SFSHF - Safestore: Strongly Positioned And Poised For Growth

2024-01-22 02:14:36 ET

Summary

- Safestore is benefiting from growing market demand and its strong brand in the self-storage industry.

- The company has a pipeline of new developments that will expand its property portfolio by 18%.

- The annual results showed weaker financial performance, including a small increase in dividends and an increase in net debt.

European self-storage operator Safestore ( SFSHF ) has a prime position in its home U.K. market and is expanding in several European countries. It is set to benefit from growing market demand and a strong brand combined with its deep operating experience.

I last covered the company last June, with my "buy" piece . Since then, the shares have fallen 7%. I maintain my buy rating but am paying close attention to how the business develops as several features of its latest results perturbed me.

Ongoing Demand Growth Looks Set

The long-term outlook for Safestore is driven by several factors in my view.

I expect demand to grow as European self-storage markets continue to be weakly developed compared to the U.S. While they may never reach U.S. levels, I think they could support far more space. Drivers like the high cost of homes in the U.K. (either bought or rented) continue to make the prospect of storing goods outside the home more attractive.

That applies to all operators, but Safestore can also benefit from its own ongoing expansion. The company continues to open new sites both in the U.K. and Continental Europe.

Company final results announcement

{kind=link}

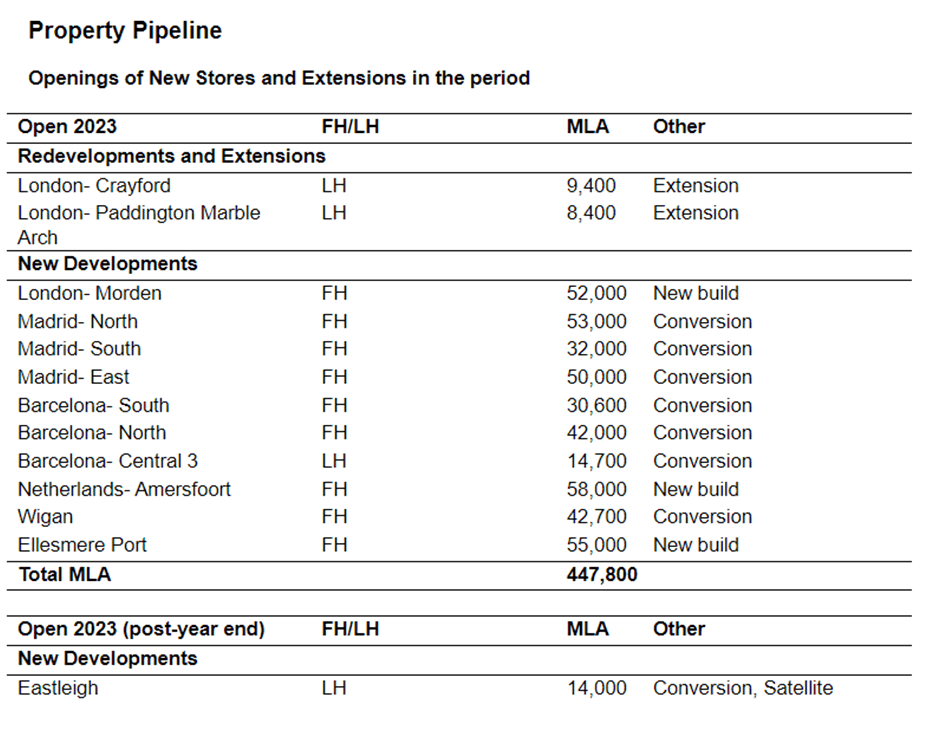

The pipeline is pipeline of c. 1.5 million square feet, which would be equivalent to around 18% of Safestore's existing property portfolio. Of those 30 new developments, around a third are in the U.K., with most of the rest in Paris and the Netherlands.

