SAFRY - Safran: Why I Outperformed And My 2023 Thesis At A 'Hold'

Summary

- Safran was one of my significant investments in the arms/industrial sector in 2022, with my latest buys in September and my last article there as well.

- The company has massively outperformed the market - almost 6x. It's part of the reason I'm positive for 2022.

- In this article, I give you my stance for Safran for 2023.

Dear readers/followers,

I realize that most of you probably did not follow my investment into Safran (SAFRY). I was a heavy investor in EU defense stocks last year, and most of them were a reason why I outperformed the overall market last year. My last article was out in September of 2022 - and here is the performance since that particular time.

Seeking Alpha Safran (Seeking Alpha)

So, not exactly a bad performance, and I'm looking to potentially take some profits here. In this article, I'm primarily going to talk about the future - not so much about the past. Still, this company is absolutely solid in terms of fundamentals, and I'll be showcasing this and emphasizing the company's quality before moving into the longer-term thesis here.

Remember, there's plenty of macro in this company's valuation from the current Ukraine/Russia-conflict, and this needs to be accounted for.

Let's see how things are looking here.

Updating on Safran for 2023

So, Safran isn't really your typical defense stock - because the sales mix is different. That's the reason I was somewhat overweight compared to businesses like BAE ( BAESY ), Rheinmetall ( RNMBY ), and others. Only Airbus ( EADSY ) is a larger position than Safran for me, though Leonardo ( FINMY ) comes close. Safran is, in fact, a multinational aerospace company and the largest after Airbus, and what it does is aircraft engines, rocket engines, aerospace components, and defense.

{kind=link}

Even though you might not have heard much of Safran, the company has 76,000+ employees, generates over a dozen billion euros in revenue, and its primary operating segments are found in aircraft engines. It owns 50% of the CFM International JV, together with General Electric ( GE ). However, aside from Civil Aircraft, it's in military and space propulsion, engine pods, landing gears, brakes, power electronics, wiring, and Avionics & Optronics in its defense segments.

I don't believe that it is an exaggeration to say that aside from Airbus, and maybe the "new" Rheinmetall, Safran has one of the more appealing sales mixes and futures in the entire industrial/defense segment in Europe. 70% of this company's mix is civil, not straight defense, and like an engine business, it relies on similar trends as Rolls-Royce ( RYCEF ) - except, you know, it hasn't seen material deterioration for over a decade.

Safran remains a great business. We reviewed 1H22 in my last article, and now it's time for 3Q22. The highlights in this term are many, so let's take a look.

