YELL - Saia: Moving To The Sidelines After Recent Run-Up (Rating Downgrade)

2023-08-02 10:29:33 ET

Summary

- SAIA has experienced a significant increase in stock price and is benefiting from the troubles at Yellow Corporation.

- The company's revenue decreased in Q2 but is expected to improve due to additional demand from Yellow Corporation's customers.

- Despite positive revenue growth prospects, the company's valuation is already high, leading to a neutral rating.

Saia (SAIA) has seen a good run-up in its stock price this year and has more than doubled since my previous article earlier this year. In addition to good execution and pricing discipline by most of the LTL carriers, the company also benefitted as customers moved their freight requirements from Yellow Corporation (YELL) to other LTL carriers as Yellow neared bankruptcy. While the company, being one of the leading LTL players, is a natural beneficiary of troubles at Yellow and its revenue and margin outlook looks good as it is poised to gain market share, the valuation has run up significantly and is already pricing in most of the upside. Hence, I am moving to the sidelines and changing my rating to neutral.

Revenue Analysis and Outlook

After seeing an extraordinarily strong couple of years post-COVID, SAIA saw some normalization in demand this year as the economy slowed due to the hawkish stance of the Federal Reserve.

In the second quarter of FY2023, the company's revenue decreased by 6.8% Y/Y to $694.4 mn. This decrease was driven by a tonnage decline of 1.7% Y/Y and a yield decline of 4.8% Y/Y. In terms of yield, the underlying performance was much better with yield excluding fuel surcharge improving 2.7% Y/Y.

Looking forward, while macros are still tough, the recent troubles of Yellow Corporation have resulted in good additional demand for the other LTL players, and SAIA is also one of the beneficiaries of the trend. As Yellow Corporation's customers have started moving their freight requirements to other LTL companies, SAIA is a natural beneficiary.

Management noted that the company's Y/Y volume decline improved as Q2 progressed and volumes turned positive in July with a strong trend seen in the last two weeks of July. According to management , the monthly tonnage till July 28 was up 2.5% Y/Y while shipments were up 5% Y/Y. With Yellow ceasing operation , this trend is going to accelerate over the coming months.

Further, if we look at FY22 tonnage or volume, it sequentially worsened as the year progressed. So, the company should also see benefits from easing volume comps.

SAIA LTL Tonnage Y/Y (Company Data, GS Analytics Research)

Not only are volumes expected to improve, but the company is also poised to see an improvement in yields. One really interesting thing to note is that the company's yield held up pretty well despite the macro slowdown and the company's yield last quarter excluding fuel surcharge was up 2.7% Y/Y. Now, this additional volume coming to the remaining LTL players after Yellow Corporation's troubles should tilt the demand-supply equation in their favor further helping the industry-wide yield. So, I am optimistic about the company's revenue growth prospects.

