SACH - Sachem Capital Is Struggling For Spreads On Limited Capital

2023-09-18 10:01:00 ET

Summary

- Sachem Capital grew too much too fast, and the money they raised to do it came at a high price.

- The company's loan book has grown significantly, but net income has lagged behind. Moreover, there has been a big spike in bad loans.

- Sachem's high debt levels and servicing costs, along with declining investor confidence, have put the company in a precarious financial position.

Sachem Capital (SACH) provides short-term financing solutions within the real estate market, mostly to "fix and flip" investors. Their primary focus is residential but have diversified into commercial in recent years. Operating largely in the northeast with some business activity in Florida, they were born out of the 2008 housing crisis. The loans they make are secured by first mortgage liens on the underlying properties.

My intent with this article is to address the unique dynamics at play within Sachem's market and how that is affecting their business. Bottom line up front: Sachem grew too much too fast, taking on a huge debt load in short order that allowed for a huge expansion in their loan book but with no commensurate increases to the bottom line. Interest payments, debt falling due, and other commitments are creating a liquidity crisis not easily solved. With no options to raise capital at attractive rates, Sachem needs to pause mortgage originations and let receivables create a cash balance that will satisfy their obligations.

Bread and Butter

Sachem makes money on origination fees and then interest payments on the loans they make. If those loans go bad they then re-possess the property and sell it off. Their underwriting standard is to only fund a project at 70% of its appraised value (loan to value ratio), and therefore are able to often make a small profit or at least break even on their loans that go bad.

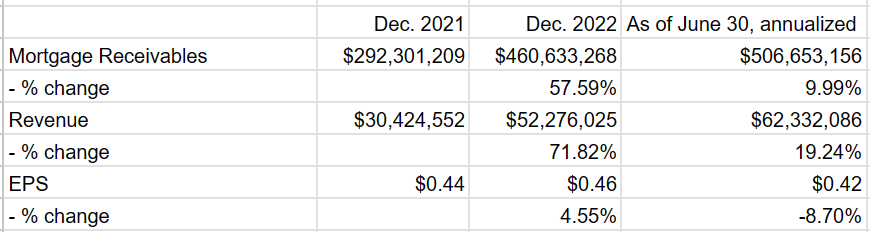

The primary influencers of how much money they make are the amounts loaned and the interest rate charged. They have been able to grow their loan book really well the past few years. Coupling that with rising interest rates means they are on track to smash their previous year's record revenue by 20%. The problem is that net income has lagged way behind:

{kind=link}

In spite of a loan book that is 20% bigger ($85 million) than at the same time last year and interest rates that are wider by several hundred basis points, EPS is LAGGING 2022 mid-year number, $0.21 currently compared to $0.22 last year.

How could this be? Part of it management explained in the most recent conference call :

So in terms of loan spreads, our cost of capital is between 8.5% and 9%. We are currently company-wide lending at a minimum of 13% and 2%, pushing higher, mostly 13% and 3%. The 3% is the origination, so our margins are very good. These are 1-year loans. We - this is not - so we were 12% and 2% when rates were much lower. We were borrowing at 6% with our unsecured notes. So our margins have been compressed....

In other words, they are getting squeezed on the interest expense side while not making up for it on the interest income side.

The other factor is that SACH has been issuing equity at an alarming rate and that at really terrible prices:

Share issuances continue at a high clip while the stock price languishes. Every new share issued at bad prices means not very much money raised, which is bad for a business that relies so heavily on outside capital, while reducing the proportional value of every share that existed before. It's bad on both ends. To make matters worse, beings that SACH is a REIT and has to pay out 90% of its earnings as dividends, each new share issued represents a new and perpetual drag on cash.

These factors have converged to make it so that the dividend payout is unsustainably high, with a most recently declared dividend of $0.13 per share with only $0.11 in earnings. That dividend was declared nearly a month after Q2 ended but 15 days before the earnings release. The company declared the dividend despite operations being unable to support it for the quarter.

