SBR - San Juan Basin Royalty Trust: Sell On Natural Gas Prices Plummeting And Production Declining

2023-07-06 08:20:50 ET

Summary

- The San Juan Basin Royalty Trust's distributable income rose to $79 million in 2022, driven by higher natural gas and oil prices, but is expected to decline in 2023 due to lower commodity prices.

- The Trust's production has declined in recent years and their distributions are likely to decrease further due to lower expected natural gas prices in 2023.

- Compared to its peers, the Trust has shown the highest volatility in income and dividend growth rates, leading to a recommendation of a sell rating for its units.

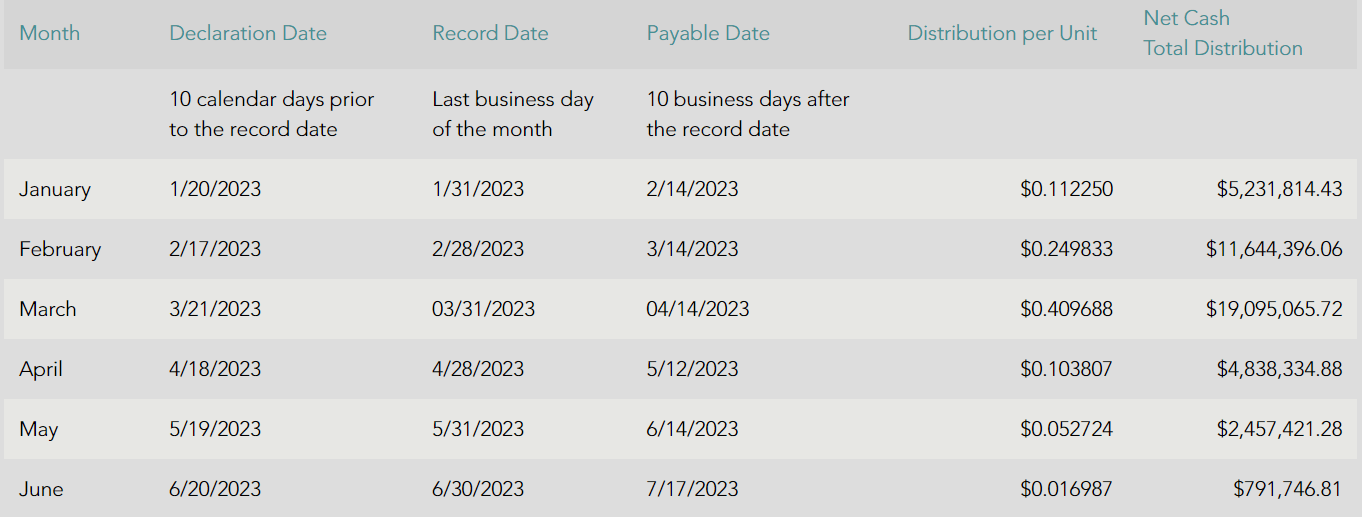

The San Juan Basin Royalty Trust ( SJT ) primarily holds a 75% net overriding royalty interest in oil and gas properties situated in the San Juan Basin of northwestern New Mexico. These properties are operated by Hilcorp, a private oil company. The distributable income for 2022 amounted to approximately $79 million, after deducting administrative expenses of $1.5 million, in 2022, the Trust distributed approximately $77.6 million or $1.664908 per Unit to its Unit Holders. This increase in income can be attributed to the rise in natural gas prices from an average of $3.20 per Mcf in 2021 to $5.54 per Mcf in 2022, as well as the increase in oil prices from an average of $54.72 per Bbl in 2021 to $86.73 per Bbl in 2022. Additionally, the Trust's natural gas production saw a slight increase from 24,209,889 Mcf in 2021 to 24,483,167 Mcf in 2022.However, it is important to note that oil and gas prices experienced a decline in 2023 and they will remain at lower levels versus 2022. Consequently, the Trust's distributions per unit have decreased on average this year (see Figure 1 ).

Figure 1 – SJT’s distributions in 2023

SJT's net cash total distributions

{kind=link}

In 2023 , the Trust has announced its plan to allocate around $4.4 million for capital expenditures. Out of this budget, approximately $3.7 million will be dedicated to 25 well recompletions and workovers. An additional $0.2 million will be set aside for future drilling projects. It is important to mention that natural gas prices are expected to remain lower in 2023 compared to 2022. Consequently, it is worth noting that a small portion of this budget may potentially have a significant impact on monthly distributions specially on small amounts of distributions like the last distribution in June 2023 that was $0.016 per unit.

SJT’s financials and market outlook

At the end of the first quarter of 2023, the beneficial interest of the Royalty was divided into 46,608,796 units. The Trust's distributable income rose from $14.4 million, equivalent to $0.30 per unit at the end of the first quarter of 2022, to $36 million or $0.77 per unit by the end of 1Q 2023. This surge in distributed income can be primarily attributed to elevated gas prices.

