CODGF - Saint-Gobain's Results Are Ahead Of 2021 Plans

Summary

- Gobain is producing good organic growth, even in Q4 which should have been under pressure, thanks to light construction and renovation markets.

- High margin businesses are also the more resilient ones for Gobain, where renovation revenues came in strong and grew margins despite cost pressures.

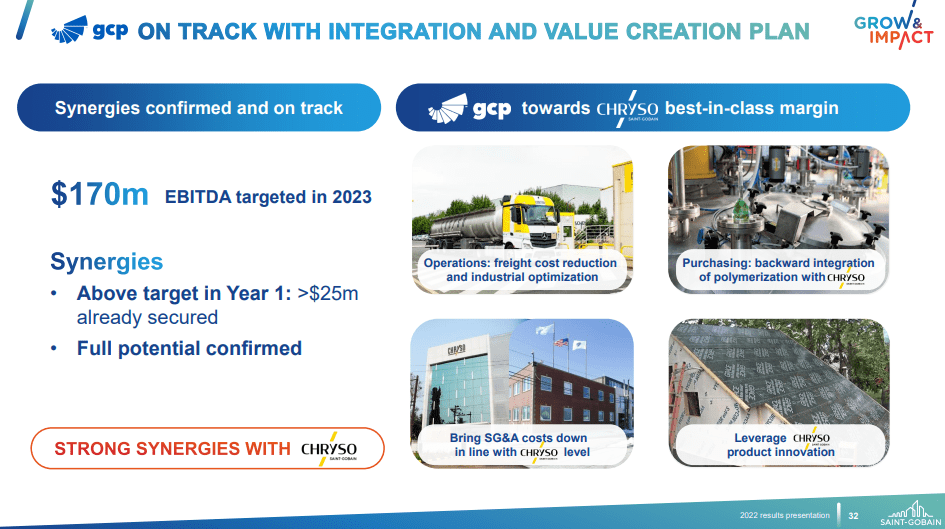

- GCP added about 3% to run-rate sales from GCP inorganically, and the multiple was decent. And the other 3% in run-rate sales were acquired at good multiples too assuming synergies.

- The dividend is being raised substantially, and the company expects to continue growth, although they seem to be signaling that they are ready for deceleration in 2023.

- In the end, they are affected by slowing construction.

Saint-Gobain (CODGF) is a comprehensive buildings supply company, selling fiberglass, cement additives, insulation and waterproofing solutions on top of other construction chemicals and specialised materials solutions. They just reported FY 2022 results and they are good, ahead of their management plan and not particularly decelerating in Q4. Forces within their business make them resilient to a new-build downturn, and they've executed an inorganic growth strategy with a decent degree of skill, although it counts on major synergies. The dividend is growing, and the company is rather cheap relative to US peers, which may be justified considering macro factors, the conclusion of our last analysis . The discount has grown to US peers though, so the company is more interesting. While there is a value angle here, the direction is tough to call at the moment, and we worry about construction trends.

Salient FY 2022 Points

- The organic growth rate was around 13% in sales. Because of the timing of acquisitions, we calculate that the run-rate inorganic growth rate was actually about 6%, added by GCP and a couple of other acquisitions made in late 2022. The multiples for these acquisitions were around 10-12x EV/EBITDA, which is somewhat reasonable in the current market taking into account the necessity of a control premium. However, these multiples include fully realised EBITDA synergies. In the case of GCP which provides half of the inorganic growth, the EBITDA synergy is forecast to almost 3x the run-rate EBITDA of the business from before the acquisition. Similar synergy marks are put with the other companies too. These seem aggressive and we don't love the inorganic growth with Gobain.

Synergies on GCP, EBITDA was $100 million before acquisition (FY 2022 Pres)

{kind=link}

- Synergies aren't getting realised massively yet at all, but margins grew across geographies, and in all cases it was because of growth of lighter construction solutions in the revenue mix. These are higher margin and more exposed to renovation activity which is more resilient. This is a very good thing. Any sort of margin expansion in the current environment is impressive, and is a testament to some degree of pricing power thanks to the value-add solutions but the mix effects had a fair bit to do with it as well.

Highlights (FY 2022 PR)

- Pricing was the only mode of sales growth, as volumes actually declined 1.3% for the FY at the group level. This is not a great sign, and while some of it can be attributed to an excited 2021 comp, it also comes down to the cracks showing in the construction activity levels, which are coming down meaningfully. Permitting rates in the US are falling below pre-COVID levels , and in general there is a slowdown in most housing markets in Europe. No signs of total disaster yet, but the rate cycle deeply affects the economics of developers.

FY Price vs Volume (FY 2022 PR)

- Q4 is showing some deceleration is sales coming down to 9.8%. 6% is coming from inorganic growth so the organic rate is about 4%. This is not a surprise and more or less in line with what we'd expect given the deceleration in housing.

Bottom Line

Declines in construction are fully expected by management, and they expect to still achieve around 6% in average growth across their management plan period. So averaging down is expected. The direction isn't that great for Gobain, but the renovation markets are a backstop both in terms of revenues but also due to mix effects.

For further details see:

Saint-Gobain's Results Are Ahead Of 2021 Plans