SBR - Sabine Royalty Trust Has Some Very Unusual Characteristics

2023-09-25 11:23:32 ET

Summary

- Sabine Royalty Trust has many operators associated with their interests unlike most energy trusts that only have one or two operators.

- Their current distribution yield is 6.8% based on their latest monthly distribution and latest unit prices.

- Because CAPEX numbers by the operators are not included in press releases, it is difficult to forecast future production results.

Sabine Royalty Trust ( SBR ) has a number of differences from other oil and natural gas royalty trusts, which makes it more difficult to analyze and to estimate a proper valuation. SBR has been helped by higher oil prices this year that partially offsets lower natural gas prices. I am estimating an average monthly distribution going forward that translates into a yield of approximately 7.5% based on the latest SBR price. Because of their business model and lack of disclosure, I rate SBR neutral/hold.

A Very Different Royalty Trust

Sabine Royalty Trust is different from most oil and gas trusts. Most energy trusts have just one or two actual operators that drill/produce oil and/or gas that is subject to the royalties. SBR, however, has many, many operators. This makes it more difficult to analyze their potential future results because you can't just look at the one producer to get a "feel" for what that producer is planning. I consider this a negative. Others, however, may consider having many different producers to be a positive because it means significant diversification. In Texas alone they have 4,194 interests and by scrolling down the list you see the operators from major ones such as Occidental Petroleum ( OXY ) to small "mom and pop" ones. For example, their interests in Panola County, Texas are where there has been significant increase in production from new horizontal wells and based on my research it seems that the actual operator is Amplify Energy ( AMPY ).

Acreage by Basin

sec.gov

A major problem with so many different operators is lack of information about current and planned CAPEX. When there are just one or two operators there is usually fairly detailed CAPEX information included in monthly distribution press releases. Unlike most trusts, such as Permian Basin Trust ( PBT ) that has such a high CAPEX allocated to them that they currently only have a token amount of monthly distributions, SBR itself does not directly pay for CAPEX. SBR investors are in the dark about CAPEX and the resulting potential (or lack of potential) production increases.

Another issue with having so many operators is that their monthly reports are not always accurate. Because the royalty checks are sent by mail some of the checks are received late, which distorts that month's numbers and the following months. Investors need to be aware of this potential issue when comparing monthly figures.

Lack of Complete Financial Numbers

SBR is also different from most other energy trusts regarding their financial reporting - it is almost nothing. Comparing the 2022 10-K annual reports of SBR and PBT we can see the difference.

Sabine Royalty Trust Annual Income Statement From 10-K

{kind=link}

sec.gov

Permian Basin Royalty Trust Annual Income Statement From 10-K

sec.gov

(PBT is a combination of two different properties)

To estimate the actual total production revenue for 2022 for SBR I used numbers reported in the discussion area because there are no actual financial statements that include total revenue in their 10-K. I multiplied the total 2022 natural gas production of 14,092,037 Mcf by the average natural gas price of $5.96 to get approximately $83.99 million and added that to the total oil production of 608,140 barrels multiplied by the average price of $90.41 to get approximately $54.98 million. The total is $138.07 million. The difference between this $138.07 million and $125.75 million royalty income is $12.32 million - implied operating expenses and taxes. I wish the trustee would give investors complete financials instead of the token amount shown in their filed reports.

SBR Valuation

When trying to place a value on an energy investment some use the estimated value of their developed reserves by estimating the present value of future forecasted net revenue discounted back to present value at 10% - PV-10. The PV-10 in the latest 10-K is $327 million, but the PV-10 in 2012 was estimated at $250 million. So, the estimated value of the developed reserves has gone up in ten years even after there has been a very large amount of revenue/production. I don't use PV-10 because it has too many problems, but some Seeking Alpha readers like to see it.

Sabine Royalty Trust is often priced in the market by a combination of two factors. The first is the yield based on monthly distributions, and the second is that it is a long-dated call option on natural gas and oil prices.

Pricing SBR based on yield is significantly impacted by current yields on alternative investments, such as 10-year U.S. treasury notes. The sharply rising interest rates over the past twenty months has had a negative impact on pricing SBR. Of course, the increased monthly distributions last year offset this downward pressure, but distributions have declined this year from last year.

Their TTM distributions total $6.90917, but that total includes distributions from late last year when natural gas prices were very high. The latest monthly distribution is $0.36430, which was based on a $1.89 average natural gas price and $74.58 oil price. This September 5 distribution declaration was based primarily on May's natural gas production and June's oil production. (This is another oddity compared to other energy trust who use the same month and are not delayed as much.) Using a very simple approach of multiplying the latest distribution by twelve months we get $4.37, which implies a yield of 6.81% based on the latest SBR price of $64.18.

Annual Distributions

2022 $8.654040

2021 $3.217520

2020 $2.396650

2019 $3.019790

2018 $3.349060

2017 $2.368370

2016 $1.93403

2015 $3.10520

2014 $4.09779

2013 $3.91645

2012 $3.70090

I estimate that an increase for the price of oil to $89 from $74.58 results in approximately a $0.05 distribution increase per month after deducting the average implied operating/tax/fees expenses. This is assuming natural gas remains at $1.89 and production remains the same. Based on my outlook for natural gas and oil prices, I would estimate an average monthly distribution of approximately $0.40 per month going forward. This estimate implies an annual distribution of $4.80 and a yield of approximately 7.5% based on the current SBR price of $64.18. Because there is no disclosure of current or future CAPEX and/or drilling plans by the operators one can't accurately estimate long-term future monthly distributions even if one could accurately forecast future energy prices.

