SACH - Sachem Capital: Impressive Growth Undervalued Stock; Dividend Sustainability Questions Remain

2023-05-25 23:02:58 ET

Summary

- The company recently released its Q1 2023 results.

- The company has shown remarkable growth in recent years, and its stock is undervalued.

- Questions over its dividend sustainability remains, with a dividend cut likely.

Introduction

I have written about Sachem Capital ( SACH ) just once previously , in 2019. Back then, I came to the conclusion that the company wasn't for me and I put it to the back of my mind. However, SACH stock caught my attention recently when I noticed it was paying a high dividend yield. Moreover, the company released its Q1 2023 earnings last week. Hence, with these developments in mind, I aim to re-evaluate the stock to determine if my investment thesis has changed.

Business Model

Based in Connecticut, Sachem Capital is a real estate finance company that specializes in providing short-term loans secured by first mortgage liens on properties located predominantly in the Northeastern United States and Florida. The company's borrower profile is typically a real estate investor or developer using the funds for property acquisition, renovation and development. These loans are also known as "hard money loans" as they are secured by real estate assets. While historically concentrated in Connecticut, the company has expanded its activity to other states in recent years. As the company has expanded, it has also gradually increased the quantum of its loans. The company oversees the entire life cycle of the loan, from origination of the loan until it is fully paid off. Thus, while the majority of the company's revenue comes from the interest income on its loans, the company also receives revenue in the form of origination fees as well.

Q1 2023 Earnings

In the first quarter of 2023, the company reported a revenue of $14.7 million. This represents a substantial increase of 42.8% compared to the same period the previous year. Additionally, the company's net income grew by approximately 22.3% to $4.2 million, up from the $3.4 million in Q1 2022. However, it is worth noting that the company's earnings per share ((EPS)) remained the same at $0.10/share.

