points or 1.3% from the previous week's close. It also ended the week right in the middle of the most recent redzone forecast range we added to the alternative futures chart several weeks ago, as stock prices resumed their downtrend.

{kind=link}

The week's most volatile action is concentrated from Thursday to Friday, 13-14 October 2022. The precipitating factor for the volatility was the higher-than-expected rate of inflation in the U.S. reported on 13 October 2022.

That news initially sent stock prices until the prospect of a full percentage point increase by the Fed at its next meeting prompted a surge in stock prices as investors shifted a portion of their forward-looking focus toward the nearer term.

But only a partial shift, where once again, the change in stock prices didn't change enough to qualify as a full Lévy flight . By the end of the week, we find the S&P 500's trajectory to be consistent with the projected trajectory associated with investors focusing their attention fully on 2023-Q2.

We'll discuss the reason why that is at the end, following our recap of the week's market moving headlines.

Monday, 10 October 2022

- Signs and portents for the U.S. economy:

- Fed on board with keeping bigger rate hikes going:

- Bigger trouble developing in China:

- IMF and World Bank getting excited about developing global recession:

- Eurozone national central banks sign onto rate hikes, lower economic growth to combat inflation:

- ECB worried they aren't doing enough and aren't doing too much to hit inflation target several years from now:

- Nasdaq registers lowest close since July 2020; chips stocks fall

Tuesday, 11 October 2022

- Signs and portents for the U.S. economy:

- Fed can't believe their hiking interest rates hasn't slowed inflation they let get out of control:

- Bigger trouble, stimulus rolling out in China:

- Bigger trouble developing in the U.K:

- Bank Of England To Global Markets: 'You Have 3 Days To Sell All The Things'

- British pension funds step up fire sales as need for cash soars

- BoE quantitative tightening likely to be delayed until later this year -fund manager

- Factbox-What are index-linked bonds and why is the Bank of England is buying them?

- IMF says high inflation to run another two years, debt-ridden nations can expect to feel pain:

- IMF chief economist says central banks' inflation fight to last into 2024

- IMF's Gopinath: Poorer nations do face big debt challenges

- IMF cuts 2023 growth outlook amid colliding global shocks

- IMF warns inflation fight, geopolitical events driving up financial stability risks

- Factbox-Ticking bomb: The risks the IMF sees to financial stability

- ECB looking to unload their expansive holdings of Eurozone government debt:

- S&P 500, Nasdaq end lower; BoE comments add to market jitters late

Wednesday, 12 October 2022

- Signs and portents for the U.S. economy:

- Fed excited to deliver more, bigger rate hikes and to start losing money:

- Bigger trouble developing in Japan:

- BOE, new U.K. government do damage control:

- ECB thinking they like more, bigger rate hikes:

- Wall St ends volatile day lower after Fed minutes, PPI

Thursday, 13 October 2022

- Signs and portents for the U.S. economy:

- Fed expected to continue more, bigger rate hikes; say all's okay for financial stability:

- Japanese government see more inflation, crank out more stimulus:

- ECB ready to shed its excess Eurozone government debt holdings, getting excited for more rate hikes:

- Wall Street ends up 2% after sharp reversal; technicals help

Friday, 14 October 2022

- Signs and portents for the U.S. economy:

- Influential Fed okay with rapid ramp up to peak Federal Funds Rate, another Fed caught with their hand in the insider trading cookie jar:

- China economy rebounded in 2022-Q3, but bigger trouble developing from zero-COVID policies and more stimulus on tap:

- Liquidity problems prompting central bankers to coordinate actions more:

- Despite inflation, BOJ determined to keep never-ending stimulus alive while JapanGov claim they've got the yen covered:

- ECB embrace Eurozone recession to fight inflation:

- Wall St drops as consumer data stokes inflation worry

The CME Group's FedWatch Tool continues to project a three-quarter point rate hike when the FOMC next meets on 2 November 2022, but now signals it will be followed by another on 14 December (2022-Q4).

In 2023, the FedWatch tool now projects quarter-point rate hikes in February and March (2023-Q1), setting the top for the Federal Funds Rate's target range at 5.00-5.25%. However, that could reverse as earlier as May (2023-Q2) as developing recessionary conditions force the Fed to change its rate hike tactics.

The Atlanta Fed's GDPNow tool 's projection for real GDP growth in the just-ended calendar quarter of 2022-Q3 dipped slightly from +2.9% to +2.3% as the U.S. economy rebounded from the week first half of 2022, as supported by recent trade and atmospheric CO? data. The Bureau of Economic Analysis will provide its first official estimate of real GDP growth in 2022-Q3 on 27 October 2022.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

S&P 500 Resumes Downtrend In Another Volatile Week Of Trading