CODGF - Saint-Gobain: Pricing India And Subsidized Green Renovation

2023-08-23 14:20:23 ET

Summary

- Compagnie de Saint-Gobain has shown continued organic growth, despite volume pressures, benefiting from trends in green construction and India.

- The H1 report shows growth in pricing and renovation, particularly in markets with government support for green construction.

- The company has seen strong performance in APAC, especially in India, but Northern Europe, particularly Germany, has been a poor performer.

- While the PE is absolutely compelling, there is too much downside for overall markets to be able to put a chip on Saint-Gobain today.

The Compagnie de Saint-Gobain ( CODGF ) ( CODYY ) (or just Gobain for short) has always been a solid, specialised building materials pick that flies somewhat below the radar on European markets. What is surprising is their continued organic growth in the face of volume pressures, and what's been a boon are their exposures to some more robust trends in the global economy such as green construction and India. The lowish PE signals that markets see an end to the growth, and while economic pressures are meant to be mounting now to stop inflation, and indeed companies like Gobain are part of the reason we are seeing inflation considering their pricing measures, the company still looks able to force some growth, although it is likely to continue to slow in coming quarters. While there is sufficient earnings yield to be interesting and the fundamentals look good, the high historical prices make us wary of the technicals, and we'd stay on the sidelines.

H1 Report

The H1 report is interesting. Firstly, we are seeing some deceleration in pricing (10% growth in Q1, 6% in Q2), which is the only reason why Gobain is growing at all. Structural inflation as well as volume declines would otherwise be a margin hit, yet they are just about growing their operating income despite construction being in the line of fire of higher rates in the battle against inflation. Nonetheless, pricing power is still meaningful for Gobain and secular trends continue to materialise for the business even on an organic basis.

The first is that all the shortfall in volumes has been the pressure on new construction, but not renovation. The markets doing best on renovation are those where there are distinct supports from government that are subsidizing green construction, or where there are otherwise systems that incentivise green renovations to reduce the carbon footprint of households, so Southern and Western Europe. The demand from these markets is enough to sustain volumes but also keep the pricing environment constructive ahead of inflation in the cost structure. Net income is flattening out but still rising.

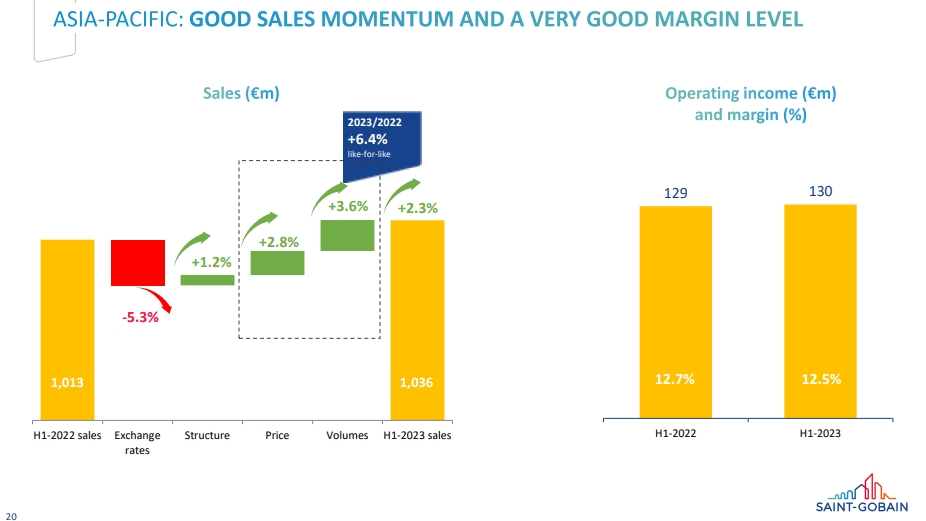

APAC has been a standout performer thanks to substantial exposure to India, which has also grown on an inorganic basis thanks to acquisitions focused on this burgeoning geography. Volumes and pricing are up here, but especially volumes.

{kind=link}

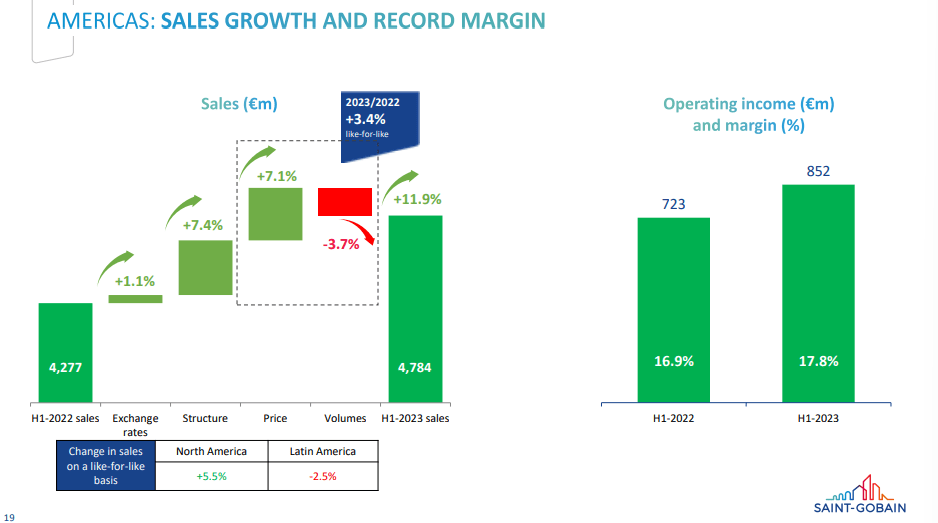

Construction trends in America buck the trend in terms of volumes, where there has been an uptrend in Q2 compared to Q1. Overall volumes are down, but there is some re-acceleration.

{kind=link}

The only poor geography is Northern Europe, particularly Germany, which due to the Ukraine war has been knocked off its perch as the most prosperous European economy. We have a secularly bearish view on Germany, which has been unable to maintain its geopolitical position at all in light of the Ukraine war and will likely remain an underperformer in the region for the foreseeable future.

Bottom Line

The 11x PE or so is actually quite compelling from an earnings yield perspective considering where benchmark rates are. Benchmark rates are going to come up in order to combat this last leg of inflation, which will disappoint markets, but even where terminal rates are likely to be the earnings yield is large enough to create a compelling return profile. There will be some earnings pressure, or at least earnings growth pressure as we continue into the year in all likelihood in geographies excluding India, which we believe is going to be on a sustained uptrend. Considering historical prices and that Gobain remains at a pretty elevated level, the technicals are likely not great considering we don't believe there will be much more momentum from economic data and markets to support the current prices. Our concern with Gobain is just our concern generally with European markets right now, which still have a lot more to do before inflation is sufficiently stamped out as far as the ECB's singular mandate would require. Nonetheless, we continue to keep our eye on Gobain as it's a stealth beneficiary of megatrends in construction and renovation and is a champion among peers.

For further details see:

Saint-Gobain: Pricing, India, And Subsidized Green Renovation