SAFRY - Safran: A Massive Aerospace Buy

2023-08-30 10:08:00 ET

Summary

- Safran stock has gained over 70% since June 2022, outperforming the stock markets.

- The company's H1 results show strong growth in revenues and adjusted recurring income.

- Safran upgraded its 2023 outlook and is considered a good long-term investment with potential upside.

In June 2022, I marked Safran ( SAFRF ) stock a buy, and since then, shares gained more than 70%, easily outperforming the market. In this report, I am revisiting Safran stock to discuss its second quarter results and the company’s valuation.

Time To Grow For Safran

{kind=link}

Looking at the narrow body capacity, it is observed that the market is recovered compared to pre-pandemic levels. It should be kept in mind that 2019 was impacted by the grounding of the Boeing 737 MAX, which was a pressure on the narrow body capacity that year but for assessing the recovery from the pandemic, 2019 is an adequate comp.

Looking at the regional progress of the cycle recovery, China and North America are seeing higher CFM engine cycles compared to 2019. China is running 2% higher down from 5% higher in Q1 while North America is seeing 16% higher cycles up from 10% in Q1. Europe is more or less stable at 95% recovery while the Asia Pacific region excluding China is 89% recovered in H1 2023 up from 80% in Q1 2023. So, we do see that the cycle recovery has been strong but is not uniform from geographic perspective.

The number of engine cycles tells us how the travel recovery is pacing, but it also tells us something about service demand because a running engine indicates an airplane that is in operation and an operational airplane needs services and parts.

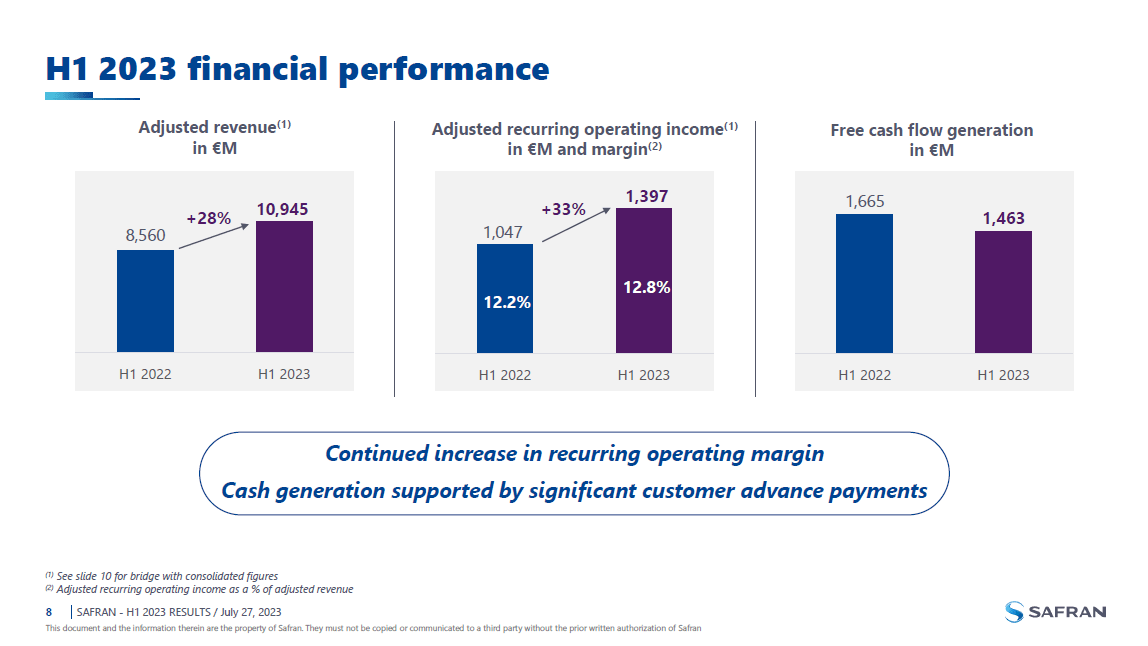

Safran H1 2023 Revenues Show Strong Growth

{kind=link}

Safran revenues grew by 28% positively impacted by a €136 million currency tailwind. Organic growth stood strong at nearly 25.9% while adjusted recurring income grew by 33% indicating a 12.8% margin compared to 12.2% last year.

{kind=link}

Aerospace propulsion revenues were up by 35.9%, driven by a 69% increase in LEAP engine deliveries which reached 785 units in H1 and was up 14% compared to Q1. High Trust Engine deliveries were down 8 units or 9% while Helicopter engine sales grew 21 and M88 engine deliveries for the Dassault Rafale saw unit delivery growth of 55%.

