PEAK - Sabra Health Care: A 9% Yielding Healthcare REIT

2023-09-20 03:56:56 ET

Summary

- Sabra Health Care REIT has defied our expectations and stabilized its funds from operations over the last 9 months.

- The company has seen occupancy gains in senior housing-leased and behavioral health categories, leading to increased tenant EBITDARM coverage.

- We give you our outlook for this 9% yielder.

On our last coverage of Sabra Health Care REIT ( SBRA ) we were skeptical that the company would be able to stabilize its funds from operations (FFO) in the face of significant challenges. We expected the headwinds to win out and hence gave a very cautious outlook on the stock. Not every thesis goes according to plan and SBRA has certainly defied our expectations and, well, even gravity since then.

Seeking Alpha

We look at the recent results and see if the thesis needs to be revised.

Q2-2023

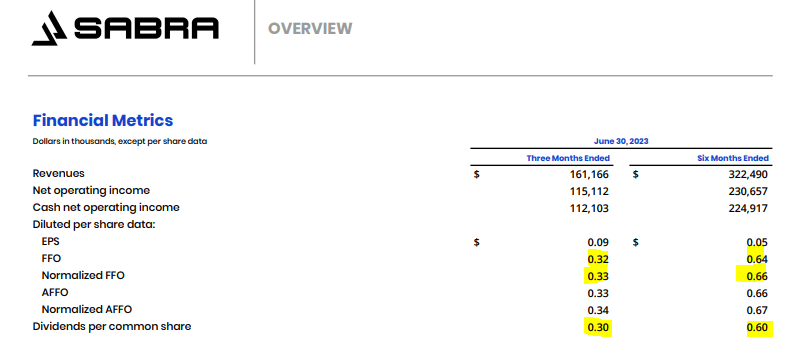

For both Q2-2023 and Q1-2023 the normalized FFO came in at 33 cents a share. This allowed a slim margin for the continued payment of the 30 cents of dividends a quarter.

{kind=link}

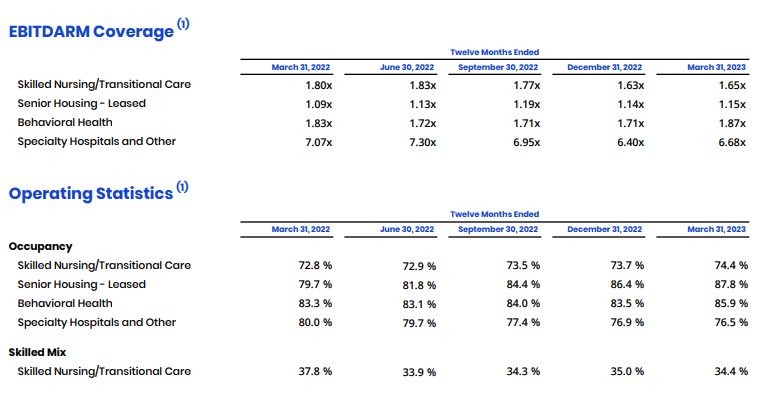

What was notable for the company was that the tenant EBITDARM (earnings before interest, taxes, depreciation, amortization and management fees) coverage increased in senior housing-leased and behavioral health categories. The former was particularly important as that segment operates on very low margins and very low EBITARM coverage levels. These small increases were the direct result of occupancy gains.

{kind=link}

The sector has struggled due to the high mortality wrought by COVID-19 on its primary population. Secondary factors like extremely high supply from builds that were started pre-COVID-19 have also played a role. But those pressures appear to be abating and occupancy gains are finally starting to come through. It was not all good news though. Skilled nursing has shown a very modest improvement off the trough in occupancy and EBITARM coverage has actually dropped over the last 12 months (though up quarter over quarter) despite that.

