SBS - Sabesp: Privatization Just Around The Corner Q3 Results Still Provide Room For Upside

2023-11-30 06:29:01 ET

Summary

- Privatization of Brazilian water management company Sabesp is progressing, with a likely completion by the first half of 2024.

- The regulatory terms of the privatization will determine the company's long-term efficiency and potential for growth.

- The optimistic scenario envisions efficiency gains and a potential EV/RAB increase to 1.5x, suggesting a substantial upside.

- Pessimistic scenario considers onerous clauses, potential EV/RAB decrease to 1x, implying downside.

- Sabesp's Q3 results showed a decrease in net profit but strong EBITDA growth and progress in its voluntary severance program.

In my previous article discussing the water management and sanitation company of the Brazilian state of São Paulo, Companhia de Saneamento Básico do Estado de São Paulo - SABESP (SBS), the investment thesis has been centered around the ongoing privatization of the company, which is now in its final stages.

While there are still risks and uncertainties surrounding the privatization process, particularly in the ongoing discussions within the São Paulo state legislature, the likelihood of Sabesp being privatized in the first half of 2024, or possibly as early as December 2023, has significantly increased with recent actions taken by São Paulo state legislators.

The critical question at this juncture revolves around the regulatory terms that will be deliberated among lawmakers. It remains to be seen whether these terms will benefit the company's efficiency in the long term or mirror the current regulations, which could be detrimental to Sabesp's efficiency gains forecasts.

Furthermore, the company reported its Q3 quarterly results on November 10th. Despite being underwhelming, with a year-over-year decrease in net profit, Sabesp demonstrated strong EBITDA growth and made substantial progress in its voluntary severance program (VSP).

Despite the market's bullish reaction to the favorable Q3 results and the significant progress on privatization in recent months, Sabesp's shares have surged by 53% since the beginning of May this year. This indicates a more robust valuation, leaving little room for negative news regarding privatization issues. However, there is still potential for upside, especially if the more optimistic scenario due to privatization materializes.

Privatization Updates: Accelerating Progress

In my recent articles covering Sabesp, privatization has been advancing positively. The operation is anticipated to involve the issuance of new shares, with the São Paulo state government expected to retain a stake ranging from 15% to 30%, as opposed to the current 50.3%.

In late November, state deputies from the Brazilian state of São Paulo approved the report on the company's privatization project within the São Paulo Legislative Assembly (Alesp) committees. This approval, aligning with the government's presented timetable, is a positive development, heightening expectations of a swift completion of the privatization by 2023.

The recently approved report underwent minimal changes compared to the one initially presented by the São Paulo government in mid-October. One notable addition was a guarantee of stability for Sabesp employees for 18 months.

The next phase of Sabesp's privatization project involves voting in the Alesp plenary. Deputies are expected to discuss the text in the first week of December, with the possibility of further amendments by legislators.

Potential risks at this stage include the introduction of burdensome amendments, though sanitation contracts tend to be more binding across various municipalities. Factors such as the privatization timeline and penalties for delays in meeting universal sanitation project targets in São Paulo remain considerations.

Upon privatization, Sabesp will be relieved of the need to conduct tenders for all purchases, streamlining processes and reducing costs, thereby enhancing the company's efficiency and predictability.

According to the São Paulo Secretariat for the Environment and Infrastructure, privatization will impact user tariff reductions. Thirty percent of the capitalization proceeds will be allocated to lowering tariffs. Regarding the sustainability of fare reductions post-privatization, the secretariat highlighted that the state's profit from its stake, anticipated to be between 15% and 30%, will be utilized to sustain the fare reduction.

Sabesp's 3Q23 Financial Results

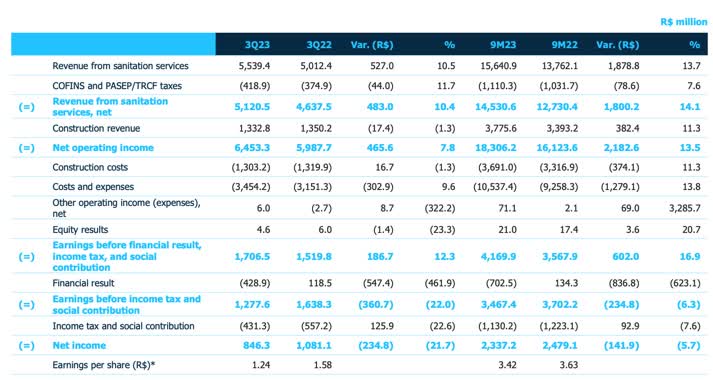

Despite Sabesp's Q3 financial results showing some weakness, there are positive indicators that offer a solid foundation. Sabesp reported strong operating performance, but the unique economic landscape hindered the year-over-year comparison.