Increasing demand for CFM56 spare parts added to the growth. Overall, the aerospace propulsion business saw 58% growth in original equipment revenues and 23% growth in services. Overall, we are also seeing that OEM sales are taking a bigger share of the pie, namely 42% compared to 36% a year ago showing that OEM sales growth is outpacing even the growth in the Services revenues. Recurring operating income rose 45% indicating a margin improvement 17.3% to 18.5%.

{kind=link}

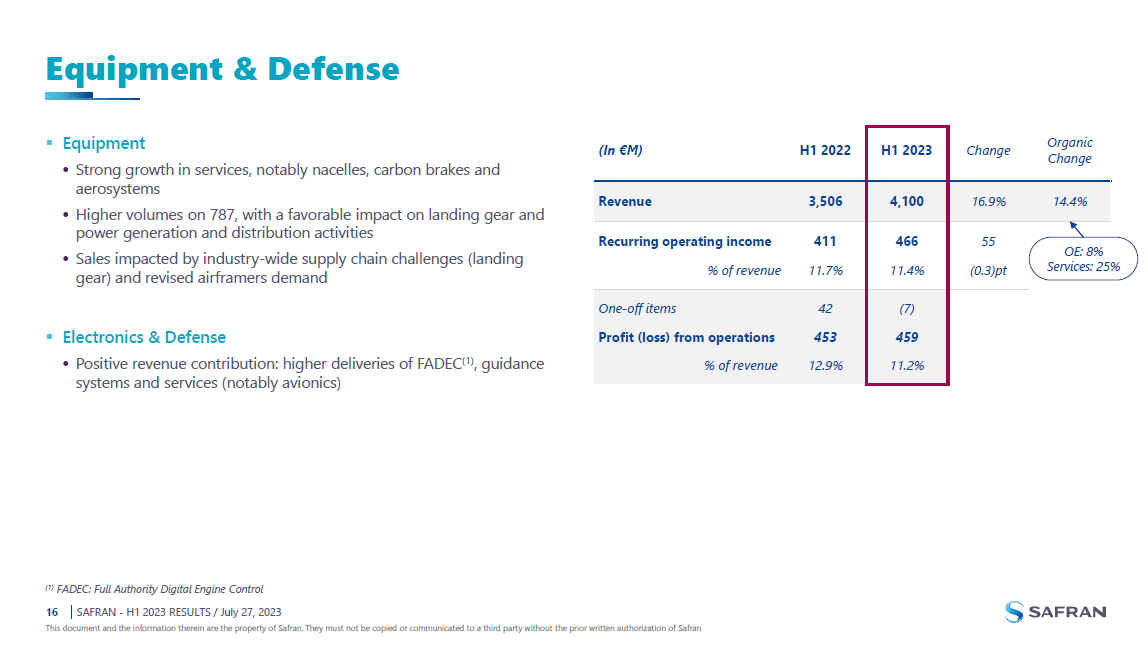

Equipment & Defense sales increased 16.9% with recurring income of €466 million indicating a small reduction in margins. Overall, the performance is relatively stable on the margins but supply chain challenges are impacting the performance in the segment. Early last year, the engines were continuously pointed at as the bottle neck for raising OEM output. However, it seems that the supply chain issues are now more prominently felt in other areas such as landing gears.

