SAABY - Saab Benefits From Ukraine War Requirements

2023-05-19 15:23:56 ET

Summary

- Saab AB (publ) saw its order intake surge.

- Saab results are surging as well, with front-loaded backlog.

- The company eyes 15% sales growth this year and profit to grow even faster.

You might know Saab AB (publ) ( SAABF ) as the manufacturer of cars. The car manufacturer was spun off and partially owned by General Motors Company ( GM ), and fully owned between 2000 and 2010, after which it was sold to Spyker Cars, which eventually went bankrupt. In this report, I want to focus on the other part of Saab, which focuses on aerospace and defense. With Defense budgets expanding, most notably in Europe, it is interesting to provide coverage on the European defense names as well.

About Saab: A Multi-Domain Defense Specialist

Saab AB is a Sweden-based company offering products and services ranging from military defense to civil security. The Company’s operations are divided into six business areas. The Aeronautics department includes the development of civil and military aviation technology, including the Gripen and Unmanned Aerial Systems. The Dynamics comprises a product portfolio of weapon systems, such as support weapons, missiles, Remotely Operated Vehicles and signature management systems. Through the Surveillance unit, the company provides solutions for safety and security, for surveillance and decision support, and for threat detection, localization, and protection, while Saab Kockums provides naval products.

Strong Order Intake For Saab

{kind=link}

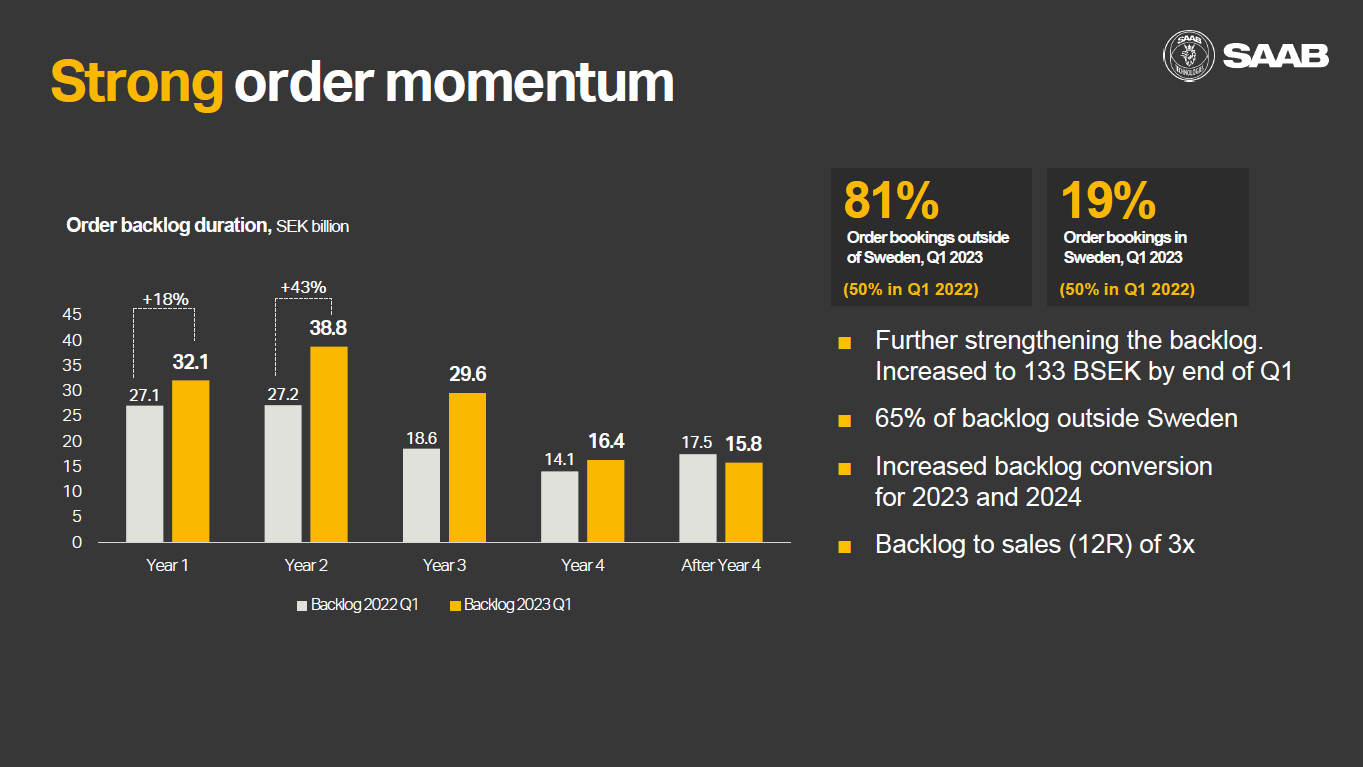

When I cover companies, I play very close attention to the slides they provide to investors and analysts. To me, it is very important to have a slide deck available that shows the strengths of the businesses as well as the challenges. A company that is not able to present itself in a good way to investors is also less likely to appeal to investors. Saab is doing a pretty good job, and it shows in the presentation of their order inflow composition. Not only to they present the backlog, which grew 27%, but they also show that a significant growth in the backlog is achieved in year two and three, with higher backlog conversion already expected this year and next year.