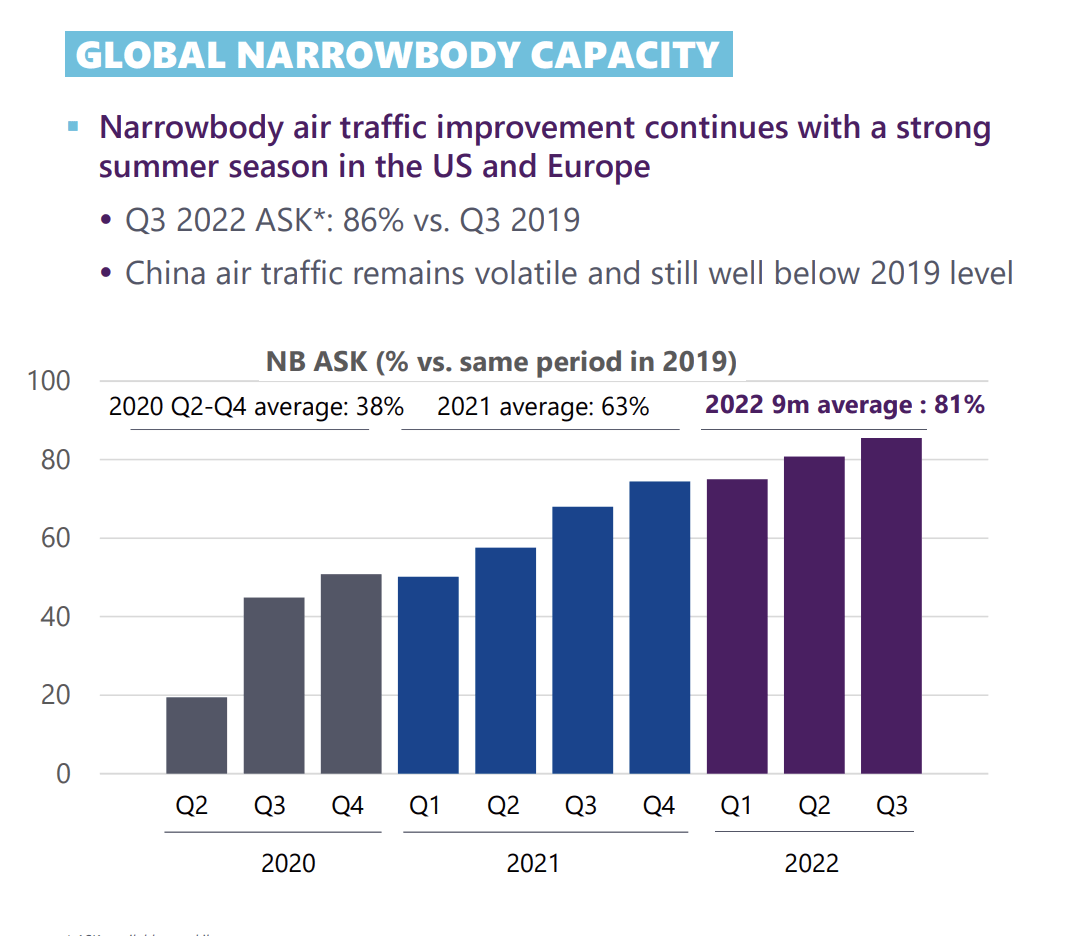

First off, air traffic recovery. The company is pushing narrowbody ASK at 86% of the 2019 level, which is excellent. While China remained volatile due to shutdowns, trends were solid despite SCM and inflation.