{kind=link}

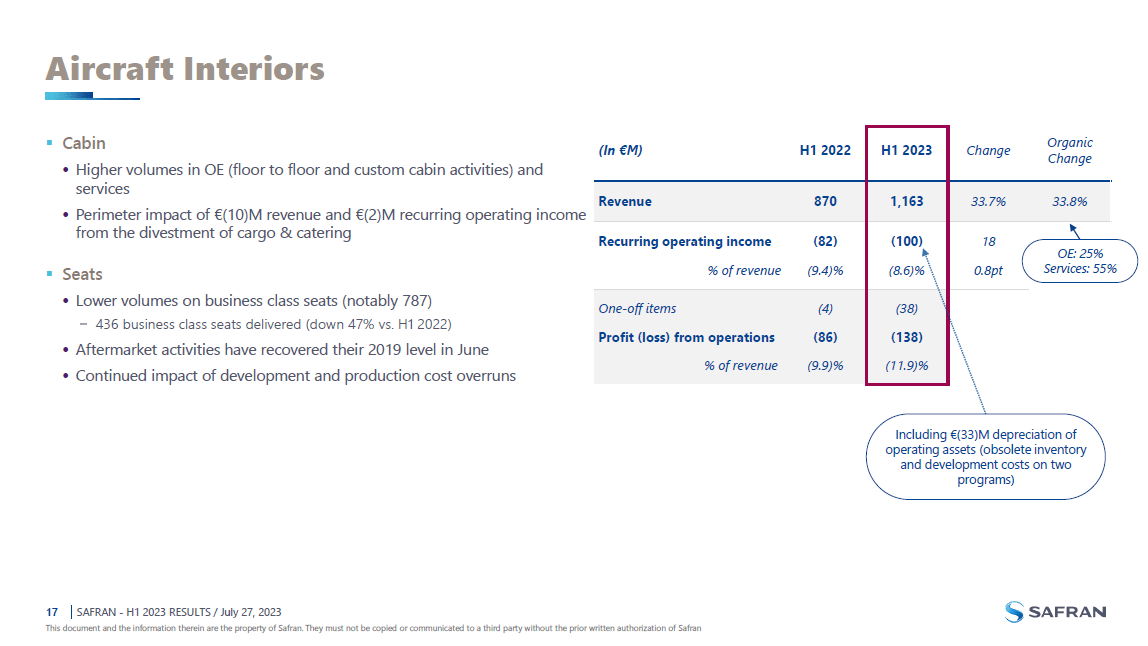

In 2018, Safran absorbed aircraft interior specialist Zodiac and while the acquisition provides better scale and depth to the aircraft interior business and fits within the consolidation trend in the aerospace supply chain, it has not necessarily been a lucky combination due to external factors. The segment saw 34% growth in revenues but it barely translated into the bottom line with a 0.8 points improvement in margins.

{kind=link}

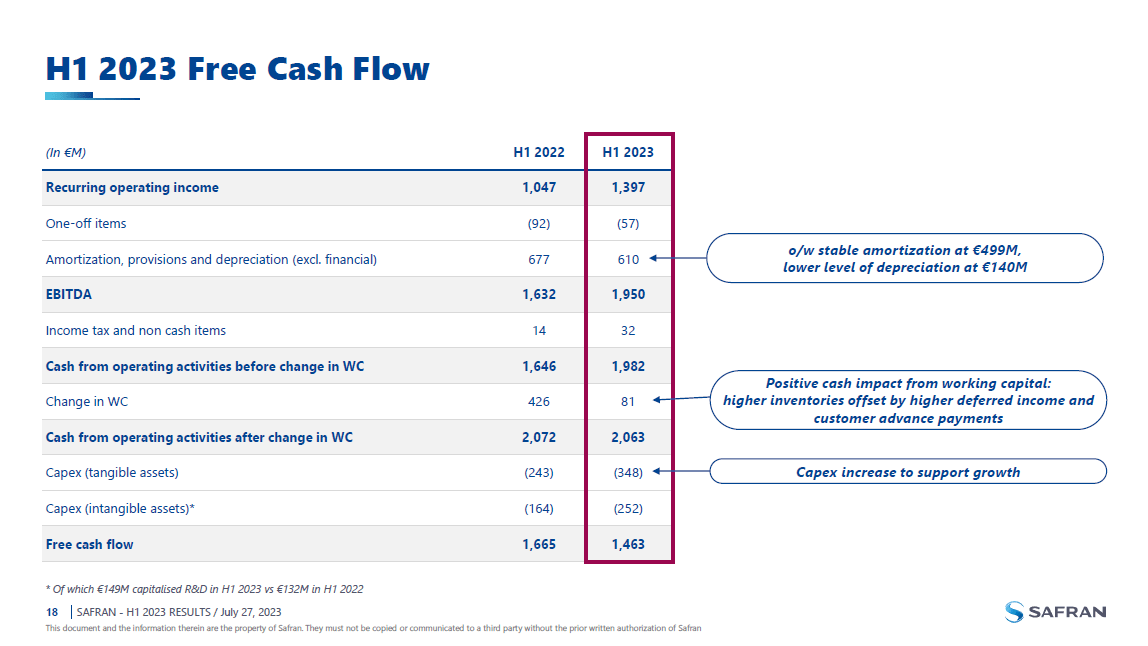

While revenues and profits grew for Safran, free cash flow declined from €1.665 billion to €1.463 billion. This €202 million decline in free cash flow can be explained by stable operating income after working capital changes while Safran invested €193 million more into the business to support future growth. So, 95% of the free cash flow decline was due to increased CapEx and the remainder was due to a reduction in operating cash flow.

