SAFRY - Safran: Phenomenal Delivery Numbers Set Up For Cash Cow Economics

2023-06-15 11:10:32 ET

Summary

- Safran got saved by the fact that meaningful aftermarket activities, which are outsized margin contributors, step up in the mix in an aviation downturn.

- Now we are getting a major delivery rebound that is accelerating deliveries in the key segment of propulsion, driven by the key new engine product of LEAP.

- In aircraft interiors, we should see a scaling into profitability, and while deliveries are lower margin in propulsion, the sheer growth should create incremental income.

- The massive growth in engine sales across the board sets up for cash cow economics from aftermarket revenues.

- However, all this is priced in at 13x EV/EBITDA.

Safran ( OTCPK:SAFRY ) is the leading European producer of engines. They also produce aircraft interiors and other equipment related to aviation. Between biannual reports, they disclose revenue figures, which are the latest data we have on Safran, and all signs point to meaningful profit growth as well as a basis for long-term cash generation as their industrial business model scales. Commercial aviation developments were as we expected . While there is a lot of profit growth coming, there is the issue that this superior business' qualities are already priced in the multiple.

Q1 2023 Note

There is no explicit income reporting here , but we can make some assumptions based on segment revenue developments which are reported.

{kind=link}

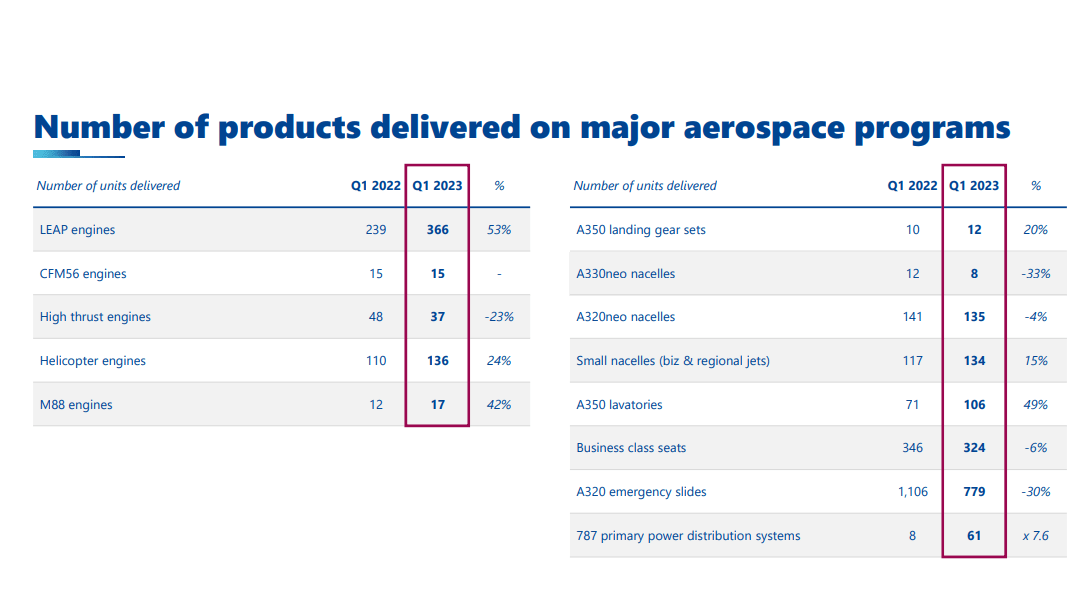

Starting with engines, note that major programmes like the M88, the heli engines and the new LEAP engine all saw major growth in deliveries. Last quarter there was less of this, and Safran was skating off aftermarket much more. LEAP was growing last quarter, but not anything else, including the M88, which is used for the Rafales.

Outside of propulsion, equipment connected to commercial aviation new builds, like lavatories and landing gear, all saw substantial growth. This quarter has demonstrated a movement away from more servicing activities to more action that builds the installed base.