Saab Books Strong Top And Bottom Line Growth

{kind=link}

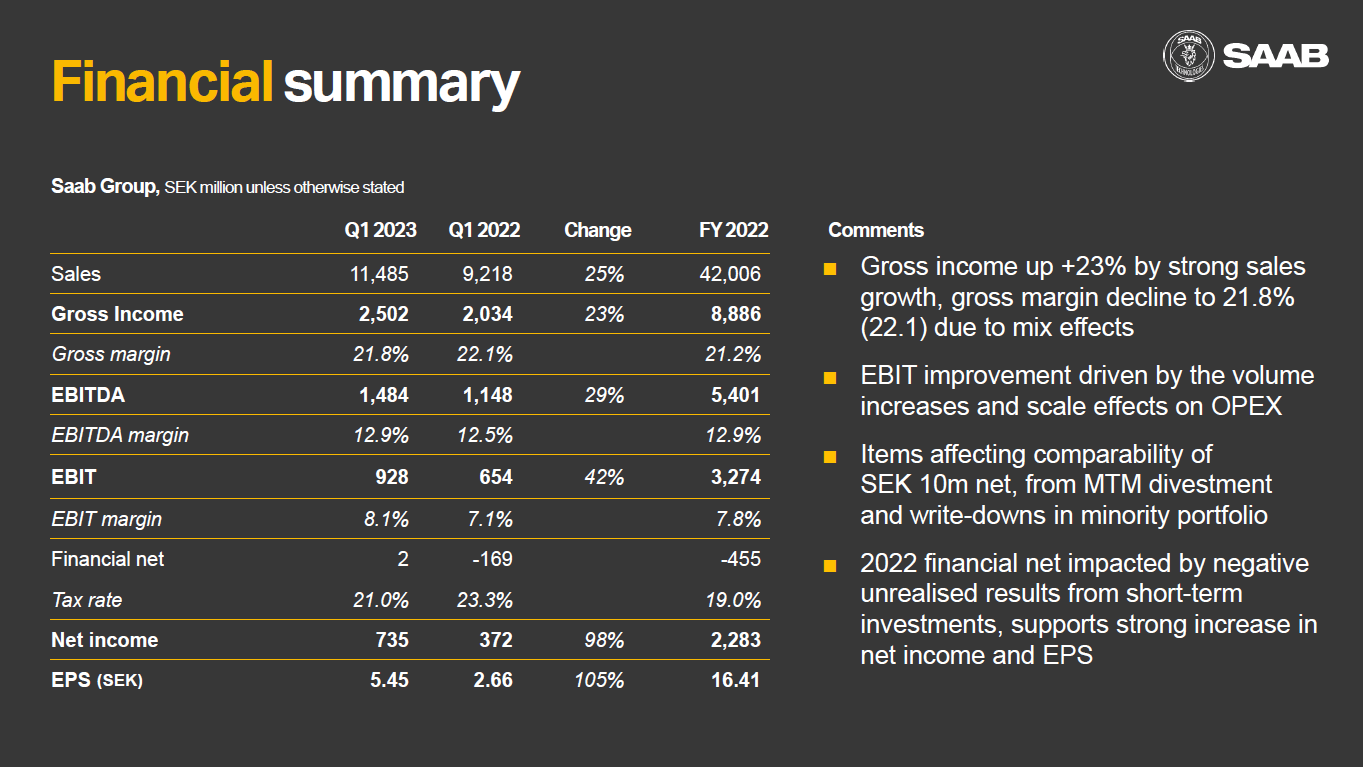

In the first quarter , sales grew by 25% and that growth did translate to the bottom with 29% higher EBITDA, 42% higher EBIT and net income almost double. The Aeronautics segment saw no sales growth and its EBIT dropped 18%, driven by T-7 Red Hawk ramp up and lower Gripen sales. With expanding defense budgets, the aeronautics division might actually be suffering some headwinds. The selling point of the Gripen fighters such as Gripen E Series is that it is a more affordable solution compared to, for instance, the F-35 from Lockheed Martin Corporation (LMT). With expanding defense budgets, more countries have the funds to consider the F-35. It’s still a very expensive piece of defense equipment to procure, operate, and maintain, but increased defense budgets ease the burden somewhat.

The Dynamics department, which sells the NLAW system used in Ukraine, saw strong sales in the quarter, up 51% year-over-year with EBIT growing 52%. This is also an area where production capacity is being ramped up so more growth can be expected. Similarly, in Surveillance, increased demand for surveillance provides significant opportunities. Sales grew 25%, while EBIT grew 21%, indicating a slight weakening in the margins. Naval system sales increased 54% while after market sales and favorable mix drove a 163% increase in EBIT. Combitech, which provides solutions in the areas of digital security, IT and AI amongst others, saw 22% sales growth and 37% EBIT growth. So, overall, we saw strength in all but the Aerospace segment.