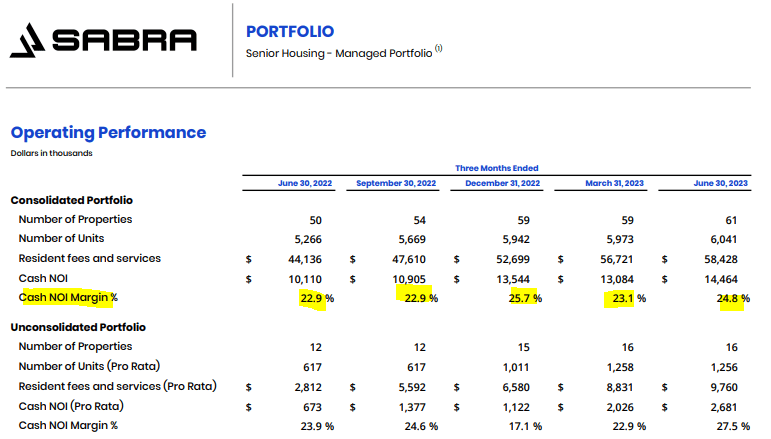

On its own managed portfolio (as opposed to the leased portfolio), SBRA showed steady improvements in cash net operating income (NOI) margins. This is one area that they faced a lot of stress in 2022 as high inflation for all supplies as well as wage pressures were the primary themes.

{kind=link}

Outlook

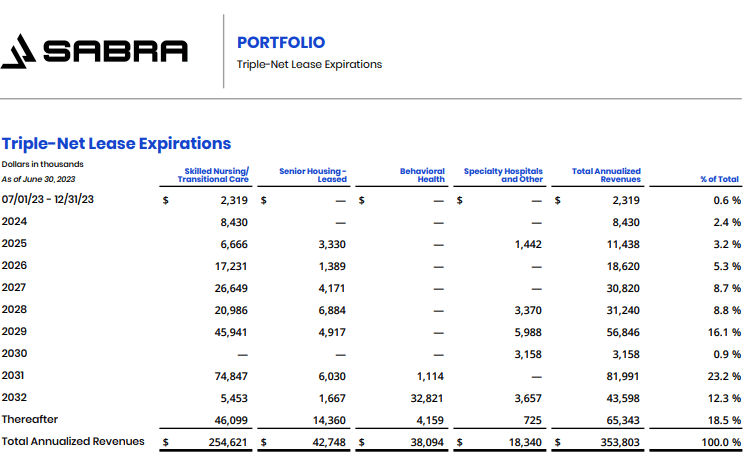

SBRA's key metrics are overall looking better and the stock has responded in kind. The REIT has very few leases expirations the next three years and that means that it will not have to go looking for tenants.

{kind=link}

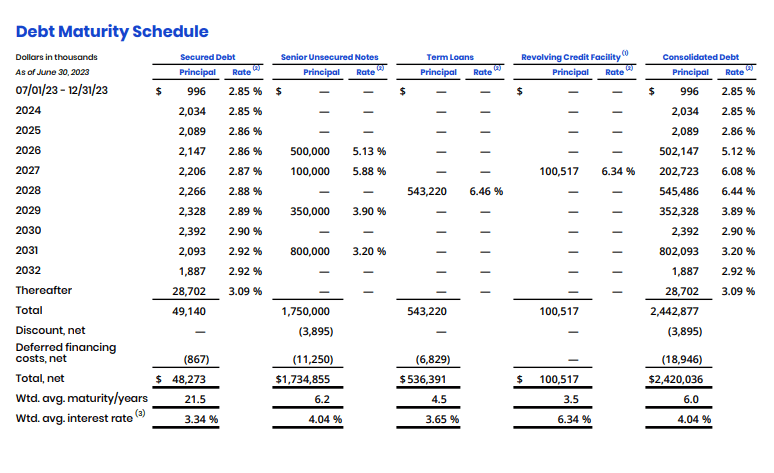

The demographic tailwind should also continue to lend an assist. This is in big contrast to some of the office REITs which have massive macro pressures from work from home trends, as well as large lease expirations . On the financing side, SBRA also does quite well. We have next to nothing in maturities for 2023, 2024 and 2025. 2026 has one big tranche at $500 million but even that is not massive in light of the total $2.4 billion of debt.

{kind=link}

Interest coverage and debt to EBITDA look quite good, and variable debt levels are manageable as well.

SBRA Q2-2023 Presentation

So those trends look good and SBRA does not have any insurmountable challenges lined up. On the other hand, most of its tenants still have extremely weak overall rent coverage. EBITARM is about the most generous metric there exists and is only one step away from "Earnings excluding every single cost". Even on that metric the tenants are not quite comfortable. Contrast that to medical office buildings even in second tier markets where Global Medical REIT Inc. ( GMRE ) operates. Rent coverage looks like breeze.

SBRA Q2-2023 Presentation

So this is a distressed asset class where periodically tenants end up taking water. Investors can visit our earlier articles for context to see how many of their large tenants have required some form of assistance or have had to be replaced. That in a nutshell is also why SBRA's FFO and cash flow per share have been doing a one-direction move over the last 5 years.

