HYG - S&P 500: Still On The Sidelines? We Break Down The Playbook

2023-08-04 10:55:15 ET

Summary

- We present a playbook for the S&P 500 Index specifically for investors who are still sitting on the sidelines.

- Our favourite playbook tactic at the moment is to rotate portfolio allocation towards value so that investors can stay fully invested in equities while managing downside risks.

- Our second tactic involves moving into high-yield bonds if reducing equity exposure is absolutely necessary for the investor. High yields will allow investors to earn a decent return without equity risk.

- Lastly, we explore overlaying a long volatility strategy on top of an existing equity portfolio as a solution to hedge against equity downside risk.

- However, because the cost of protective puts on the S&P 500 Index has risen this week the long volatility strategy would be costly. Nonetheless, the strategy is still relevant for investors looking to hedge against equity risk.

For investors who missed the equity market bottom in October 2022 and the subsequent rally, the consequences of being caught on the wrong side of the trade are beginning to haunt them. The true cost of missing a bull market is not limited to just a bruised ego or forgoing a year's worth of returns. Missing out on a 26% gain on the S&P 500 Index ( SP500 ) since October is a permanent drag on the long-term performance of a portfolio. At its worst, it inflicts a psychological impediment to making sound investment decisions thereafter.

Because equity valuations have recovered while downside risks continue to give hope that prices may pull back, many argue that "valuations are no longer attractive" and use that as an excuse to not invest in equities today. Furthermore, with yields on cash and short-dated bonds at the highest levels in decades, missing out on the equity bull market doesn't feel as costly as it should. As such, waiting for a meaningful pullback in equities or hoping that some bearish scenario will eventually play out, is likely to be the preferred game plan for these investors for now. Yet deep down, these investors may be feeling uncomfortable with that game plan. What if this bull market is genuine and prices don't look back?

{kind=link}

TradingView.com, Stratos Capital Partners

If what we have described matches your situation, the good news is that we think it is not too late to catch up with the equity bull market. In this article, we present a playbook for the S&P 500 Index specifically for investors who are still sitting on the sidelines and are caught in a dilemma on whether to chase the market or wait for a pullback. We explore several options that investors can pursue to catch up with the bull market without resorting to leverage or having to take on unnecessary risks. All is not lost, and there is certainly no need to become a perma bear.

But before we dive into the playbook, it might be worthwhile to assess the psychology that may be holding many investors back from investing in equities at the moment.

The Psychological Challenge Of Buying High & The Essence Of Value

Investors who have committed the same mistake of missing previous bear market troughs in March 2020, and March 2009, would empathise with how challenging it is to buy an asset after watching it spike by 20% or more. But staying on the sidelines would prove to be an even bigger mistake as previous bull markets never looked back and went on to make new highs thereafter. Very rarely do bull markets pull back meaningfully to offer investors a second chance to hop on. Even in those rare occasions where markets do pull back meaningfully, they are usually accompanied by fresh risks justifying the renewed pessimism. Thus, investors often find themselves back in the same situation of indecisiveness and fear of taking the shot.

The challenge associated with buying an asset only after its price has surged is primarily psychological. Common sense would probably suggest that buying something at a high price is generally a bad deal. That logic is fundamentally sound and adequate when applied to regular goods and services that we purchase for consumption. However, common sense logic often results in suboptimal decisions when applied to productive assets that grow in value over time.

Deciding whether to buy a productive asset based on the performance of past prices is a critical mistake. This is because the value of a productive asset has little to do with past prices or the returns that it can generate today. Instead, the value of an asset is mostly dependent upon the returns/cashflows that the asset is expected to generate and grow into the future. And because fundamentally sound and quality assets grow over time, prices of these assets should also drift upwards over time, regardless of short-term swings in sentiment.

In contrast, the price of regular goods reflects the immediate benefits that arise from the consumption of that good. This fundamental difference between productive assets and regular goods is why large swings in asset prices are common, and why these price swings often seem to be driven by sentiment rather than economic fundamentals.

The problem of investing can be relatively straightforward if one clearly understands one's objective for investing in an asset. If the goal is to invest in an asset that is expected to grow in value over time, then it is only reasonable to pay an adequate price multiple for that growth. Then the decision to invest would boil down to the investor's expectations for the pace of growth, the longevity of that growth, as well as what would be a reasonable multiple to pay based on historical trends. Because young companies may hold immense potential for growth in the long term but are making temporary losses during their initial stages of growth, it may even be appropriate to buy loss-making companies. So long as you believe that future growth will materialise.