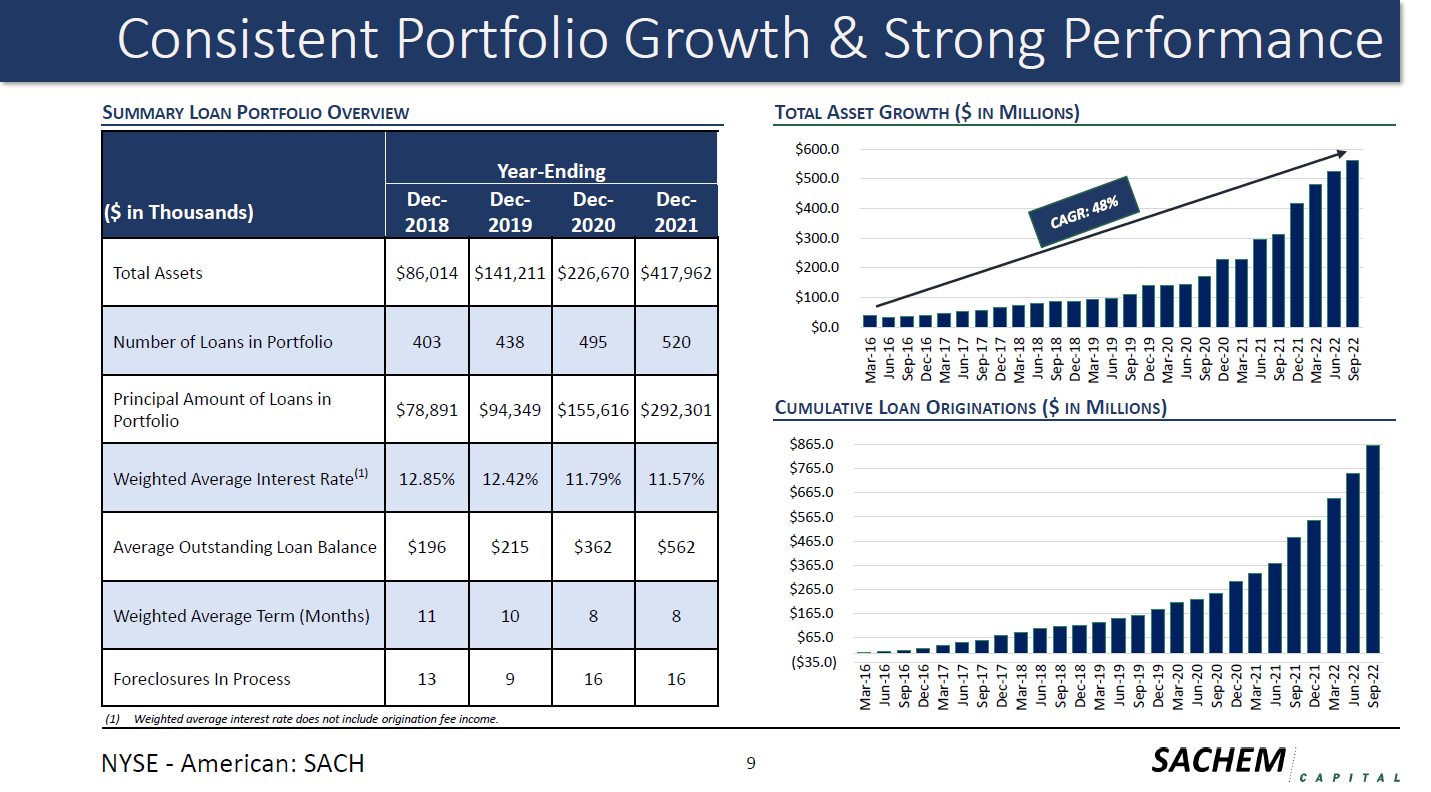

The company's mortgage loan portfolio has shown remarkable growth over the years, and this quarter was no exception. Starting from slightly under $79 million at the end of 2018, the loan portfolio has seen an impressive surge, reaching $460 million by the end of 2022. As at the end of the first quarter, the company's loan portfolio stands at $476 million, a 500% growth in slightly over 4 years (do note that the image below comes from the January 2023 investor presentation before the release of the FY 2022 results, which is why it only includes figures up till December 2021).