They did explain in the conference call that the mismatch between net income and the dividend was "primarily related to our timing of certain revenues and originations." We will see. They followed up with:

As a REIT, we are required to pay out 90% of taxable income per year to our shareholders. And in this environment, the Board will continue to evaluate the distribution policy on a regular basis, balancing our performance with the importance of maintaining financial flexibility.

Bad Loans

A big concern is the amount of bad loans stacking up in their portfolio. As their loan book has grown generally, the amount of problem loans has increased disproportionately on a percentage basis. The table below has the numbers:

{kind=link}

The clear deterioration in underwriting is alarming. SACH does have a pretty good history of basically breaking even on foreclosed properties, but that is of little comfort. They aren't in business to break even, and they certainly aren't going to attract investors by breaking even. The time and money it takes to foreclose on a property is the biggest issue, as it diverts managerial attention away for the core business, which is a challenging one particularly in today's environment.

Weigh all this info against what they said in the 2022 10K as part of their 2023 business strategy:

We are funding larger loans than we have in the past that are secured by what we believe are higher-quality properties that are being developed by borrowers that we deem to be more stable and that have a history of successful real estate development. In addition, we believe the migration to these types of loans will offset any rate compression and help us maintain a low foreclosure rate.

Low foreclosure rate? For us as investors, we have to look at trends to try and extrapolate a future. The trend here is a huge red flag, especially given the peculiar macroeconomic conditions current.

Big Picture

In real estate, an ideal seller's market is defined as one where property values are high but interest rates are low. Those conditions mean the seller is going to get a good price for the property and finding a buyer won't be hard as the price of borrowing money is amenable.

A buyer's market is one in which property values are low and interest rates are low. Get a property for a good price and the price of borrowing money to buy the property is affordable.

