SALRF - SalMar: A Lot Riding On The CMD Organic Growth Strategy And Cost-Cutting

2023-12-17 10:30:09 ET

Summary

- SalMar is operationally compensating for the bottom line hit of the new ground rent tax.

- Organic initiatives, cost savings and a Scotland rebound should help results in 2024 grow nicely despite new headwinds.

- Business still benefits from high reinvestment rates so the CMD initiatives should accrete value.

- While the current 25x PE can get driven down quickly, there are still better opportunities in other markets that we will prefer with our capital.

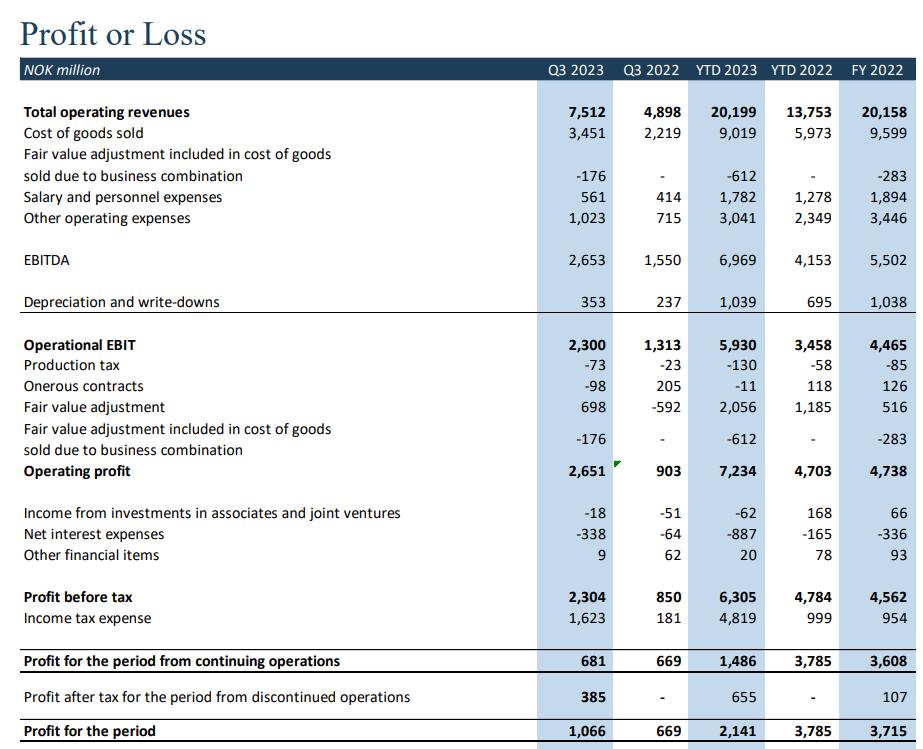

SalMar ( OTCPK:SALRF ) now sees the pretty massive impacts of the new tax regime on their income. However, very strong harvest volumes have actually kept them looking pretty solid on the bottom line YoY. Moreover, there are decent organic growth initiatives in the business that are going to benefit from alright reinvestment rates, and they are doing some cost cutting that should yield further results. The high run-rate multiple seems to reflect these positives, but there are much better companies out there at lower multiples than this.

Earnings and CMD Considerations

Taxes are important to consider.

{kind=link}

There is the new production tax which has more or less doubled unit taxes per tonne. But this is small beans compared to the ground rent tax which has more than doubled the effective tax rate. Read here , we won't repeat ourselves.

The YTD and Q3 results both reflect proper run-rates, since there was a retroactive application that is accounted for in the YTD figures, which the company refers to as the implementation costs .

Run-rate PEs are around 25x. Salmon prices are down YoY , but harvest volumes have come up very substantially in order to create quite substantial scale economics as the operating level and volume based sales growth.

{kind=link}

There are also cost improvements that have kicked in.

By the end of the third quarter, we can report that 75% or NOK635 million of NOK844 million in annual cost savings has already been realized.

CFO of SalMar Ulrik Steinvik

So there's another 200 million NOK to come.

In terms of the CMD , the company is focused on the fact that on current supply chains there is space for organic growth in terms of investing in more smolt space, more pens, and prepping for more harvesting. Volumes could go up as much as 33% according to the CMD.

Verdict

The organic growth should come in pretty profitably, with the needed investments to get more organic volume growth likely to come in at sufficiently high reinvestment rates. We calculate unlevered ROIC to be around 11%, post-tax of course. That's definitely good enough, and reflects excellent ROICs even after the new, massive taxes.

There is also around 200 million NOK more in annual savings to come on the operational side. It's a nice 2.5% lift to EBIT, not totally insignificant.

Ultimately, SalMar has managed to overcome the massive earnings hit that comes from the higher taxes.

Please note that they made a disposal which generated a pretty substantial gain and also saw this quarter as the last period where the discontinued Frøy operations are contributing. You have to use the continuing operations EAT to get to the 25x run-rate PEs.

The organic initiatives are likely to come in over the next couple of years with not too much trouble at a 10% unlevered bottom line return. The Scottish operations are also profit detractors. Conditions are pretty bad right now in that operation due to some mortality events, and the profit detraction is around 5% which is pretty substantial. Turnaround there would be helpful but guidance is still lower in Q4 so one would have to wait for 2024.

There are positives here. SalMar will continue to grow even though the tax situation really is painful for the company. However, it was relatively inevitable as the ROICs of SalMar and other offshore pureplays has always been extremely high, to the point where the government was giving away too much of a cut to a business that is ultimately dependent on government concessions. At least SalMar has these taxes in the rear-view for the Norway dominated mix. Other geographies could follow Norway later.

Post-tax EATs should be on the up secularly without issue. Growth continues. But 25x PE is high, and there are cheaper opportunities in Japan in less cyclical industries.

For further details see:

SalMar: A Lot Riding On The CMD Organic Growth Strategy And Cost-Cutting