{kind=link}

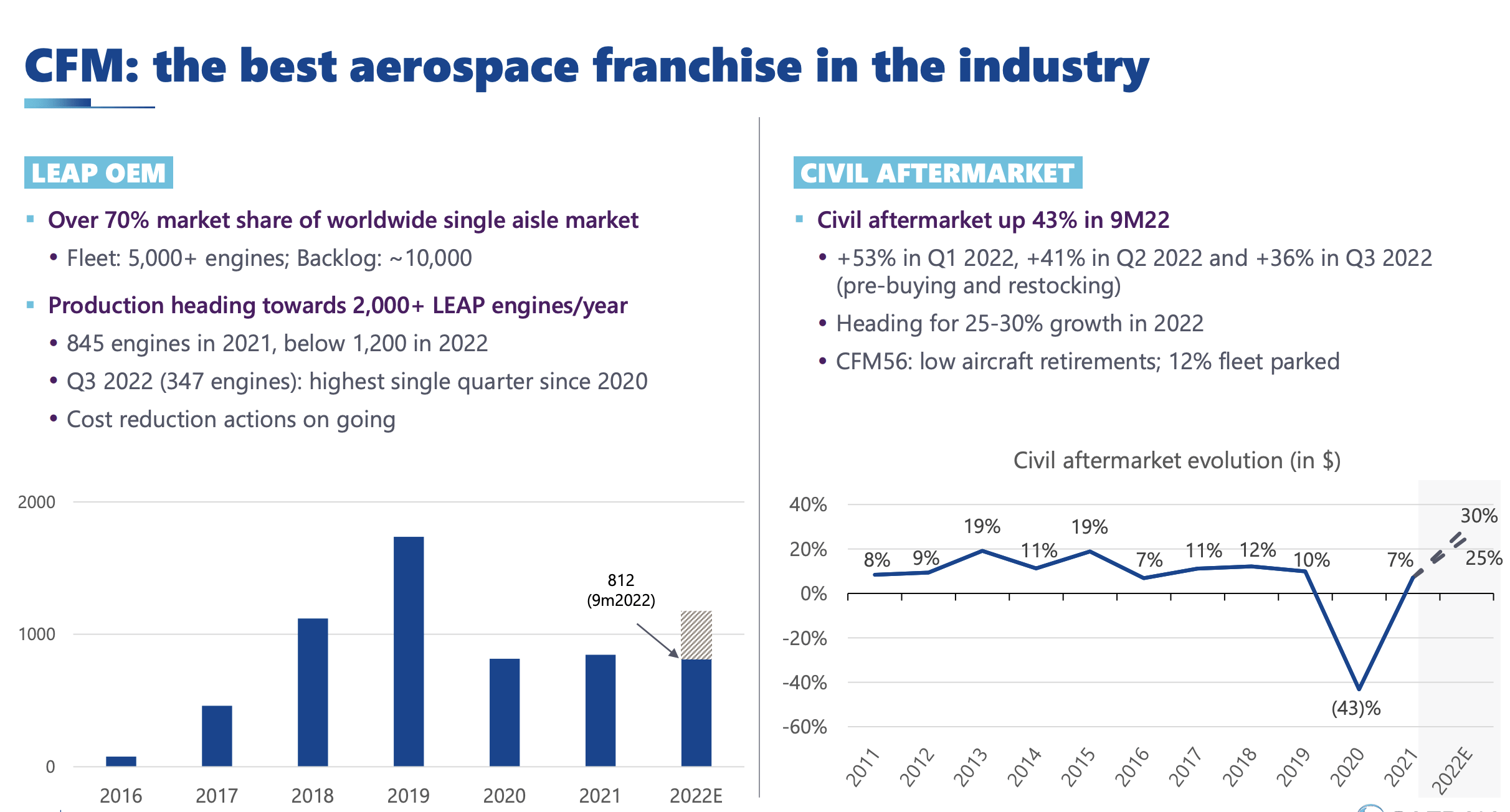

Safran reported 30% revenue growth, of which 18% was organic, not price/mix, and with a high civil aftermarket component. LEAP deliveries were up 54% sequentially.