{kind=link}

Dividend History

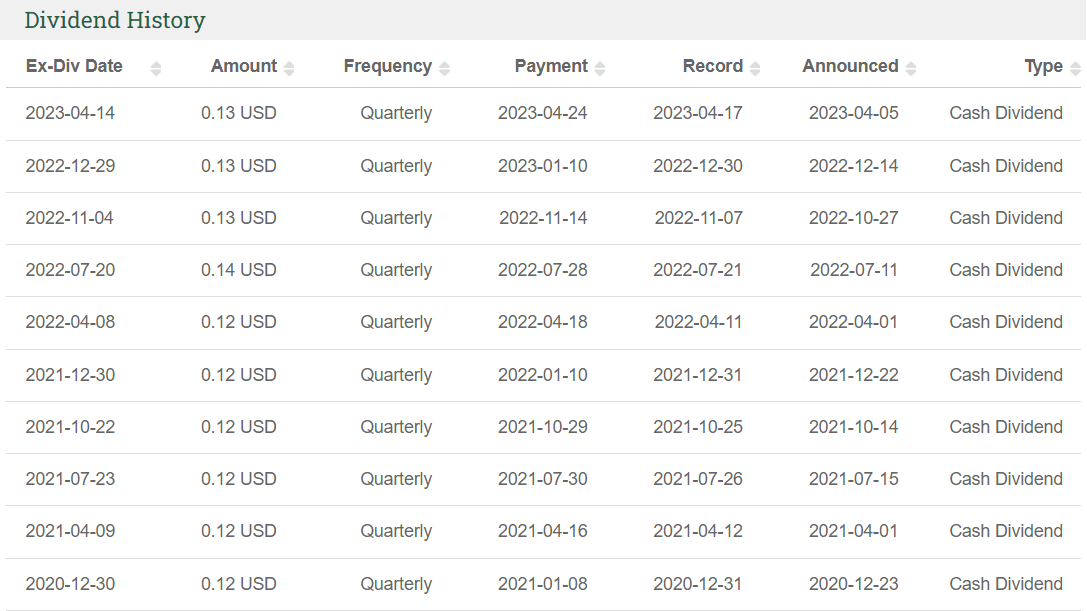

In April this year, the company paid a quarterly dividend of $0.13/share, marking its third consecutive quarter. It's worth noting that this represents an increase from the previous payout of $0.12/share, which had remained consistent since 2019. Some attentive readers may note that the company briefly raised its dividend to $0.14/share in July 2022, before ultimately settling at the $0.13/share in the next payout. While it may seem like a dividend cut (from $0.14/share to $0.13/share), I believe the adjustment to $0.13/share should be seen as a correction rather than a true dividend cut. In the broader context, the overall dividend has increased from $0.12/share to $0.13/share.

Based on the current share price of $3.04 and a quarterly dividend yield of $0.13/share, the company's forward dividend yield stands at a very impressive 17.11%. This high dividend yield naturally raises the question of its sustainability. A quick comparison to the company's EPS of $0.10/share shows that the dividend is not adequately covered; in fact, the payout ratio is at 130%. In fact, during the recent earnings call, the CEO acknowledged this concern, mentioning that there might be "a little bit of a slip" to the dividend, though he added that the company would defend the dividend "as long as we can". With how high the current dividend is, even a 50% reduction to $0.06/share would still see a very respectable dividend yield of $7.9%. Nevertheless, a dividend cut is never a good look for a REIT as it would indicate underlying issues within the company.

{kind=link}

Share Price & Valuation

In terms of valuation, the company appears to be significantly undervalued. According to Morningstar, the company is currently trading at a price-to-book (P/B) ratio of just 0.58, indicating a considerable discount to its intrinsic value. It's worth noting that historically, the company has traded at a premium to its book value. One caveat of course, is that its past performance is certainly no indicator of future performance and it is possible the company may not trade at a premium to book value in the future. Nevertheless, even assuming a P/B ratio of 1, the company's fair value can be estimated to be around $5.30, implying a potential upside of just over 70%.

{kind=link}

Risks

In the current challenging macroeconomic environment, brought on by rising interest rates and the recent bank failures, the company faces several challenges. The CEO acknowledged in a previous earnings call that 2023 would be a challenging year for the company, with originations in 2023 expected to be lower than in 2022. However, the company has taken proactive measures to strengthen its financial position and enhance liquidity. During the quarter, they secured a $45 million revolving line of credit, with the potential to expand it to $75 million, which provides valuable support for addressing short-term liquidity concerns. It is important to emphasize the short-term nature of the company's loans, as a significant portion is set to mature this year. Consequently, the company's ability to continually originate new loans becomes crucial to sustain its operations and is something to watch out for.

{kind=link}

Conclusion

When I first wrote about the company, one of my main concerns was whether the company would be able to sustain its growth as it expanded beyond Connecticut. A few years on, it is pleasing to note that although the majority of its portfolio is still in Connecticut, this proportion is gradually decreasing each year. Sachem Capital makes for a compelling growth story, having grown its mortgage portfolio by over 6 times, from $79 million at the end of 2018 to the current $476 million. Moreover, the company's substantial undervaluation presents an appealing opportunity for potential capital appreciation.

However, my key concern lies with the company's dividend. Based on current indicators, the dividend does not seem to be sustainable, and a dividend cut seems imminent, with the CEO having indicated as much. As a dividend investor, looking for sustainable dividends is a key factor in my investment decisions, leading me to remain cautious about the company, at least for the time being. Nevertheless, I will be keeping a close eye on the company's performance in the coming months and re-evaluate my decision again.

For further details see:

Sachem Capital: Impressive Growth, Undervalued Stock; Dividend Sustainability Questions Remain