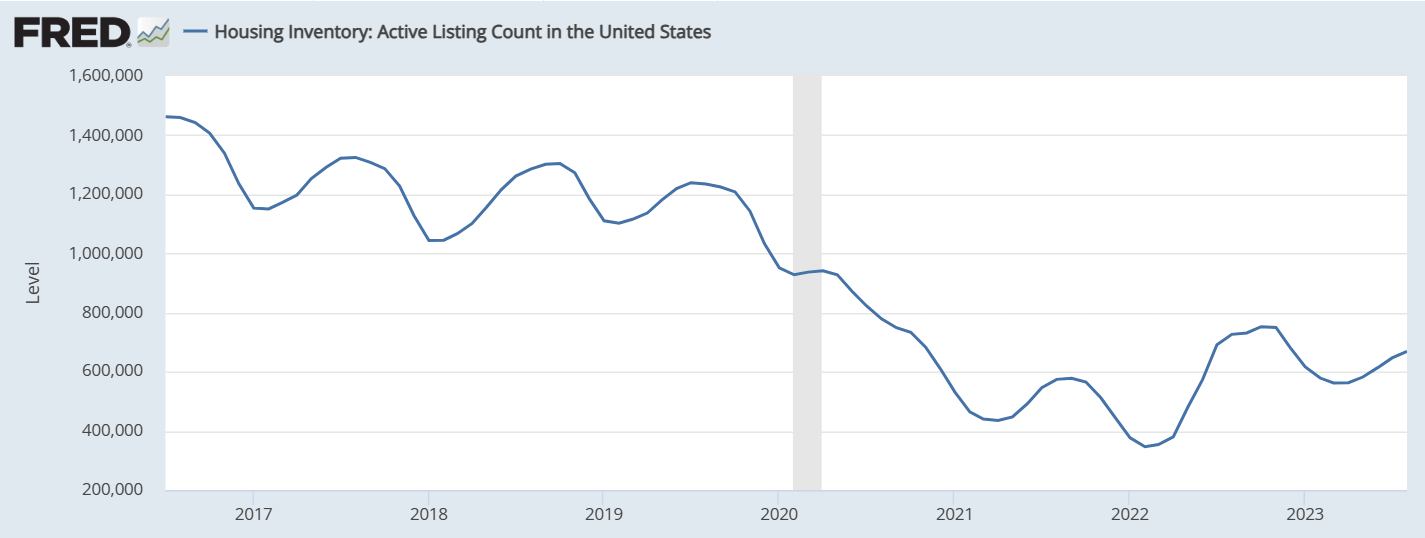

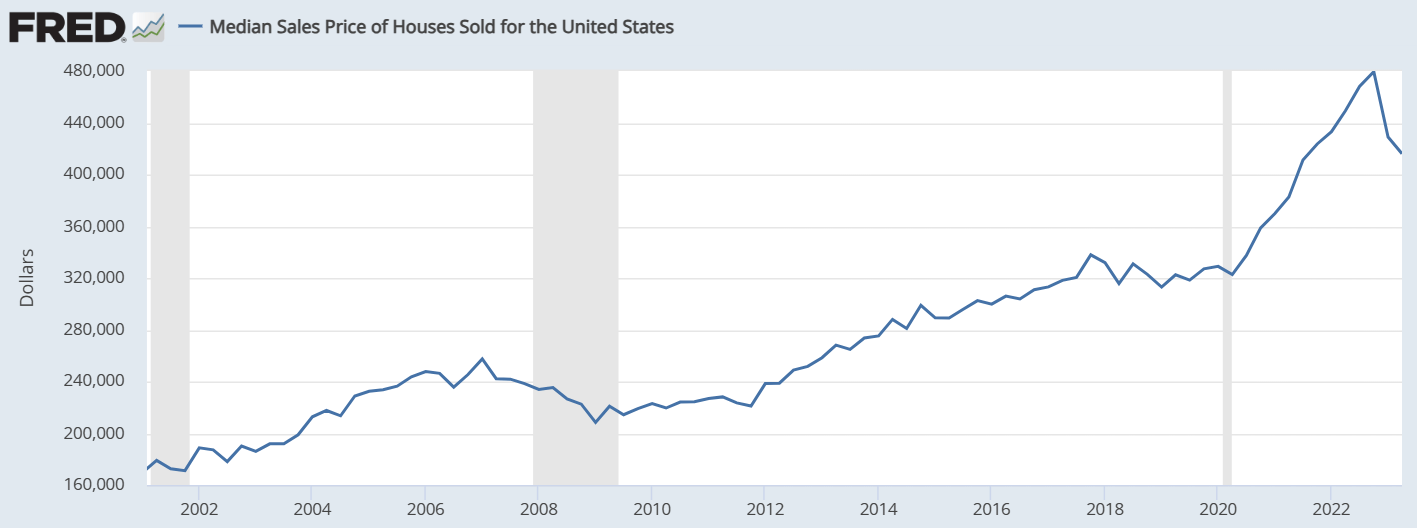

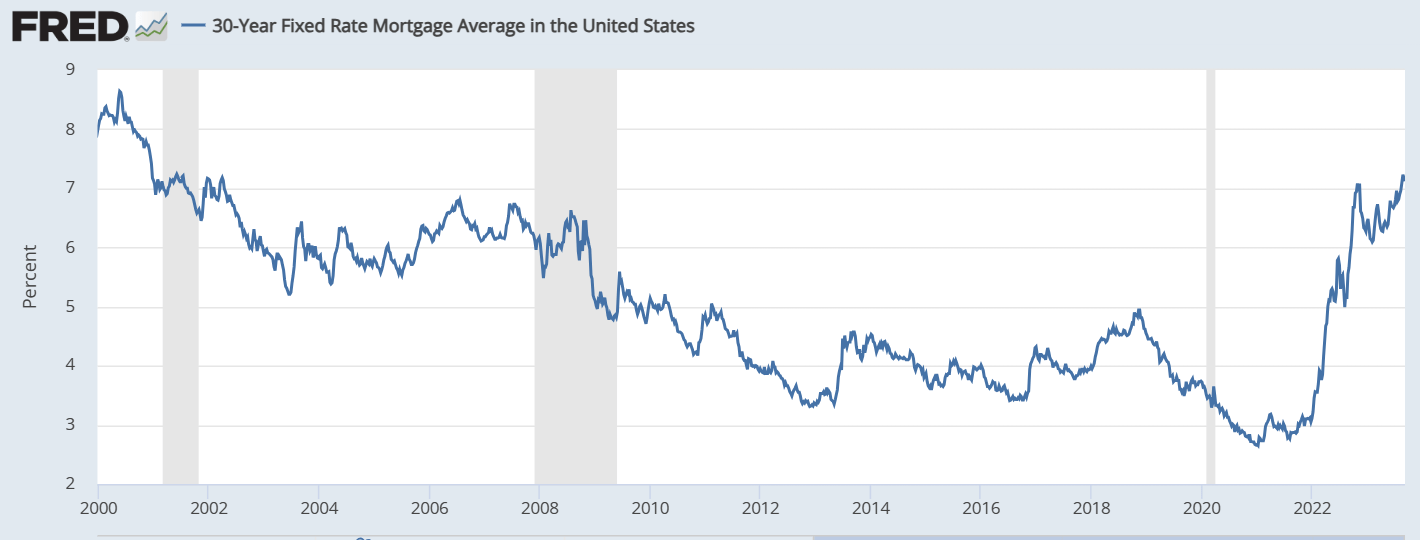

What are we in today? Well, property values are high due to inventory shortages, but interest rates are super high as the fed has been raising prevailing interest rates in an attempt to cool inflation. It's nobody's market. Sellers can't sell because a lot of buyers can't afford, but scarcity is keeping property values elevated as the few who can afford things are willing to pay a pretty penny for the little inventory that does hit the market. The following graphs paint the picture:

St. Louis FED St. Louis FED St. Louis FED

{kind=link}

{kind=link}

{kind=link}

Where does Sachem fit into all this? Well, as mentioned prior, the spread between their cost of capital and the interest rate they can charge on their loans in narrowing. Financial institutions are charging them higher interest rates to borrow but the market isn't allowing them to pass on commensurate increases to their borrowers.

It's also extremely interesting that the loan book at SACH has skyrocketed while the number of loans has decreased. They are funding loans at much higher values. The increased concentration risk needs to be underscored, especially in light of how their foreclosures have been trending. Any one loan that goes bad is going to have a larger impact on things. Here is another table that breaks down average loan value:

{kind=link}

Debt

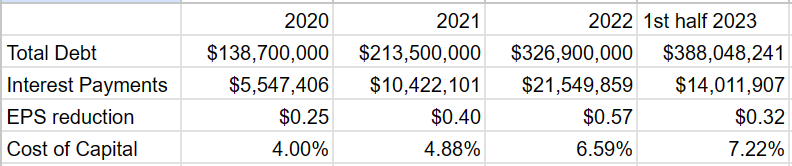

I briefly addressed the loan spread issue, how their large debt load and servicing that debt has made it so that their net income is struggling in spite of a much bigger loan book and commensurate increases in revenue. I think it worthwhile to get a bit more granular. The following chart shows how total debt and total interest payments, as dollars and on a per share basis, has grown over the past few years, alongside the imputed cost of capital:

{kind=link}

The cost of growth is getting ever higher.