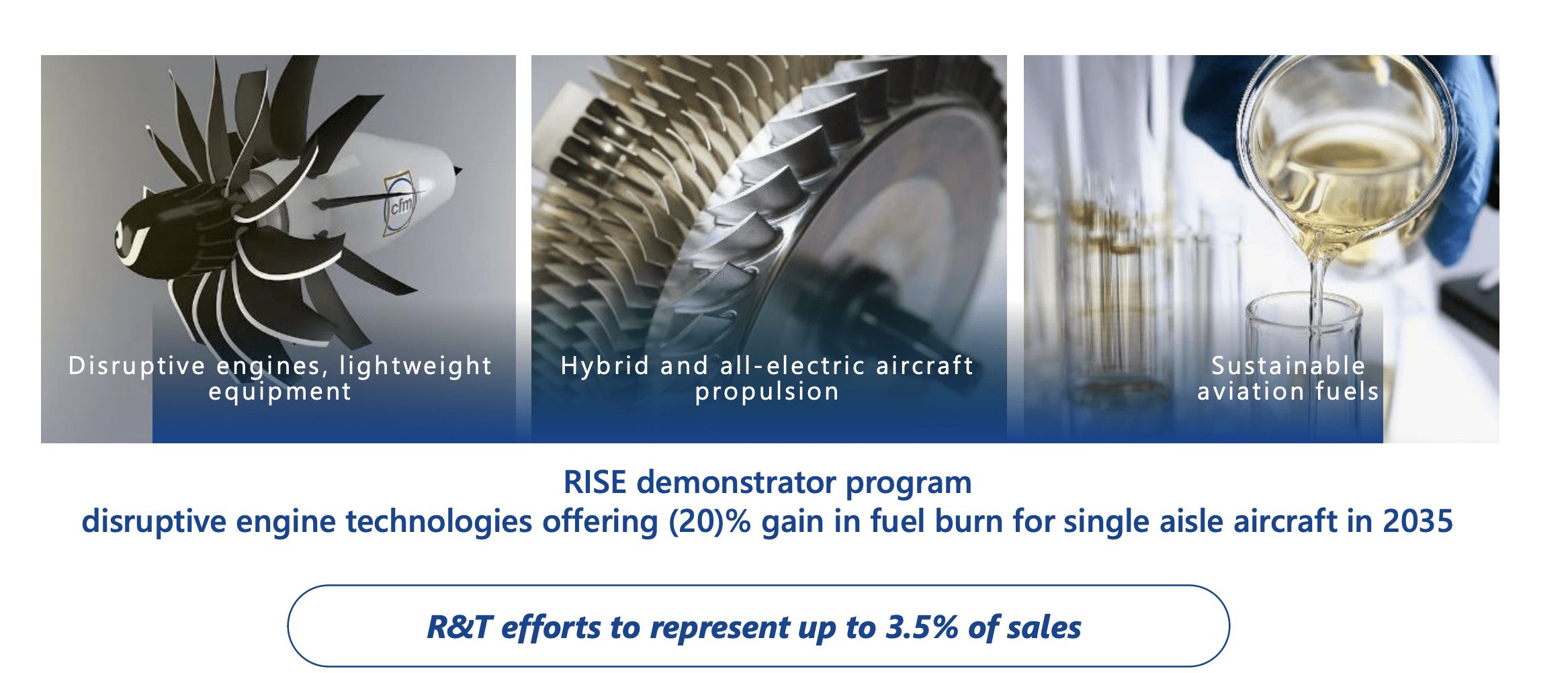

Also, the company has now exclusive negotiations with Thales ( THLLY ) to acquire its electrical system activities, which could result in a bolt-on. The focus should be on traffic improvements overall...

{kind=link}

....and on the following business-specific highlights:

- 364 CFM engines delivered, which is up 121 units on LEAP alone.

- Civil aftermarket up 43% YoY in 9M22.

- Contract renewals for over 900 Arriel engines support a U.S. army contract for its UH-72 Lakota Helicopters.

- Landing Gear for Philippine Airlines.

- 5-year service contract with Cathay Pacific for the thrust reversers of their 51 A330ceo and the nacelles of their 32 A321neo.

- 3-year service contracts for Spring, again for the nacelles.

Remember, Safran also has its aircraft interior business, and this is also up with new contracts from Asia, Europe, and the Middle east for seats, retrofitting, and business class interiors.

So, top line was absolutely solid - and mostly due to demand, not pricing. The company is also actively managing its share liabilities, which is part of the reason why the shares are likely up as much as we're seeing. Safran is going to buy back 9.4M shares to offset/hedge the potential dilution from a set of 2027 convertible bonds in the OCEANEs transaction. This is happening in the next 6-9 months.

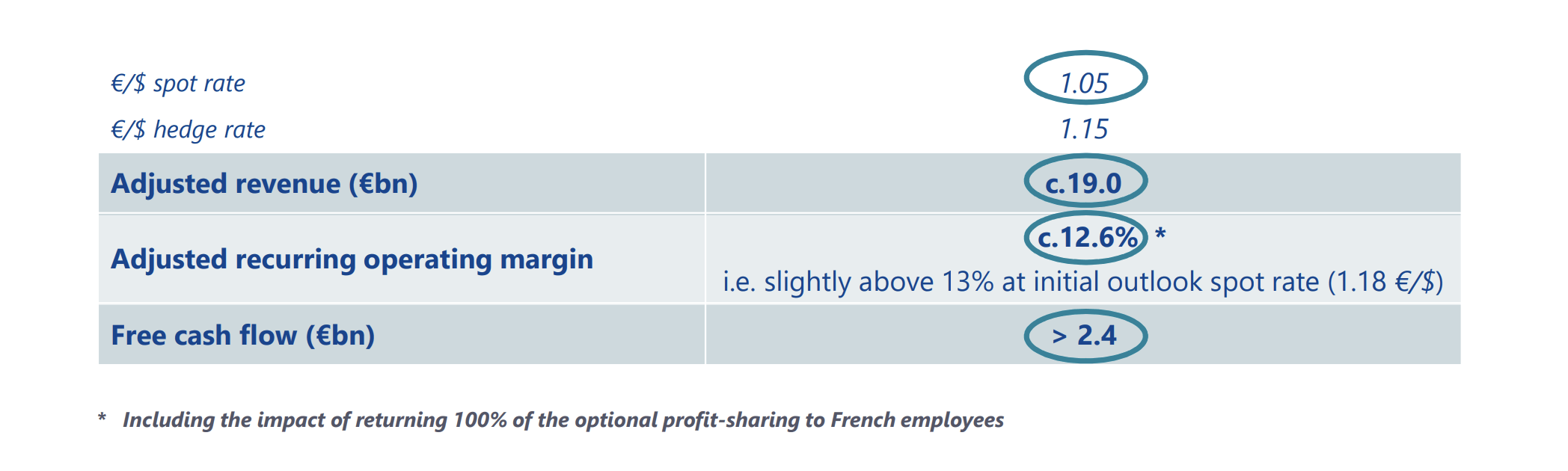

Here is the company's full-year outlook, which we'll see very soon.