Because I expect natural gas prices to trend lower on a seasonally adjusted basis, after already declining since my bearish price outlook mentioned in my Chesapeake Energy ( CHK ) article in early September, and that I expect only a modest increase in oil prices from their recent highs, the "call option" part of the value of a SBR unit is only very modest. This means that most of the value is, therefore, currently based on the distribution yield. Allowing for a modest amount of the current $64.18 SBR price to be effectively a call option on energy prices, the implied yield would increase from the forecasted 7.5% to about 8%, which is about 355 basis points above the 10-year UST yield or about 289 basis points above the 2-year UST yield. This spread difference is not significant enough, in my opinion, to make SBR attractive for investors because SBR is very risky.

Natural Gas and Oil Prices Outlook

Stronger oil prices have partially offset much weaker natural gas prices this year as can be seen by their impact on SBR's price in the two charts below.

Natural gas prices continue to decline in the futures market and in the various regional markets.

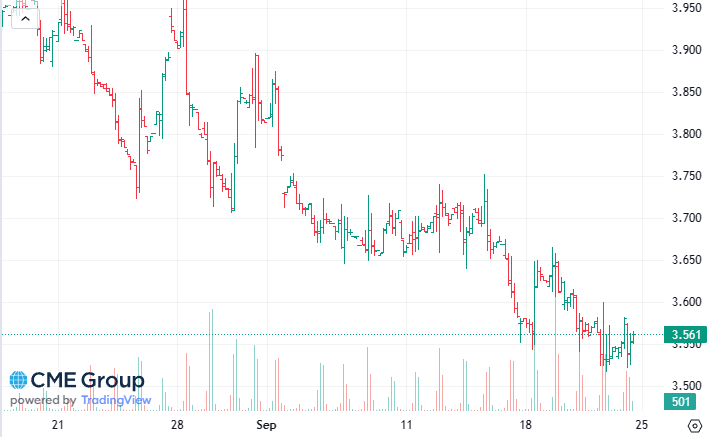

January 2024 Henry Hub Natural Gas Futures Prices

{kind=link}

www.cmegroup.com/markets/energy/natural-gas

Regional Natural Gas Spot Prices (9/22/2023)

www.eia.gov/todayinenergy/prices.php

(Percent changes are from the prior day)

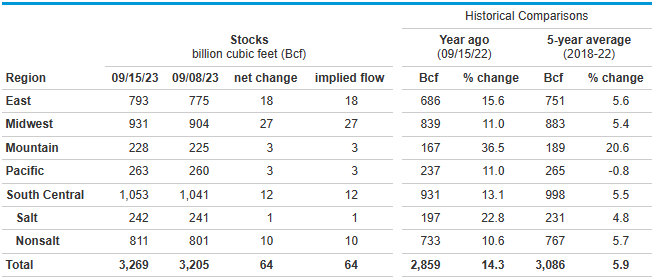

I think that natural gas prices may continue to trend lower on a seasonally adjusted basis because of the strong storage numbers as can be seen by the table below. Colder than normal temperatures this winter, of course, could change all that.

Weekly Natural Gas Storage Report

{kind=link}

ir.eia.gov/ngs

All last week there were many bullish reports on the price of oil going over $100. The $100 is a very nice media "shock value number", but in reality, it is only a little more than 10% above the current price. The price may pop up above $100 and then drop back down as the impact on a slower world economy impacts demand/prices for oil. The higher interest rates caused by the Fed are not having a negative impact as fast as I expected. The delay is caused partially, in my opinion, by the irrational increase in stock prices that is making consumers feel wealthier and more willing to spend. When the market drops and small businesses have an even harder time getting loans at attractive rates, the economy will head south for the winter. Oil prices will follow lower.

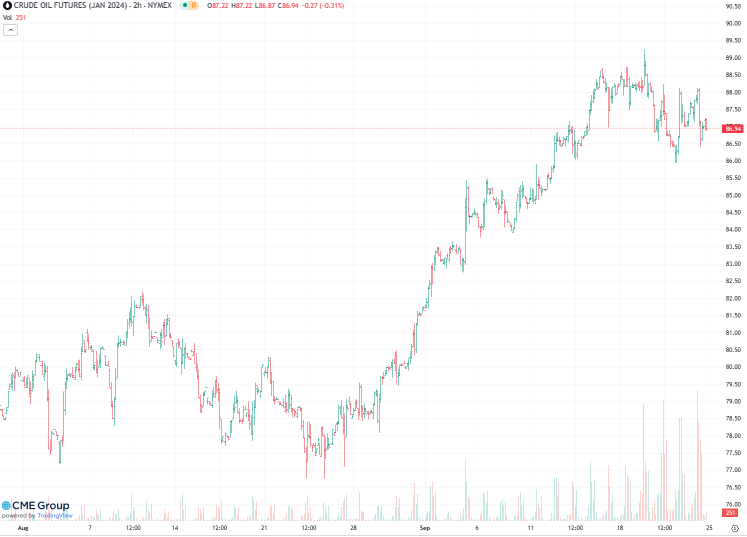

January 2024 Crude Oil Futures Prices

{kind=link}

www.cmegroup.com/markets/energy/crude-oil

Conclusion

I have always passed over Sabine Royalty Trust as a potential investment because they have so many producers associated with their interests that you are in the dark regarding current and expected CAPEX. You can't, therefore, get a feel for future production and future distributions. Planned CAPEX by producers might be very high or low - we don't know. They also do not report what I consider complete financial statements. In addition, because I am not bullish on long-term natural gas and oil prices, I'm avoiding buying most energy companies. The relatively high distribution yield may act as a cushion for further declines in SBR price, but I do not consider it a buy. I rate SBR neutral/hold.

For further details see:

Sabine Royalty Trust Has Some Very Unusual Characteristics