Margin Analysis and Outlook

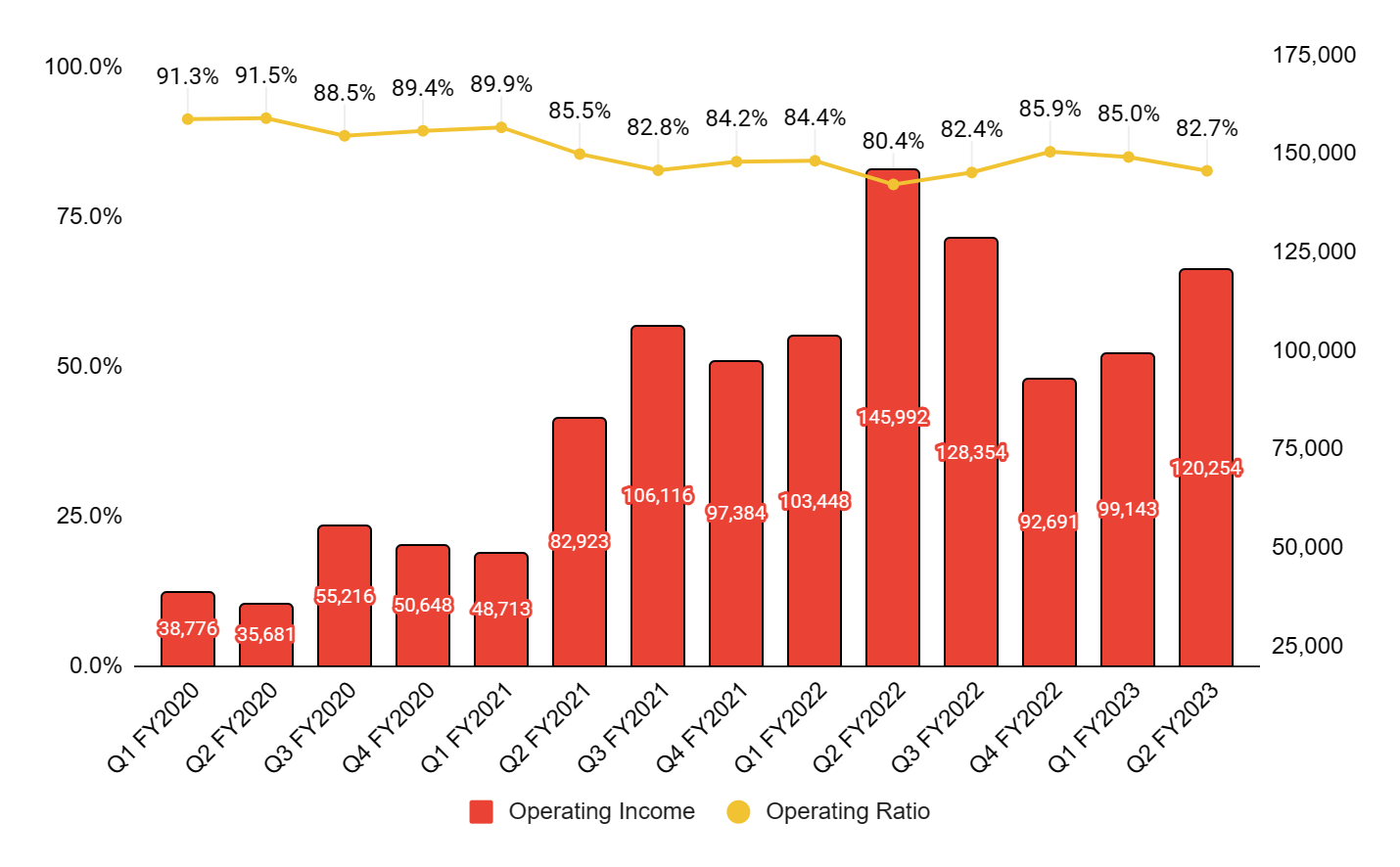

The company's Q2 margins were impacted by volume deleveraging and 5.7% Y/Y cost inflation from increases in salaries, wages, and benefits. As a result, the company's operating margin declined 230 bps Y/Y to 17.3%.

SAIA Operating Income and Operating Ratio (Company Data, GS Analytics Research)

{kind=link}

Given the company's wage increase in July, management has indicated that its operating margin should decelerate 100-150 bps from Q2 to Q3. However, if we look at the current industry dynamics with a potential improvement in both volume and yield for SAIA, I believe the company can do much better and more than offset the impact of wage inflation through operating leverage and yield improvement. So, I am expecting the margin to perform better than expectations and see a potential expansion from the Q2 levels as the year progress.

Valuation and Conclusion

While the company's business is headed in the right direction, one thing which bothers me is its valuation. The company is trading at 33.52x FY23, 28.49x FY24, and 16.34x FY25 consensus EPS estimates. This is much higher than the company's 5-year average forward P/E of 22.95x.

SAIA P/E valuation based on consensus estimates (Seeking Alpha)

The company's earnings estimates have also seen a meaningful revision over the last month after Yellow's troubles, and its FY24 and FY25 EPS consensus EPS estimates have been bumped 7.34% and 8.24% from where they were a month ago.

SAIA Consensus EPS Estimates Revision (Seeking Alpha)

So, the benefit from Yellow's troubles is already getting reflected in the numbers to a good extent. Even if we see another 10% upward revision in estimates, the stock will still be trading higher compared to its historical levels. I like the company's good execution and prospects of market share gain, but the current valuation leaves little margin of safety. Hence, I am moving to the sidelines and changing my rating to neutral.

For further details see:

Saia: Moving To The Sidelines After Recent Run-Up (Rating Downgrade)