{kind=link}

The company is one of the lowest-debt defense/aerospace businesses on the planet that's privately owned/publicly listed. The company is investment-grade rated and offers investors a dividend of between 0.6-1% - so relatively low. But that's really one of the only drawbacks the company has. The company's credit rating was recently bumped up to an A-rating, which is another reason for the excellent development.

Let me also point out that the largest shareholder, by far, in Safran is a government. The French government. If you know my writing, the companies that have government shareholding are typically some that I am positive about - you'll likely be aware of this. Another large shareholder which should lend you trust is BlackRock ( BLK ).

Risks and challenges for Safran? Because not much has changed, one of the largest challenges, and at the same time largest benefits is the Russo-Ukrainian war. While limited tourism will impact the results, the fact is that this conflict drives demand for parts of Safran's products - and the service business the company operates cannot be paused for aircraft owners due to the war either, because Airplanes need to be constantly maintained regardless of the macro.

However, it's important to be aware of the raw material impacts of Russia being closed. France had a pretty close relationship with Russia prior to the war. The aerospace industry relies heavily on titanium and superalloys, which is also why Safran has joined forces with Airbus to acquire Aubert & Duval and secure its supply, and this was finished a quarter ago now.

From a high level, I would also say that there's the question of how the company's contracts are indexed or constructed with regard to inflation and SCM effects - I have as of yet been unable to find details on this, and IR has been no help. Because of this, my PT for Safran is more impaired than most of my other analyst colleagues that follow the company.

I've said before that Safran valuation is complex - and it remains so.

Safran - Changing my thesis due to valuation, and taking some profits.

So, Safran is up 60%. My last PT was €115, the company has been beyond that for some time now. I haven't taken profit in this investment yet, because I've waited to see what the company does and where it goes before 4Q22. But when it started touching levels towards €135/share, I could stay quiet or passive no longer.

Safran's valuation is based on very sound segments, even if they're complicated. It's a substantial order book and a leading market position in the civil market, which is bound to benefit from a long-term linear growth rate in terms of sales revenue and service revenue, coupled with military/defense markets, which are also likely to grow here. The company has "specialized" appeal, with its work in landing gears, brakes, interior designs and development, and other areas. With its relatively recent sale of non-core assets and down payment of debt, the company is entering the full year of 2023 with less debt than at almost any time in its company history.