At present, the $1.36 of trailing 12 month FFO has come uncomfortably close to the dividend rate of $1.20. While unpredictable as to when it will occur, you can rest assured that the next tenant blow-up will take the FFO right in line with the dividend, or perhaps even below it.

Verdict

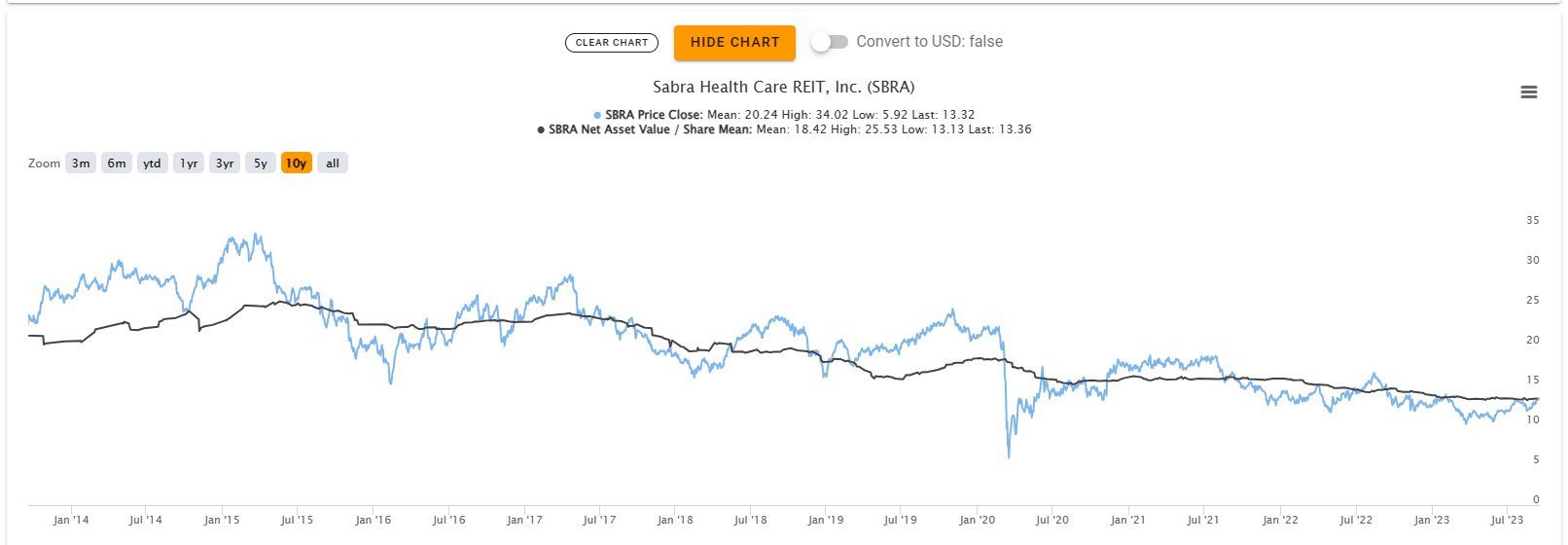

Over the last decade, SBRA has delivered a total return of 24.58%. This was less than breakeven if you went back a few months.

Granted that all REITs are beaten down at present and few show spectacular returns. But in its peer group also, SBRA has come in at the bottom of the barrel. The peer group in this case includes,

1) Ventas Inc. ( VTR )

2) Welltower Inc. ( WELL )

3) Omega Healthcare Investors Inc. ( OHI )

4) Healthpeak Properties Inc. ( PEAK ) and

5) National Healthcare Investors Inc. ( NHI ).

SBRA has had bigger tenant problems and has also issued a lot of stock at depressed prices, further lowering FFO per share.

This has also counteracted the natural flows which appreciate properties over time. Consensus NAV has trended lower over the last decade. That would be a stark contrast to property values which have increased at least 50% per square foot.

{kind=link}

We see the company as one of the weaker players in the space and don't think the current price offers a compelling entry point. Yes the large dividend yield looks tempting, but it is really about considering the total returns investors have got from the company. More importantly, the bulk of the price loss over this timeframe was due to FFO declines and not due to a multiple compression. We rate this a hold while giving it a 6 on our potential pain scale at this price.

{kind=link}

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Sabra Health Care: A 9% Yielding Healthcare REIT