So why do some investors become indecisive when investing in equities? Usually, the underlying reason is either fear or greed. Either the investor is fearful of suffering potential losses by investing at a price that is high relative to the past, or the investor is greedy and hopes to catch the stock only at the best price possible. With careful introspection, the root cause of indecisiveness and poor investment judgement often boils down to this senseless obsession with price instead of investing in value.

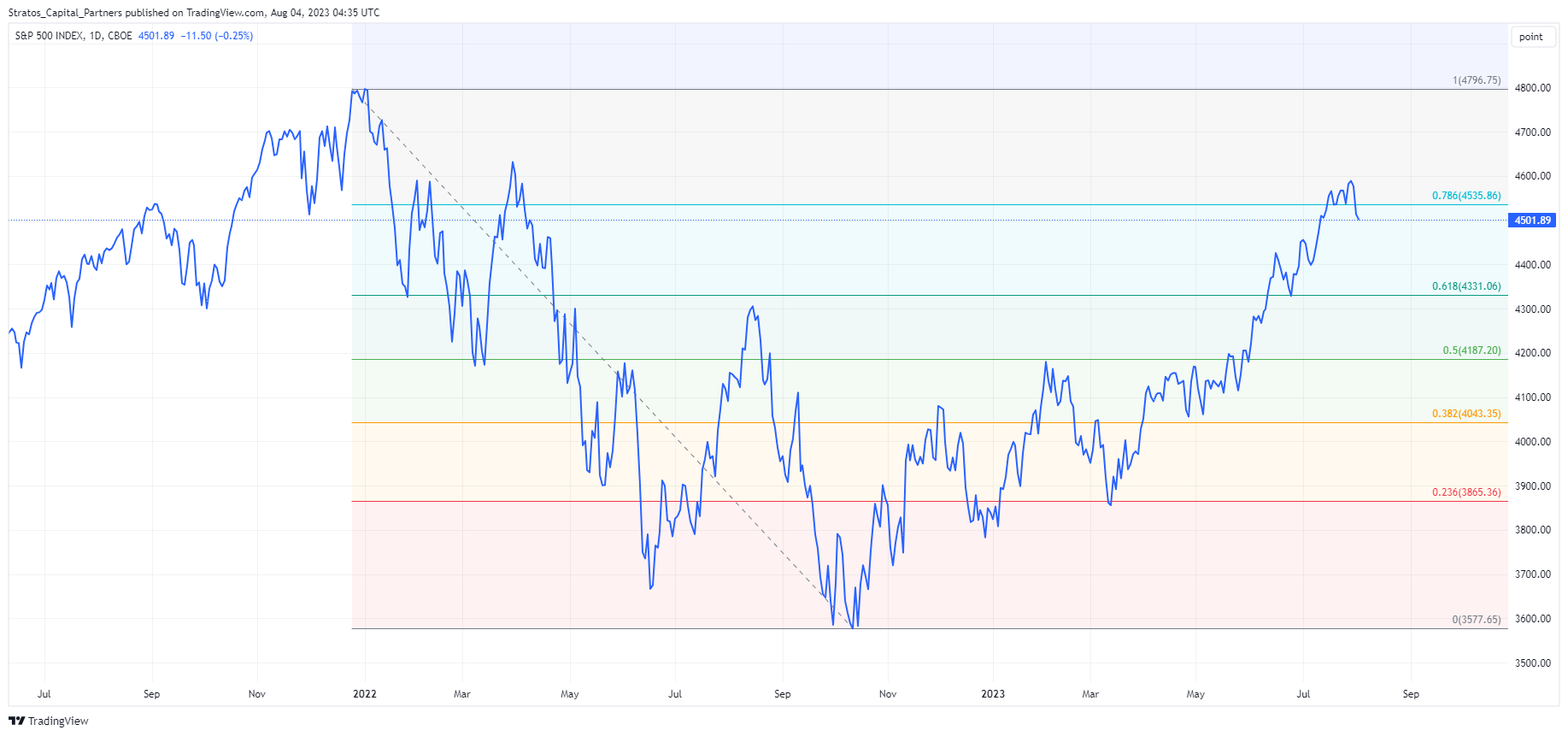

Don't get us wrong, the price we pay for an asset matters. However, prices are only meaningful and relevant within the context that one has determined the potential value of an asset. Prices can then be judged as being too cheap or too expensive. If investors are rational long term, then prices should converge towards value. A picture is worth a thousand words, and the chart below nicely illustrates the market's fickle sentiment and senseless obsession with price, versus the steady upward drift in value that prices inevitably converge towards over time.