Favorable monetary and exchange rate variations influence this comparison. Consequently, the financial result showed a negative value of R$428.9 million in the third quarter, significantly below the R$118.5 million recorded a year earlier. Nevertheless, from July to September, net operating revenue, including construction revenue, reached R$6.453 billion, marking a 7.8% annual increase.

{kind=link}

Notable figures include a 21.7% year-over-year decrease in Sabesp's net profit to R$846.3 million. On the positive side, adjusted EBITDA reached R$2.4 billion, reflecting a 13% increase from the previous year. Consequently, the adjusted EBITDA margin (excluding construction revenue) reached 47.1%, up from 46.1% in 2022, signaling initial improvements under the new management that assumed office at the beginning of the year.

Sabesp' IR

Factors contributing to this improvement include the 9.6% tariff readjustment implemented in May and a 3.5% increase in the invoice volume. Additionally, the voluntary severance program (VSP), with 1,862 employees signing up (approximately 16% of the company's workforce), enhanced Sabesp's margins in Q3.

How Far Can Sabesp Go With Privatization?

Companies operating in the water and wastewater sector, particularly those in regulated environments like Sabesp, have their rates and returns on investment determined by regulatory bodies. The EV/RAB ratio, denoting Enterprise Value to Regulated Asset Base, serves as a metric for investors to gauge the market's perception of the company's value relative to its regulated assets.

Since efficient companies often trade at least 1x their EV/RAB, a buoyant market perception about Sabesp's privatized operations could potentially drive this value even higher. Efficient distributors can trade at 2x EV/RAB in sectors like electricity.

With Sabesp shares surging nearly 30% since June, the company trades at an EV/RAB of 1.1x. In my assessment, this no longer reflects the worst-case scenario for the company, where it remains state-owned and undergoes no significant turnaround.

{kind=link}

In an optimistic scenario, the company's efficiency will likely improve as privatization progresses, fostering greater efficiency without substantial contractual constraints. This could result in lower tariffs, increased investments, and the stock potentially reaching close to 1.5x its EV/RAB. This optimistic projection could bring Sabesp stock to $18.75 per share, representing an upside of around 35%.

In a more cautious scenario, where privatization fails to drive efficiency improvements and current regulations persist, resulting in higher tariffs and unattractive returns on investment, the company might still trade at an EV/RAB of at least 1x. This would be approximately 10% above the current level.

However, in my perspective, this cautious scenario is less probable. The interests of the state of São Paulo, which is expected to retain a significant stake, appear to align well with efficiency and growth opportunities for the benefit of all shareholders, including the general population.

The Bottom Line

While Sabesp's recent Q3 results may not yet be labeled as excellent, they signify the company's positive trajectory. The report highlights robust annual EBITDA growth and significant advancements in its voluntary severance program (VSP).

As the privatization process continues, the primary concern for the current thesis revolves around the regulatory conditions under which the company will be privatized. The critical question is whether these conditions will foster the anticipated efficiency needed to reach its 2029 universal sanitation target.

In the most optimistic scenario, which aligns with the position of the Government of São Paulo and suggests a harmonious alignment of interests in the privatization process, I maintain a positive outlook. Sabesp currently trades at an EV/RAB of 1.1x, but it has the potential to reach 1.5x. This suggests a substantial upside potential in the short to medium term.

In a more pessimistic scenario, where Sabesp faces onerous clauses in the event of project delays under the current regulation, which lacks a focus on efficiency, and structural difficulties persist in the Brazilian sanitation sector, such as the absence of standardization, the company could be traded at an EV/RAB of 1x. This would imply a downside in the current share price. The extent of this downside is contingent on the severity of regulatory challenges and structural issues impacting the sanitation sector in Brazil.

For further details see:

Sabesp: Privatization Just Around The Corner, Q3 Results Still Provide Room For Upside