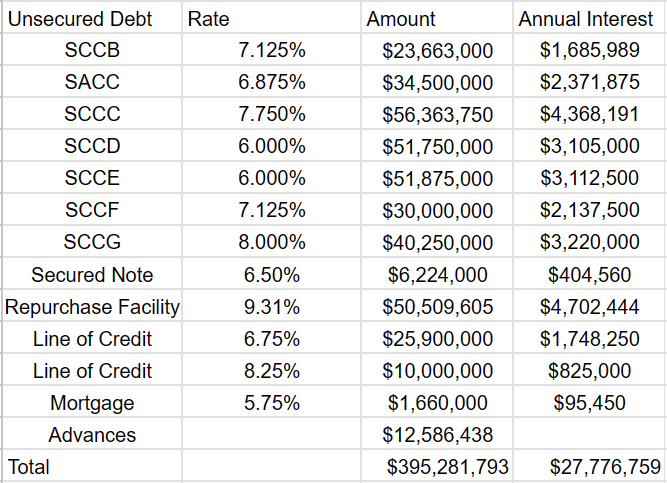

Here is a table of the total outstanding indebtedness:

{kind=link}

Here are the most interesting things to draw attention to:

1) The "advances" on the last line are "Advances from borrowers" as shown on the liability section of the balance sheet. What I find fascinating is that this item is only mentioned four other times in the 10K, and those mentions are only in the bits where they put into prose what is already shown on the balance sheet and cash flow statement. There is ZERO explanation of who they are borrowing these funds from, at what rate they are borrowing, and how long they have to pay things off. Nor do they explain what they are using these borrowings for. Generally speaking, advances from borrowers differs from loans in that they are typically short-term in nature and are used to meet working capital requirements. The outstanding balance of this line item is enough to warrant more information, but none is given.

2) The "repurchase facility" has some unique characteristics that are worth mentioning. First, it carries the highest interest rate among all their sources of capital in spite of outstanding amounts being secured by certain mortgage loans. Which brings up the second point: the collateral pledged backing up the $50.5 million outstanding balance are 26 mortgage loans that have an unpaid principal balance of $82.9 million. SACHEM is clearly shouldering all the risk here. Interestingly the 10K says this about this expensive source of capital:

We believe the Churchill Facility gives us the ability to raise capital as needed at a relatively low rate.

SACH can continue to draw on this facility up to $200 million.

3) The mortgage listed is for the corporate buildings SACH uses. What is interesting here is that the initial mortgage had pretty attractive terms, 3.75% interest rate with only interest due and payable for the first 12 months. After that, principal and interest amortized based on a 20-year schedule with all unpaid amounts due 2037. That agreement was made in 2021. But then, for reasons that seem inexplicable to me, the company refinanced the mortgage in February of 2023, which refinancing grew the loan from $1.4 million to $1.66 million and had a new interest rate of 5.75%, with principal and interest payments starting immediately. What's really peculiar is that SACH had $62 million of cash in the middle of 2021. They had $44 million in investment securities. Why would they take out a mortgage on corporate properties for such a relatively tiny amount when they could easily fund it with cash on hand? They started 2023 with $23 million in cash. Why would they refinance the mortgage to WORSE terms?

All told, their debt servicing is costing them $0.61 worth of EPS annually.

At the bottom of the capital stack is their Series A Preferred stock, of which 1,928,000 shares have been issued and are outstanding. At a rate of 7.75% annually, these shares come with an annual price tag of $3.7 million, another $0.08 worth of EPS. Interestingly, in the first six months of 2023 the company issued 24,603 shares of preferred stock but were only able to do so at a 16.6% discount to the liquidation preference.

So what is the point of all this? The point is that, for a variety of reasons, individuals and institutions have less confidence in SACH to successfully navigate the future such that they are demanding a higher reward for the risk they take in loaning money to SACH. Higher interest rates, harsher terms, discounts to liquidation preference, says it all.

It is worth noting too that SACH doesn't have an awful lot of wiggle room as it relates to their debt covenants. The agreement on one of their lines of credit will be considered breached if SACH asset coverage ratio falls below 150%. It is at 158% as of the last reporting period. Their unsecured notes as well as the repurchase facility have covenants that seriously impair Sachem's ability to do certain things if the 150% threshold is breached. Most importantly, they are forbidden from raising any more debt under that scenario. The dollars in between their current 158% and the 150% limit is only $20 million.

