SCPPF - S4 Capital: Bargain Buy For The Digital Economy

2023-06-06 21:50:08 ET

Summary

- S4 Capital's share price has suffered due to delayed accounts, key man risk, uncertain digital ad market outlook, and an unproven business model.

- The company has experienced strong business momentum and organic growth rates, with revenue surpassing £1bn for the first time in 2021.

- Despite risks, the current share price is considered a long-term bargain, with potential for increased value through improved profitability and succession planning.

After Sir Martin Sorrell left the shell-company to global ad giant he had created in WPP ( WPP ) back in 2018, he went off and bought another shell company, which he promptly renamed S4 Capital (SCPPF), to turn into a digitally-focused marketing services agency. The shares have had their ups and downs. I see risks but still consider the current share price a long-term bargain. I maintain a “Strong Buy” rating and have recently increased my own position.

A Bumpy Road

I last covered the company in April 2022, in S4 Capital: A Big Bump In The Road . Due to the uncertainty surrounding delayed accounts, I assigned a “hold” rating. That accounting issue has now long since been resolved, so I am reverting to my historical rating of “Strong Buy”.

The accounting issue has been deeply damaging for the share price, but it is not the only thing.

{kind=link}

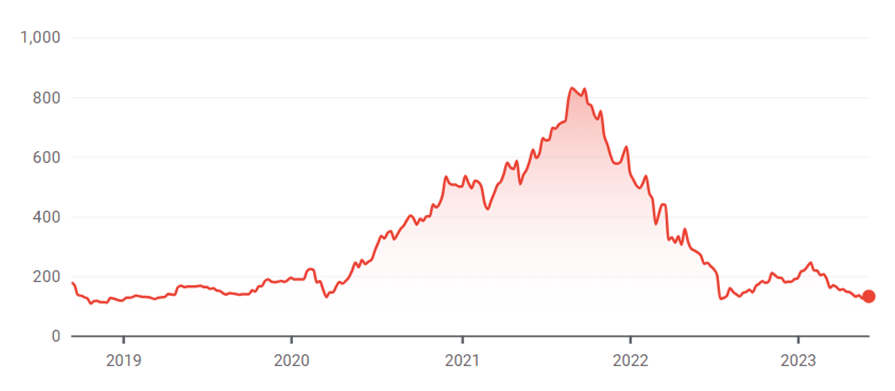

Here are the various factors I think have contributed to the rapid decline of the S4 share price after a great first couple of years (it is now back to roughly where it was as a shell company before Sir Martin got involved).

- Delayed accounts . Last year, final accounts were delayed twice. That undermined confidence for many investors. The accounts showed nothing untoward and Sir Martin made it clear he intended for there to be no recurrence, with financial controls being tightened up.

- Key man risk . It was revealed in February that Sir Martin was undergoing serious medical surgery. Since then the shares have declined 44%. As he remains in charge, I see that as an overreaction. But it does point to the key man risk here (flagged in previous pieces on SA). Despite having around 9,000 staff worldwide, S4’s identity remains indelibly linked to its founder.

- Uncertain digital ad market outlook . Investors have been concerned that a declining ad market in a recession could hurt demand for S4’s services. The company in fact expects continued growth, noting in its most recent trading update, “We remain cautiously optimistic for the rest of the year, despite a slowdown of forecast growth rates in our two major addressable markets to 7-10%”.

- Unproven business model . One growing pain for S4 over the past 18 months has been rightsizing its cost base and what that means for profit margins. That seemed to hurt the investment case for the company, even though it has been working to keep costs in check. It remains lossmaking – last year’s loss rose 180% to £160m. It remains to be seen whether the business model here really can generate sizeable profits in the long run.

One additional concern I have is the lack of director buying. No directors have bought this year, including Sir Martin and Scott Spirit, both of whom were previously buying at a much higher share price.

Clearly, then, there are risks here. The chart above is a not a pretty sight.

Strong business momentum

Set against that, though, is the growth we have seen at S4. The accounting delays leading to a share price tumble meant that the company became less willing to use its stock as currency for M&A, which had been a key growth driver for the firm. Even without the benefit of M&A, though, organic growth rates are strong.