Results show Ongoing Growth but Less Impressive Financial Performance

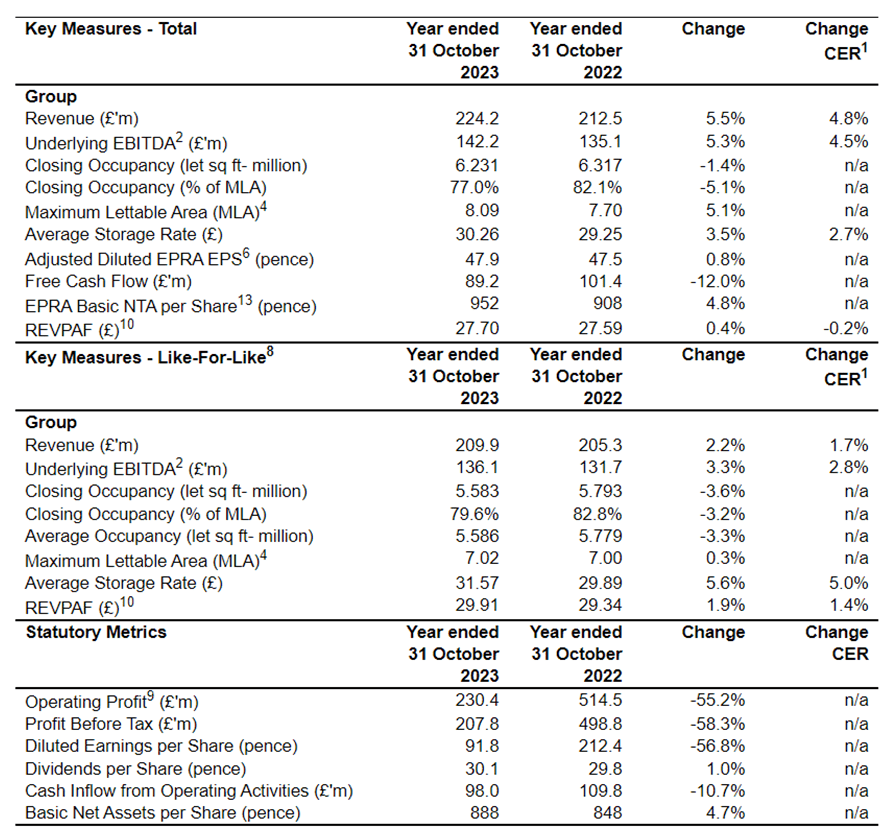

The company issued its full-year results this week and they were weaker than I would have hoped compared to recent years, although the company had signalled its commercial progress during the course of the year so they were not entirely a surprise. On the day the shares closed down 8%, suggesting the market did not like what it heard.

Company final results announcement (footnotes omitted)

{kind=link}

While revenue grew, that largely reflects adding footage to the estate. Closing occupancy was down and rental rates grew sharply, but revenues still fell. In the company's core U.K. market, closing occupancy rates fell from last year. I see that as alarming, even though the fall was modest. Closing occupancy rates were 78%, which is not terrible. But as the company continues to grow its estate at speed, I think it needs a more compelling commercial strategy to boost occupancy (Spain was disastrous, more than halving to a closing occupancy rate beneath 40%, but as it is a small part of the business that is less important, though very alarming).

Dividend Growth has Effectively Stalled

The big disappointment for me in the annual results - and I think it is one that affects the investment case negatively - was the size of the dividend increase, which grew just 1% year on year to 30.1p per share.

Yes, it is an increase but it is a dramatic step down. Safestore has long been a solid dividend raiser and the past couple of years saw big jumps.

Chart calculated and compiled by author using data from company annual reports and announcements

{kind=link}

Perhaps this is the inevitable follow-up to those big jumps. It may be financially prudent. After all, free net cash flow after investing costs was -£35m. Dividends added £66m of costs onto that and free cash flows were still negative overall but a £101m drawdown of borrowings in the financing costs section of cash flows largely balanced things out. In terms of coverage and sustainability, though, that is not a good omen.

One of the drivers for Safestore's strong share performance over the past five years has been its dividend growth rates. With that era seemingly now at an end, I think it could hurt investor enthusiasm and therefore to some extent the business case.

The company reiterated that this year's dividend increase was "in line with our progressive policy" With that policy still in place, we can expect more dividend increases in future. But the rise felt like bare compliance with such a policy, which I do not think bodes well for future especially if cash flows are negative.

Net Debt is Increasing

That brings us neatly to the topic of net debt (including lease liabilities).

It increased 16%. Note that that is mostly (90%) bank loans not lease liabilities. Digging into net debt excluding lease liabilities (albeit they are ultimately a real form of debt), here is the pattern. Debt has been growing, clearly.

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| 2023 |

| Bank loans (£m) |

| -369.9 |

| -413 |

| -454.5 |

| -484.7 |

| -623.8 |

| -725.8 |

| Cash at hand (£m) |

| 10.5 |

| 33.2 |

| 19.6 |

| 43.2 |

| 20.9 |

| 16.9 |

| Net debt exc. Lease liabilities (£m) |

| -359.4 |

| -379.8 |

| -434.9 |

| -441.5 |

| -644.7 |

| -742.7 |

Chart calculated and compiled by author using data from company annual reports and announcements

That makes sense in the context of the company's storage estate expansion. But I am not that impressed by the continual growth in debt at a time of higher interest rates when the company's overall financial performance is somewhat lacklustre.

Some Risks

Although I remain bullish on Safestore, there are risks. I see the barriers to entry for self-storage as fairly low and local operators with a warehouse can set up pretty easily. That poses a risk to pricing in the industry.

Falling occupancy rates also suggest there may be a mismatch between demand and supply in the U.K. self-storage market. Ongoing estate growth by Safestore and rivals could exacerbate that.

The debt also looks like a growing risk to me. It needs to be serviced and repaid at some point, potentially hurting future earnings.

Valuation Looks Attractive

The company is now selling for less than basic net assets per share.

I think its strong brand, established business, and commercial know-how mean it is cheap at the current price and maintains my buy rating.

By my calculation, the current price/FFO ratio is around 8. For a growing, established self-storage operator, I think that is attractive. It is less than half that at U.S. peer Public Storage ( PSA ), for example.

| net income (£m) |

| 204.4 |

| depreciation (£m) |

| 1.3 |

| amortisation (£m) |

| 1.3 |

| capital gains on asset sales (£m) |

| 0 |

| FFO |

| 201.8 |

| market cap (£bn) |

| 1.67 |

| price/FFO |

| 8.3 |

Table calculated and compiled by author using data from company annual reports and Seeking Alpha

However, I will be looking out for any further signs of commercial weakness over the coming several years that may affect that, particularly letting rates and net debt.

For further details see:

Safestore: Strongly Positioned And Poised For Growth