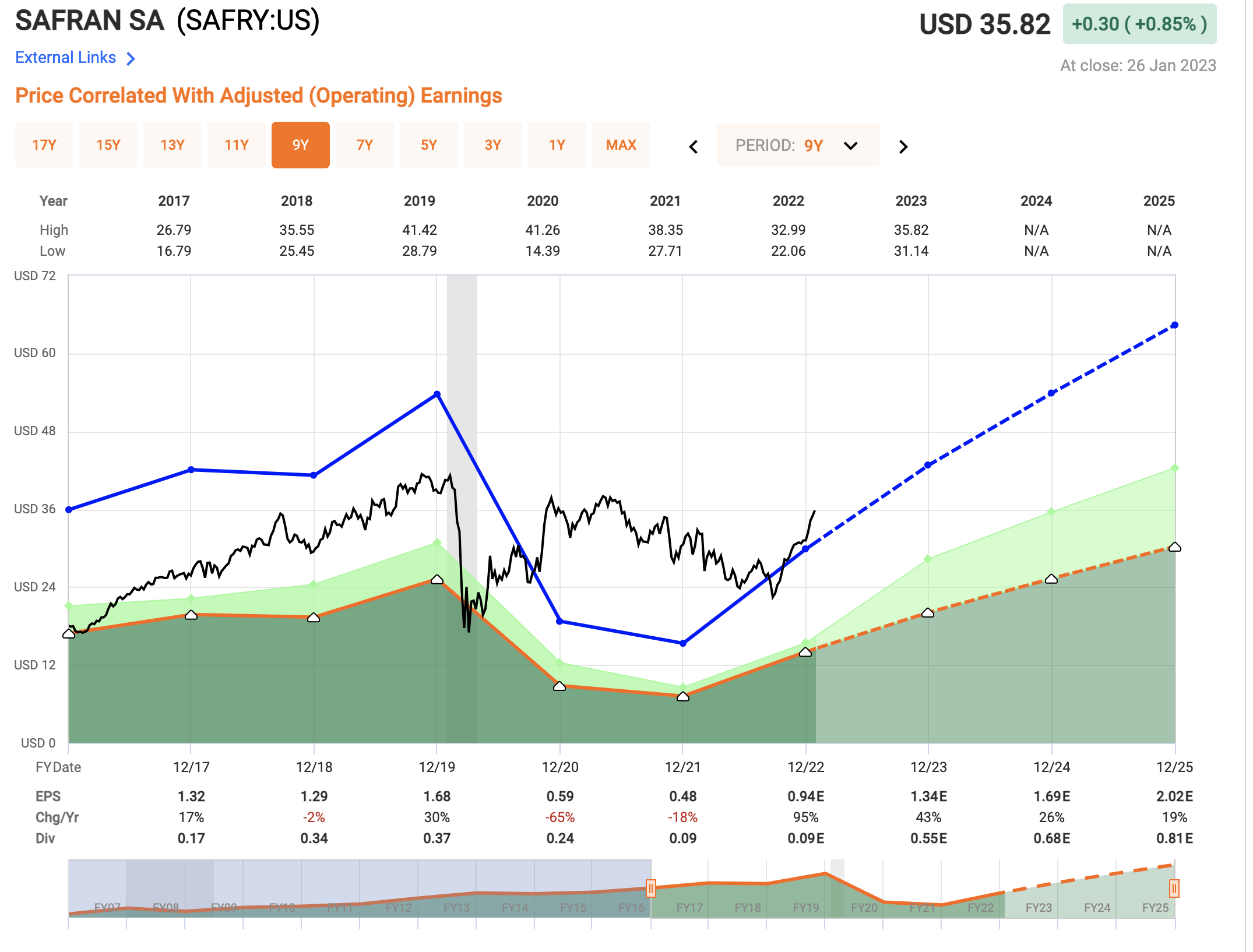

I've been positive on Safran for a long time due to the sheer undervaluation and ignorance of its growth potential. This graph should explain at least some of it.

Safran Valuation (F.A.S.T graphs)