The Irrelevant Investor

Now that we have properly addressed the psychology and root cause of poor market timing, let us explore our playbook of ideas that could help investors catch up to the S&P 500 Index.

S&P 500 Mostly Driven By Big Tech, So Look Elsewhere To Play Catch Up

Our favourite playbook tactic at the moment is to rotate portfolio allocation towards value so that investors can stay fully invested in equities without the risk of missing a bull market, and still be able to manage risk and improve returns. We recently published an article highlighting our view to rotate out of big-tech and AI-related stocks and to invest in homebuilders, biotechnology, and cybersecurity stocks, which we think are likely to outperform in the medium to long term.

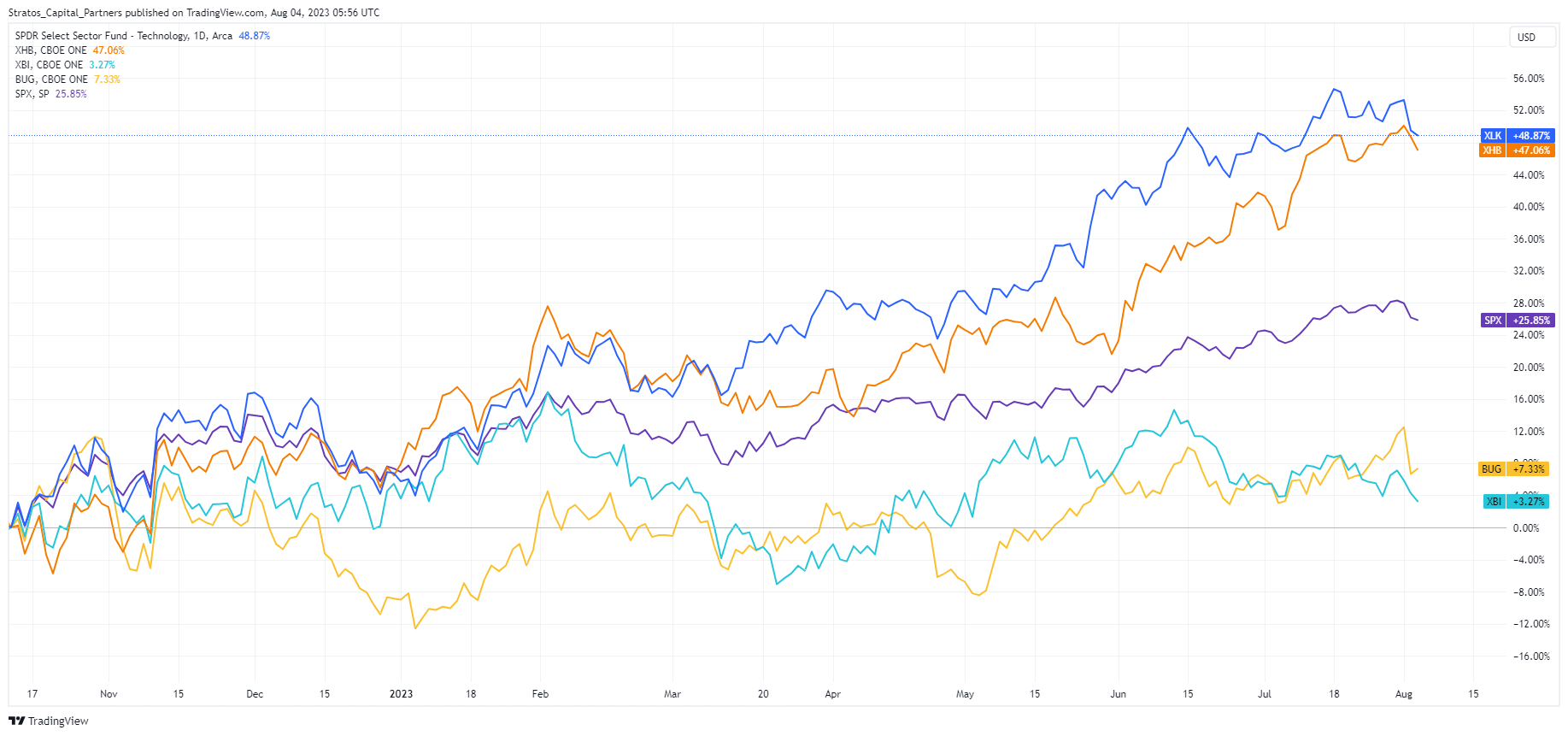

In the chart below, we compare the price performance of the S&P 500 Index ( SP500 ) versus ETFs representing the sectors we have mentioned above including the Technology Select Sector SPDR Fund ETF ( XLK ), SPDR S&P Homebuilders ETF ( XHB ), SPDR S&P Biotech ETF ( XBI ), and Global X Cybersecurity ETF ( BUG ). The chart shows performance beginning from October 12, 2022 when the S&P 500 Index bottomed out.