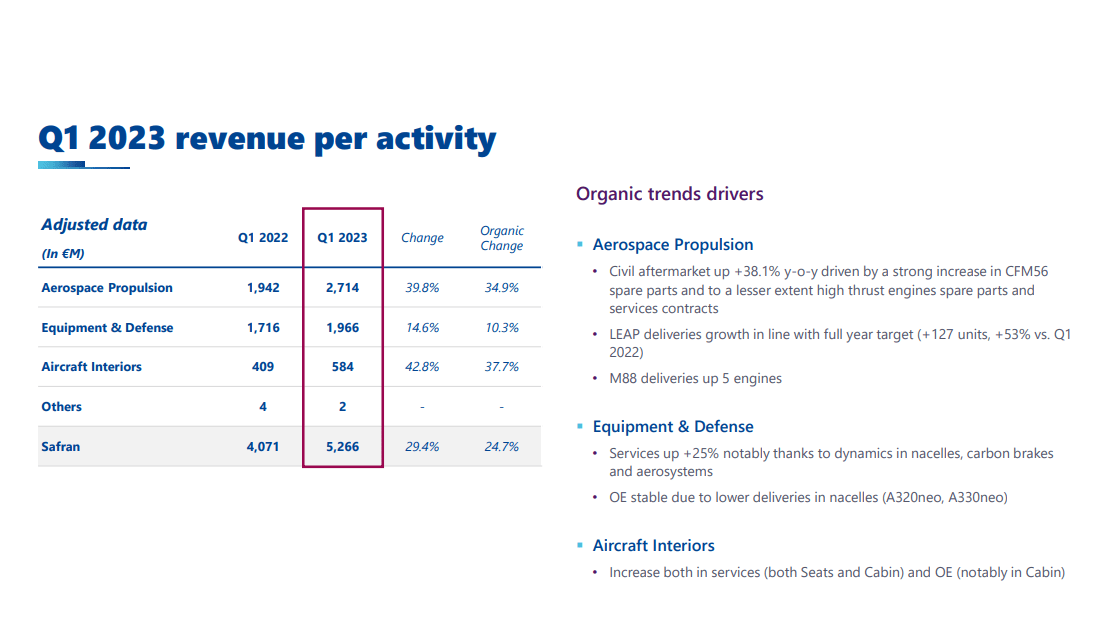

Revenue is up 25% organically YoY for Q1 2023 being driven by aircraft interiors and propulsion, which in turn are both being driven by a strong rebound in commercial aviation new building.

Aircraft interiors was an unprofitable segment last year due to the depression in aviation, but there was quite a meaningful gain in operating margin as it scaled 34% from 2021 to 2022. Continued scaling this year with growth accelerating in this quarter could erase losses and add about a 3-4% bump to the operating profit line.

{kind=link}

While delivery activity in propulsion is going to be less profitable than aftermarket, the almost 40% growth in revenue is bound to drive profit growth even if mix effects are not in the bottom line's favour. What's more is that an acceleration in the growth of their new engine programme just grows the installed base of engines that Safran will be able to service for multiple decades, as it has done with the older CFM platform. Since aftermarket revenues are always going to offer a higher contribution than straight deliveries, which are close to being unprofitable, growing the installed base by such a substantial degree will set Safran up for another wave of cash cow economics as the LEAP platform begins to age a little.

Bottom Line

Reopening in APAC after recent COVID-19 lockdowns, particularly in China, is spurring a lot of revenge travel and carriers are investing again. Across geographies, fleets have gotten older and smaller, and a rebound in carrier fleets is going to sustain Safran's delivery situation, and we believe a rebound can persist even if we enter a shallow recession, since aviation's depression has been so idiosyncratic.

The H1 should show decent profit growth, pressured somewhat by mix effects, but aircraft interiors should revert into profitability and eliminate that segment's drag on the bottom line. The new LEAP engine is proving to be a success, and cash cow economics can resume once the market gets saturated with these engines.

While Safran remains a superior company, the 13x EV/EBITDA is a private market style multiple that already values the marquis positioning as well as the potent industrial economics that Safran has to offer. 13x is reminiscent of pre-rate hike multiples, and therefore could be considered rich in the current environment. While quality can deserve a premium, we think investors may have to get more creative than a name as well-known as Safran in order to generate returns in the market.

For further details see:

Safran: Phenomenal Delivery Numbers Set Up For Cash Cow Economics