{kind=link}

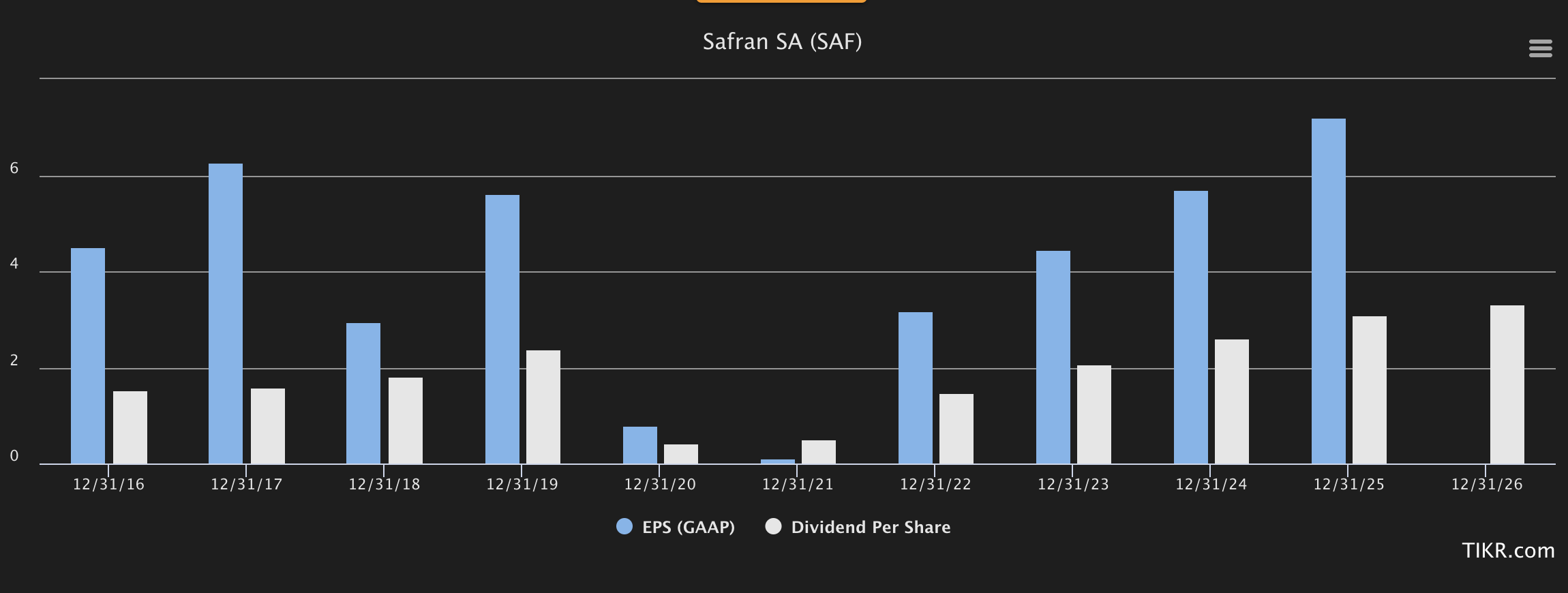

And we can also look at S&P global estimates for the next few fiscal of native GAAP as well as dividend forecasts for Safran here for the ticker SAF, which I invest in.

{kind=link}

Safran is expected to become a dividend stock once again, with 2022E yielding perhaps 1-1.5% at the right valuation. Not much, but decent for its history. You can see though that even in times of massive GAAP, the company hasn't rewarded shareholders here, and even cut it during bad years. Safran should not be thought of as a dividend investor's dream, but a growth-type sort of investment, much like the 60% I've made here. Nothing of that came from dividends paid by the company, all capital appreciation from valuation change.

Analysts following Safran give the company a target range of €118 to €198/share, averaging at around €146. Mind you, these analysts have always been very exuberant for the company, targeting high when the company has troughed. I personally like taking a more conservative approach. My latest target was around €115. In the light of improved revenues and sales, I'm bumping that by €7/share, but no more than that. We're at €122, which means that I would not "BUY" Safran here. I'm changing my stance to "HOLD".