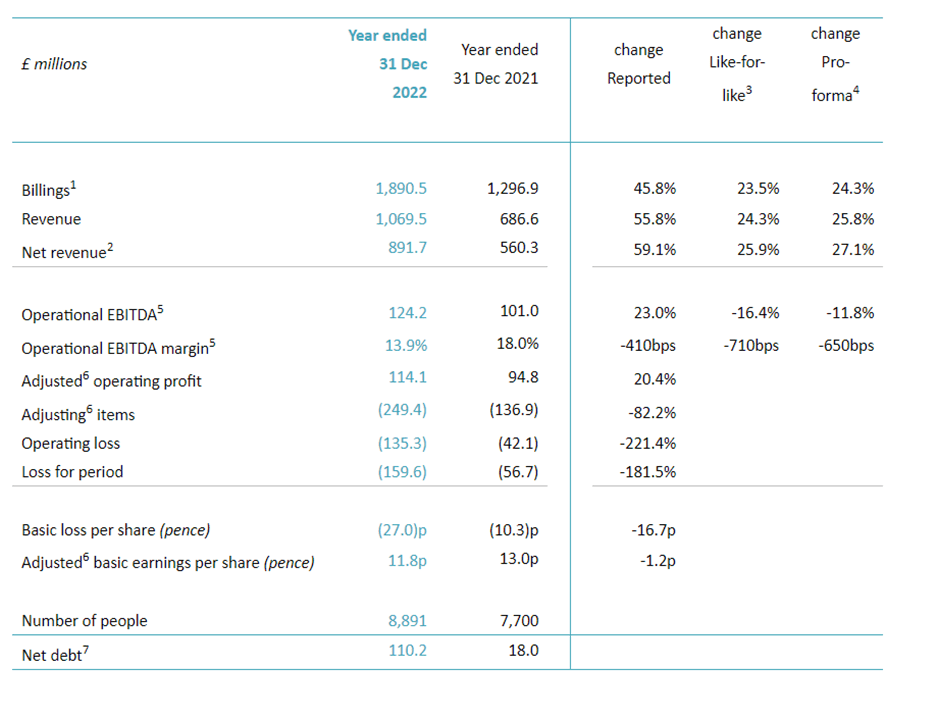

Here’s a snapshot from last year.

company final results announcement

{kind=link}

S4 is clearly going gangbusters. My key concern financially is the losses and debt. The company expects net debt to rise this year, as it pays compensation for historical M&A. But next year, that ought to fall away. Alongside an improved operational model, I therefore hope that ongoing strong revenue growth ought to see losses fall back next year and perhaps even turn into a profit.

S4’s business model has been covered in depth before on SA (starting with A Rising Star In Online Media: S4 Capital , since when the basic model has remained unchanged). I think what we see now is that the model is delivering when it comes to revenue growth. Revenue last year topped £1bn for the first time (against a current market cap of £760m).

Ongoing sales growth sets the foundation for long-term success: what is needed now is conversion to profitability. Declining merger payments, economies of scale and tighter cost control ought to enable that, in my view.

Bargain Price

For all of that, I think the current share price looks like a bargain. While the Trade Desk isn’t an exact comparator as a business, it comes close. Whereas S4’s price-to-sales ratio last year was 0.7, The Trade Desk’s was 23. Sir Martin’s track record at WPP ought to give S4 a premium if anything (arguably in 2020-21 it did, but not now). But even ignoring that, and allowing for racier tech valuations Stateside than in the London market, that suggests that S4 is an absolute bargain relative to its peers. (Indeed, many S4 shareholders have suggested that simply gaining a U.S. listing could immediately unlock substantial value at the firm, which does the majority of its business in North America).

What will it take to unlock this? Great revenue growth has not been enough so far. Maybe a clearer path to profit is needed. Certainly, confidence about both Sir Martin’s health and robust succession planning could both help. The ad outlook isn’t helping and S4 may continue in a rut for a while. Ultimately, though, I think today’s price is a deep bargain for the long-term investor.

For further details see:

S4 Capital: Bargain Buy For The Digital Economy