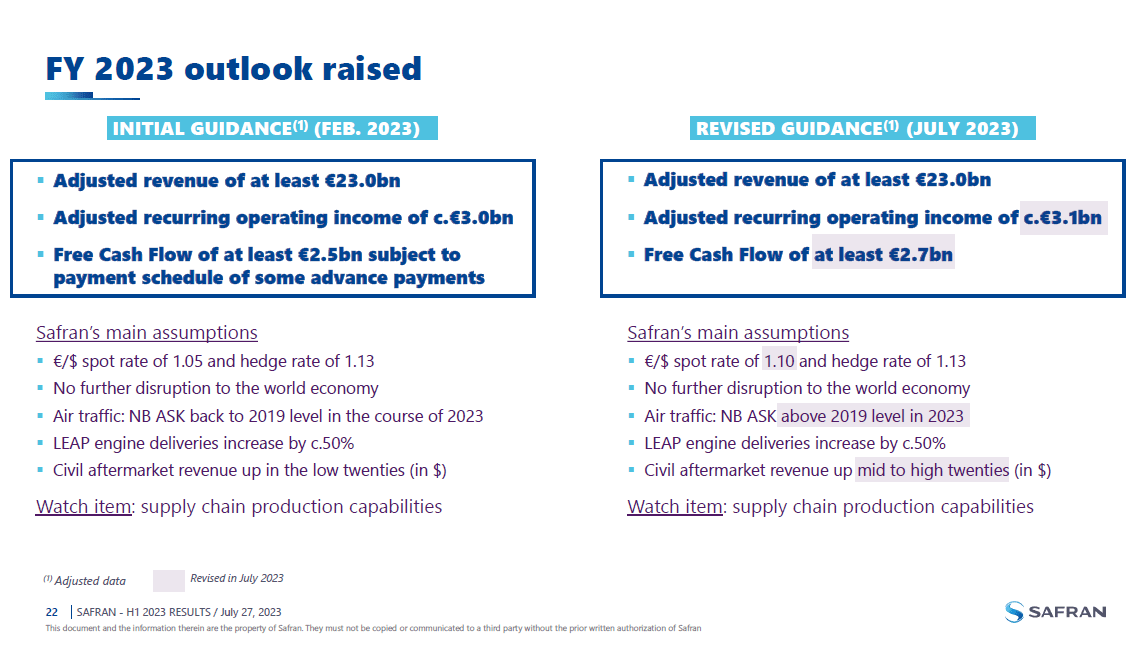

Safran Updates 2023 Outlook

{kind=link}

Safran has revised its guidance that it issued in February this year. Adjusted sales guide was kept constant, but the company expects €200 million higher free cash flow and €100 million higher operating income with civil aftermarket revenues guided higher and narrow body capacity being above 2019 levels. So, what we are seeing is that with a stronger recovery in narrow body capacity or better said growth compared to pre-pandemic, Safran has adjusted its revenue guide for civil after market and that is exactly what I pointed out at the start of the report when reviewing the engine cycle growth.