Saab Positions For 15% Growth

{kind=link}

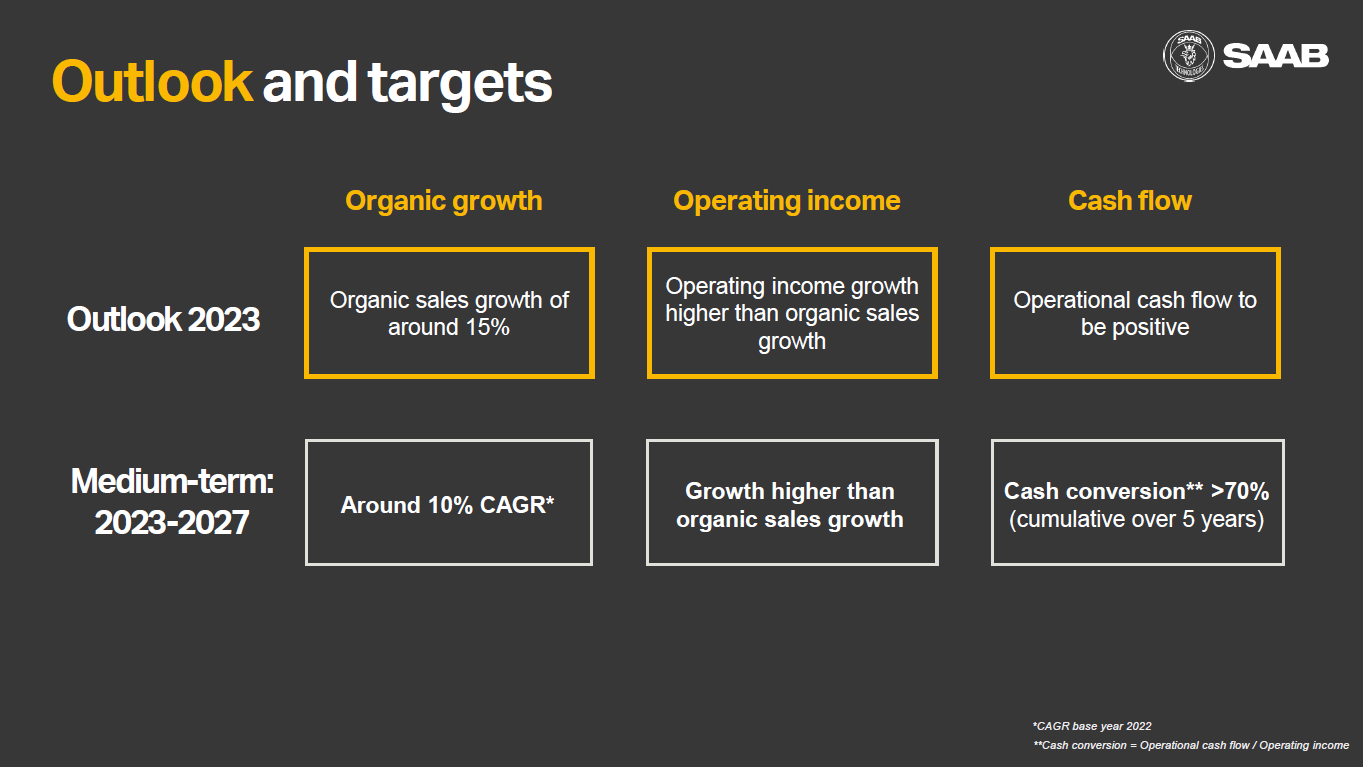

For the year, Saab expects 15% revenue growth and profits to grow faster than the sales growth. Similarly, for the medium-term, 10% growth is expected, with income outpacing said sales growth. Increased demand for defense equipment and services is a clear driver of the growth in the coming years, with sales potential related directly to Ukraine and increased NATO defense budgets. In that regard, Saab is not that different from other European defense contractors that also see significant opportunity to capitalize on the increased defense budgets on the European mainland.

Is Saab Stock A Buy?

I believe it is. We are in the early innings of increased defense equipment demand translating into sales, and Saab is already benefiting. I don’t see that changing in the near future, and based on an enterprise to EBITDA valuation, Saab is undervalued compared to peers as well as its median EV/EBITDA. I believe that the stock should be trading at least at $72.50 per share, giving it north of 25% upside.

Conclusion: Saab Is A Buy On A Strengthening Defense Environment

While the focus is primarily on U.S. defense contractors, I do believe the European ones offer significant upside. Investing is less popular in Europe, but that is changing somewhat in recent years. Perhaps Defense companies in Europe will also benefit from this, as the demand to profit translation might be noticed by investors.

For further details see:

Saab Benefits From Ukraine War Requirements