So what should SACH do? I think they should pump on the breaks in a considerable way as it relates to new loan originations. They have $229,763,962 receivables due in the rest of 2023 and prior, $97.1 million of which is distressed (due but unpaid), for $132,663,962 net that is healthy. They have $58 million in unsecured notes falling due in 2024 and the $12.5 million in advances from borrowers are short-term in nature and likely due within the next twelve months. It should be noted too that the 2024 notes can be re-paid at any time without penalty. They should stamp out the "advances from borrowers" and the 2024 notes as soon as possible, even if that means foregoing some loans. A strong case could be made too for them paying off the repurchase facility. They should most certainly NOT take on new debt to pay off the old. The $132 million coming at them for the rest of this year is more than enough to take care of all their near-term obligations PLUS the repurchase facility (the one with the highest interest rate), with $11 million left-over. Doing this would save them almost $8 million on interest expense in 2024, adding $0.17 in EPS.

But there is one more variable at play, one which cements the case for not originating any more loans for a while. They have $112 million worth of "unfunded commitments" to borrowers, a line item that is peculiarly absent from the balance sheet. Whereas most of their loans they fund in full at closing, this is money that is to be given incrementally as the borrower asks for it and meet certain conditions as construction and renovations progress. These amounts are contractually obligated and are all due within one year. Between these unfunded commitments, their unsecured notes due in 2024, interest payments, all in context of relatively low cash balances, it is my opinion that Sachem needs to NOT recycles mortgage receivables back into new loans. That cash has other, more important places to go.

The alternative is for them to continue to plow down the path of raising capital at increasingly unattractive terms so that they can pay off old debt, meet their unfunded commitment obligations, and underwrite more loans that are on a clear trend of having a worse profile. Their spread is contracting, and their foreclosures/nonaccruals are growing. Why continue to chase business under these conditions? The best thing they can do for the business is halt any new originations and start stacking cash so that they can satisfy all these financial demands.

Conclusion

Sachem's story is a tale as old as time that has turned into the song that never ends. They chased too much growth too quickly, growth at any cost. I feel this pattern is especially true in REIT-dom where, borrowing money is a necessity in order to grow since 90% of taxable income must be paid in dividends. It's easy to get caught in the loop of borrow money, spend that money, raise more capital to pay off the initial borrowings and try to pursue new business, and on and on and on. But that cycle can only ever perpetuate in a way that is accretive to the business and the shareholders if the capital raises are always on attractive terms relative to the return earned. It's about maintaining a spread. But Sachem hasn't done that. They have expanded their loan book by tens of millions of dollars in short order yet somehow managed to lose a penny worth of EPS over the comparable period. Now they are running into liquidity issues. Their debt ratios are outside of generally accepted limits, with a debt/EBITDA ratio of almost 8 (high is bad) and an interest coverage ratio of only 1.8 (low is bad), whereas a healthy number for the former is usually between 4 and 6 and the latter ought to be over 3. They simply CAN NOT pursue new business opportunities AND meet their contractual obligations. The money just isn't there. They can either seek a bunch more money on terrible terms (borrow at high interest rates or issue tons of shares at terrible prices), which I feel will only kick the can down the road, or they can stop originating new loans so as to build a cash balance that will allow them to pay off debt, pay interest, and meet their unfunded commitments. The latter choice is the best choice, but will obviously be terrible news to the market. If management announces a cessation of new loan originations the stock price is going to crater in a huge way. But that will be a huge buying opportunity because it means that the business has a chance to stay afloat and even get to a healthy place. If we get news of more borrowings, then that will be a signal to sell short. We will see.

For further details see:

Sachem Capital Is Struggling For Spreads On Limited Capital