SAFRY - Safran Benefits If Fleets Stay 20% Smaller In Commercial Aviation

2023-04-05 16:14:02 ET

Summary

- Fleets have shrunk by about 20% across the board among commercial carriers, and this means that new deliveries fall into the background for Safran's CFM and Leap engines.

- Deliveries, also in the military segment for the Rafale, are negative margin contributors, so a skew in the mix towards aftermarket is a good thing.

- Recession may limit discretionary investment by carriers and keep Safran's cash economics in a better state, while travel still makes a recovery from COVID-19.

- More normalised activity in the interiors segment will turn it from being a negative margin contributor, already evidenced in Q4 2022.

Safran (SAFRF) is one of the two major players in manufacturing jet and helicopter engines in Europe, and one of the four major players in the world. Their engines are commercially very successful, and we think that recessionary conditions, while on balance are still bad for the company, allow for downside protection due to the nature of Safran's economics and the dynamics in its installed base. Moreover, 2021 was still damaged by COVID-19, and regardless of discretionary income, more will be spent on travel now compared to 2021. We predict resilience by Safran on a fundamental level, but do not bite at the current valuation and would require major drawdowns in price before we'd be interested.

Q4 Safran

Let's start with the obvious: a still depressed environment in the second half of 2022 was a problem for the aircraft interiors segment which depends on higher orders for aircraft. Those had picked up in some markets, but China was a drag, and generally the outlook is improving for this sort of OEM revenue. Already in Q4 2022 the segment , which had been a negative profit contributor for the whole of 2022, has gone to breakeven and has returned about 8% back to operating income on a run-rate basis , so as of the Q4 2022.

The story of this year is that there's been a slowdown in deliveries of new units of engines. On the military side, the issue wasn't demand, it was supply side issues. On the commercial side it's been a demand issue as well, specifically with China being a weak market for new orders. Narrowbody has been the more prosperous market, with not that many new orders for jumbo jets for obvious reasons - carriers are still concerned about the situation in the markets, perhaps less now from COVID-19 and more so from a potential recession.

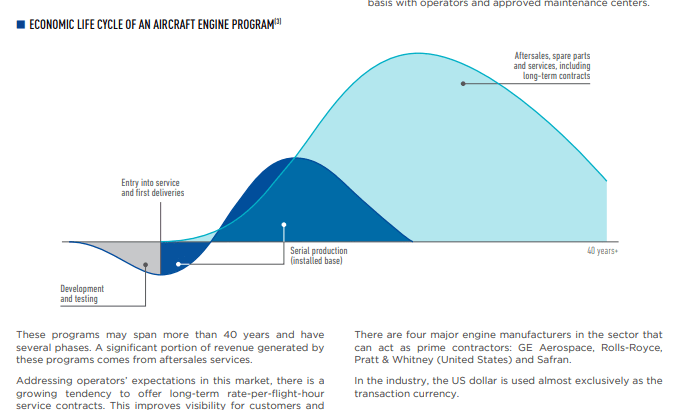

When new engines are smaller in deliveries, and there's more aftermarket activity in the revenue mix on already installed platforms, margins markedly improve.

{kind=link}

Operating income growth exceeded revenue growth on those mix effects (24% growth and 33% for the FY).

While the Rafale has been a very successful platform lately, and supply chain bottlenecks loosening will mean more M88 deliveries, there is a case for continued positive dynamics in the commercial aviation segment.

Fleets have fallen across the board by 20% as older planes have been scrapped. A 20% smaller fleet might be about the right size for the current market environment. While COVID-19 isn't such a demand problem anymore, fuel prices are high and a rational supply among carriers is necessary in light of that. Moreover, recession will mean a cap on the amount of discretionary travel, and this should limit the extent of airport activity and travel recovery to pre-COVID levels. There shouldn't be too much latent demand for Safran's commercial engines, which are getting long in the tooth anyway and maturing into the best part of their aftermarket phase.

Ultimately, new deliveries are a good thing because they broaden the installed base, but it's good to know that the business can be positioned for a higher return on restored flight hours from a depressed 2021 due to COVID-19. Also some amount of new deliveries should come from a reopened China, where we are getting a lot of revenge travel going on right now.

Bottom Line

The FCF conversion is phenomenal, more than 100% FCF on EBIT. The current economics of Safran are great, and we expect a relative amount of resilience to continue thanks to the passing hysteria over COVID-19.

The problem is the multiple. The company is too expensive at over a 10x EV/EBITDA multiple. We aren't interested in anything at this multiple in current markets given the many alternatives that we hold in our model portfolio.

For further details see:

Safran Benefits If Fleets Stay 20% Smaller In Commercial Aviation