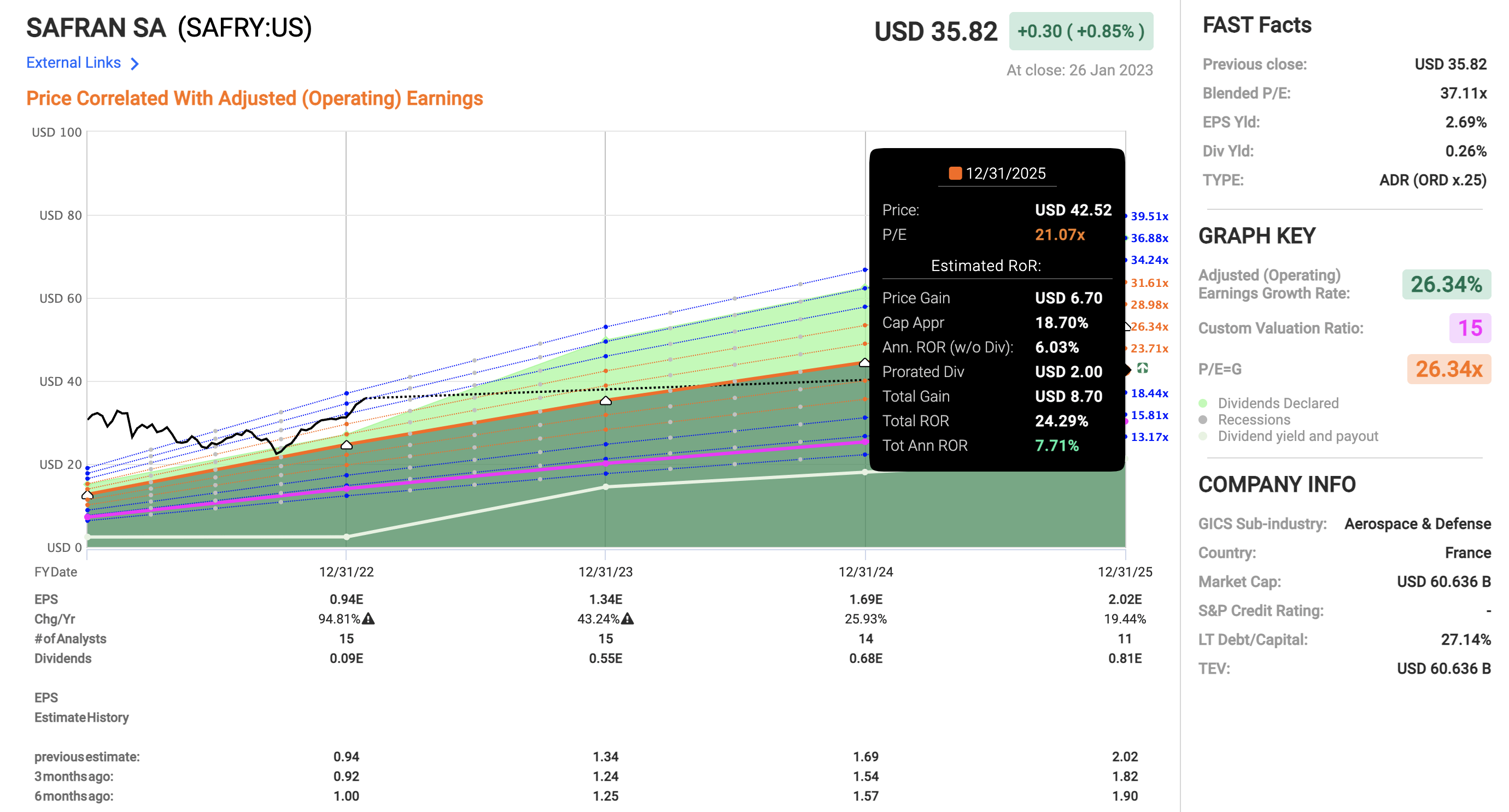

The company might have "room to run" left, looking at the valuation here, but this demands a very high premium of 25-30x. If you forecast the ADR at 32x, you can see a 2023E RoR of 83%, or 23% annually here. But I believe this to be far too positive, all things considered. I forecast Safran at 18-22x P/E, which is what I believe a company growing with this sort of volatility and yield would be worth. This means the company's upside is now barely above 7%, even with the massive growth of 26% per year that we're expecting here.

Safran Upside (F.A.S.T graphs)

{kind=link}

That isn't good enough for me. A common mistake made by investors in European - or any stocks - is that when an underappreciated company likes this start outperforming, people assume it's going to continue doing so. While I believe the company has the potential to go higher - and that's why I keep most of my position in Safran - I also acknowledge the very real possibility of a drawdown that causes the company to trade closer to 15-18x, which by the way company did for almost a decade. I also believe the growth estimates are somewhat too positive here.

I say the company deserves €122/share here, but I'd also say that this is a "HOLD", with the following thesis.

Thesis

- Safran isn't the most immediately profitable or exciting investment opportunity with what's happened in Russia, but it's a solid aerospace company with a market-leading position in appealing segments. The delayed earnings growth will likely materialize in 2023-2025.

- If the company becomes cheap enough - then I'm interested, and at the current price either for the ADR or for the native share. I invest in the native French shares.

- I give the company a PT of €115/share, and it's a "BUY" here.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is no longer cheap, and also doesn't have a significant enough upside for me to go "BUY" here. For that reason, I'm out and at a "HOLD". I'm rotating part of my Safran investment and looking for greener pastures/more value elsewhere.

For further details see:

Safran: Why I Outperformed, And My 2023 Thesis At A 'Hold'