{kind=link}

TradingView.com, Stratos Capital Partners

As we can see, big tech and homebuilders have been outperforming the S&P 500 Index by a substantial margin since October. Because the S&P 500 has also become heavily weighted towards big tech over the years, the strong performance of big tech has also become the biggest driver of the S&P 500's gains to date. Meanwhile, other tech-related sectors such as biotechnology and cybersecurity have been lagging far behind with single-digit gains.

So just based on price performance alone, we can loosely infer that big tech and homebuilders have become much more expensive since October while biotechnology and cybersecurity could potentially provide a good bargain for playing catch up to the market. Of course, looking at price is not enough, so let us turn to valuation multiples.

The table below shows the current P/B and P/E ratios as well as sales growth for the respective ETFs (sorted by P/B). Here we can see that XLK is the most expensive ETF among the group with the highest P/B of 7.7x, and the second highest P/E of 26.8x. To judge if such lofty price multiples are realistic, we can compare recent sales growth. Here we see that XLK's sales growth is middling at 12%, just slightly above the broader SPY.

Morningstar, Stratos Capital Partners

In comparison to the next most expensive ETF on the list BUG, we note that BUG is made up of mid-sized companies that are still in their early stages of growth and profitability compared to the much more mature XLK. Thus, BUG has the highest P/E despite having the slowest sales growth. Admittedly, BUG presents a mixed picture. While price performance suggests BUG is cheap, valuation multiples suggest BUG may be an expensive ETF.

From our perspective, we like BUG because of the sector's long-term growth prospects, which we think justify the higher multiples. For investors who are investing long-term, we think BUG is attractive given the sector's long runway for growth. However, we acknowledge that although BUG may appear cheap based on recent price performance alone, BUG may not be an ideal choice for more conservative value investors.

Recall that XHB has been a top performing sector this year tracking closely behind big tech. However, if we look at valuation multiples and sales growth, XHB is still the cheapest in terms of price multiples with relatively strong growth. XBI is also a great choice for value given that it is delivering the strongest sales growth while price multiples are attractive.

Dislike Equity Exposure? Stay On Track With High Yields

Although we repeatedly recommend our readers stay fully invested in equities, we understand that some investors may be adamant about taking some profits off the table instead of pursuing tactical rotational strategies. In the case where reducing equity exposure is absolutely necessary, then we offer our second favourite playbook tactic. We recommend that investors at least reallocate to high-yield fixed income.