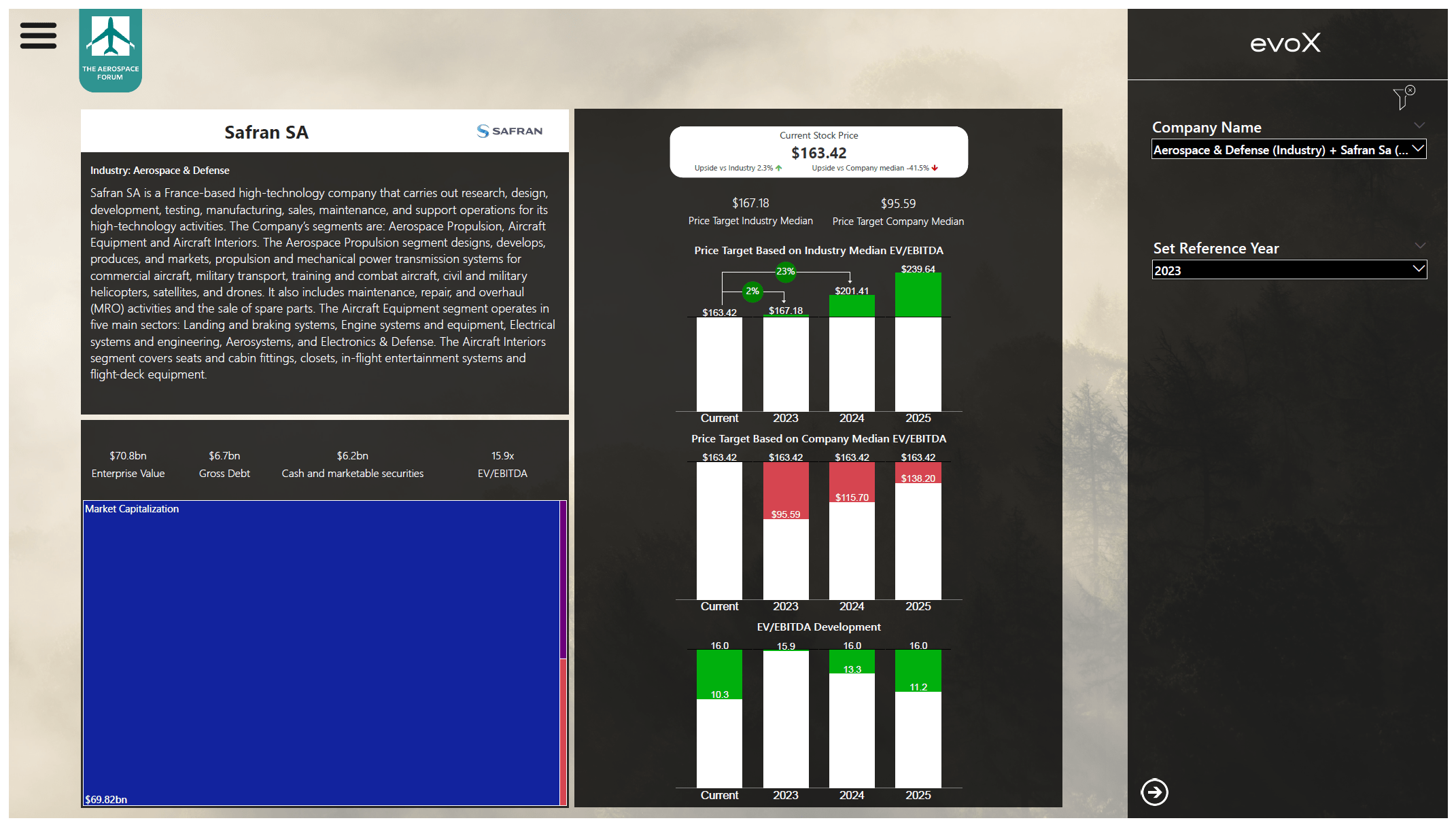

Is Safran Stock A Good Buy?

Safran stock price valuation using evoX Financial Analytics

{kind=link}

After surging 70% since my last coverage, the big question is whether Safran stock has any upside left. I wouldn’t want to value Safran against its median EV/EBITDA of 9x. Not because that is the situation that does not provide upside, but because it does not make market sense to have the industry valued at 16x EV/EBITDA and a company with low net debt at a 9x multiple. Even more so, given how big this company is with exposure to the key propulsion system on the Boeing 737 MAX and Airbus A320neo.

Filling in the numbers from the balance sheet as well as the projections for the coming years, Safran stock is fairly valued for this year’s earnings. So, if you would buy now, you buy the stock at a very small discount. However, I believe that this is a stock you should be interested in to buy and hold for the longer-term. With the long-term holding in mind, we should also evaluate the price targets in the future and for 2024 there is 23% upside with roughly a similar upside for the subsequent year. With that in mind, I would mark shares a buy.

Conclusion: Safran Remains an Aerospace Stock to Buy

Safran continues to track well on its CFM LEAP delivery ramp up and the CFM56 spare business provides a boost to the business. The company does have the OEM and after-market sales channels which I am a big fan of as well as commercial aerospace and defense exposure. So, in terms of diversification it has the end-market and channel diversification that I like. The aircraft interior business is not so much performing in line with expectations but the overall business is performing well and while there are supply chain challenges that are sticky, I think the financial performance has been good and Safran is investing for the future for growth. If it had no indications that the supply chain health would further improve, it would not put in those capital expenditures.

For this year, I believe that the stock is more or less fairly valued. So any buying at this stage means you are not buying at a discount. Generally, I would buy the stock on any price weakness, but also with the upside in 2024 and 2025 in mind, I do consider Safran to be a highly attractive stock to capitalize on increased demand for airplanes and defense equipment without having to choose between Boeing or Airbus.

For further details see:

Safran: A Massive Aerospace Buy