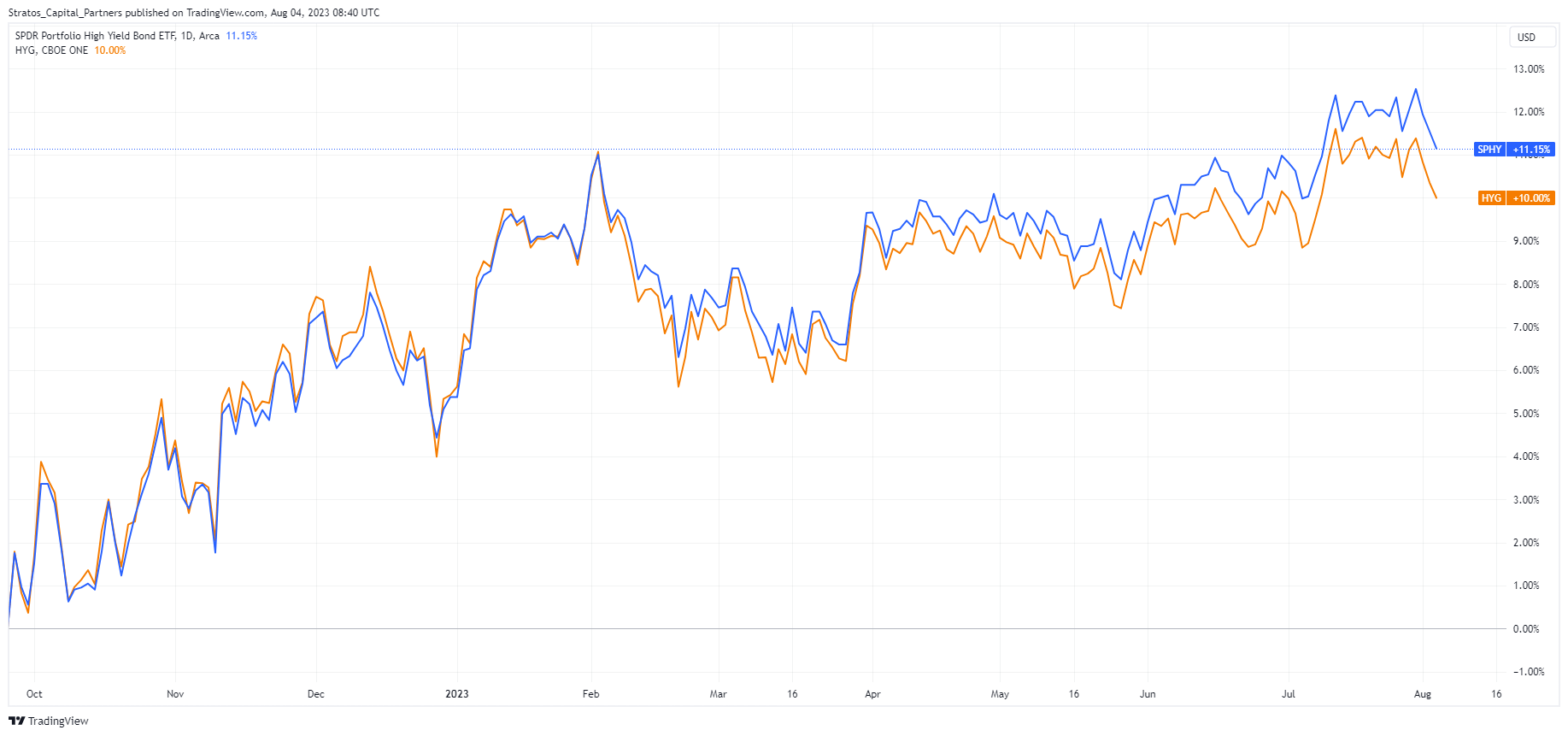

We have also published articles covering several high-yield ETFs including the iShares iBoxx $ High Yield Corporate Bond ETF ( HYG ) as well as the SPDR Portfolio High Yield Bond ETF ( SPHY ), and we continue to give a "Strong Buy" rating to both.

When we initially published our bullish view on high-yield ETFs such as HYG and SPHY, our original intention was to set ourselves up for peak yield and for the potential gains to come when the Fed normalises monetary policy. Our thesis was that the economy would hold up well enough such that we would not see defaults rise too dramatically to the extent that these ETFs would rack up losses. And while we wait for monetary policy to eventually normalise, we would be earning a very attractive yield on these investments.

Thus, high-yield ETFs are ideal for investors that are worried about short-term equity downside risk but are happy to earn ~7%-8% yields, which is close to long-term equity returns, while patiently waiting to reap larger gains when the Fed eventually brings interest rates back to a more neutral level of 3%.

{kind=link}

TradingView.com

As the chart above shows, investors who invested in these high-yield ETFs since October would have earned a decent 10%-11% return to date, including dividends. Our bullish view on high-yield bonds still remains relevant in today's market environment. HYG and SPHY are both suitable alternatives for investors looking to avoid short-term equity downside risk but would like to still be able to capture decent returns over the next 12 to 24 months.

Hedging With The VIXY

Our final playbook tactic involves overlaying a long volatility strategy on top of an existing equity portfolio. We explored a volatility strategy of our own in some depth back in November 2022 in an article titled "VIXY And SVXY: Exploring Strategies To Profit From Fear" and we recently executed on the strategy by taking a bullish position on the ProShares VIX Short-Term Futures ETF ( VIXY ).

Given that volatility in the equity market has jumped slightly this week, the cost of buying protective put options on the S&P 500 Index is now no longer as cheap. Thus, such a strategy that involves hedging against equity downside risk would entail paying a costly insurance premium. Nonetheless, we still appreciate the relevance of using a long volatility strategy to help protect against downside risk while staying fully invested in equities.

For further details see:

S&P 500: Still On The Sidelines? We Break Down The Playbook