Furthermore, following a significant increase in the Trust's cash balance to $6.2 million by the end of 2021, up from $1.3 million during the economic downturn of 2020, their cash generation experienced a decline to $5.5 million by the end of 2022. However, in their most recent report, the Trust announced a cash generation of $20 million. Moreover, their equity level decreased from $5.1 million in 2020 to $3.0 million at the conclusion of 2022.

SJT's income during the first quarter of 2023 significantly increased to $36.4 million compared to $14.9 million in 1Q 2022. Various factors contributed to this surge in oil and natural gas prices during 2022 and early 2023, including the Russia/Ukraine war, which caused uncertainty and shortage in the natural gas supply chain. Additionally, the colder-than-normal winter in California and the southwest region increased the demand for natural gas, resulting in higher prices. However, factors have now been mostly eliminated or reduced. California's winter season has ended, leading to a decline in the demand for natural gas. Furthermore, although the Russia/Ukraine war persists, adjustments have been made globally to address issues within the natural gas supply chain.

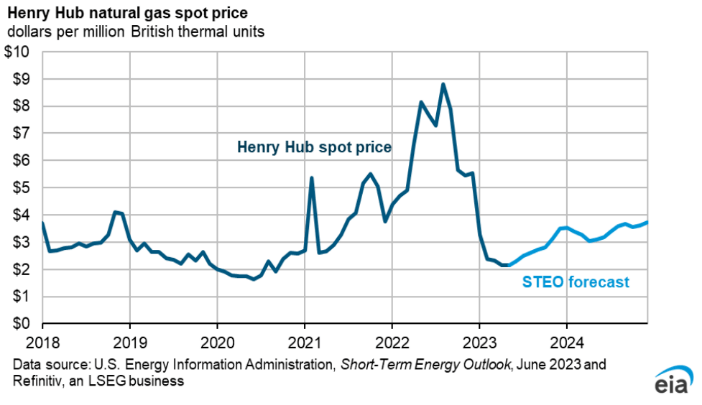

Although the U.S. benchmark Henry Hub natural gas price is projected to increase during the summer and reach $2.6/MMBtu in the third quarter of 2023, it is unlikely to come close to the prices seen in 2022. The average natural gas prices for 2023 are expected to be around $2.66/MMBtu, significantly lower than the average prices of $6.42/MMBtu in 2022. Additionally, it is anticipated that Henry Hub prices will average around $3.4/MMBtu in 2024, representing a 30% increase compared to 2023. Despite the anticipated rise in prices during the summer, ample natural gas inventory levels will prevent them from reaching the levels observed in 2022 (see Figure 2).

Figure 2

{kind=link}

Apart from the impact of natural gas prices, it is of great importance to acknowledge the significant decline in production by the Trust in recent years. In 2018, their natural gas production stood at 32,501,962 Mcf, but it has since plummeted by 24% to reach 24,483,167 Mcf by the end of 2022. Despite Hilcorp's intentions to boost CAPEX for new drilling projects, I am skeptical about its ability to enhance Trust production. Therefore, it might be more prudent for them to allocate their cash towards distributions instead, in my opinion.

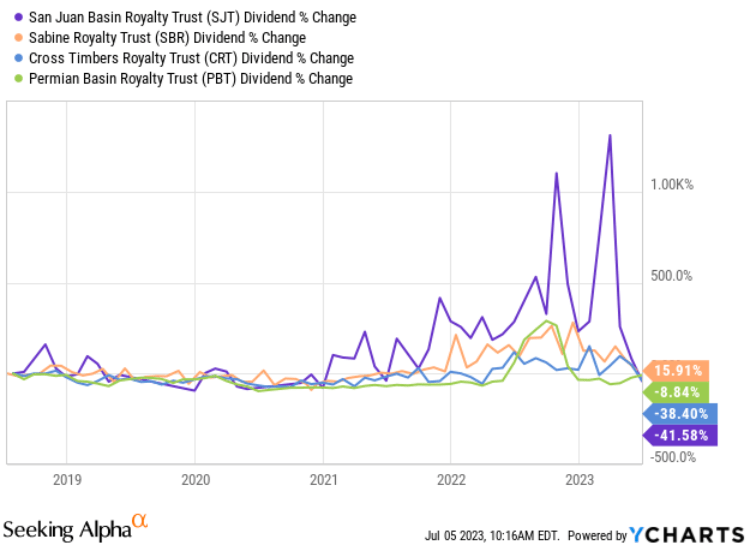

SJT’s performance vs. its peers

In this section, I have compared SJT with some of its peers to delve deeper in the Trust’s performance as compared with its competitors during the last years. The energy industry was one of the best performing industries in 2022 due to geopolitical reasons; as a result, royalty trusts could take advantage of high commodity prices because royalty trusts are a single asset and their cash flows are mostly from oil and gas (and sometimes other commodities). When examining Figure 3, it becomes evident that SJT's dividend growth rate is -41.5%, which is lower than all its peers. Additionally, SJT has experienced the highest fluctuations in its dividend growth rates over the past five years. You may prefer more reliable dividend rates in long-term, don't you? In contrast, Permian Basin Royalty Trust ( PBT ) has demonstrated the lowest volatility during this same period.

Figure 3 -

{kind=link}

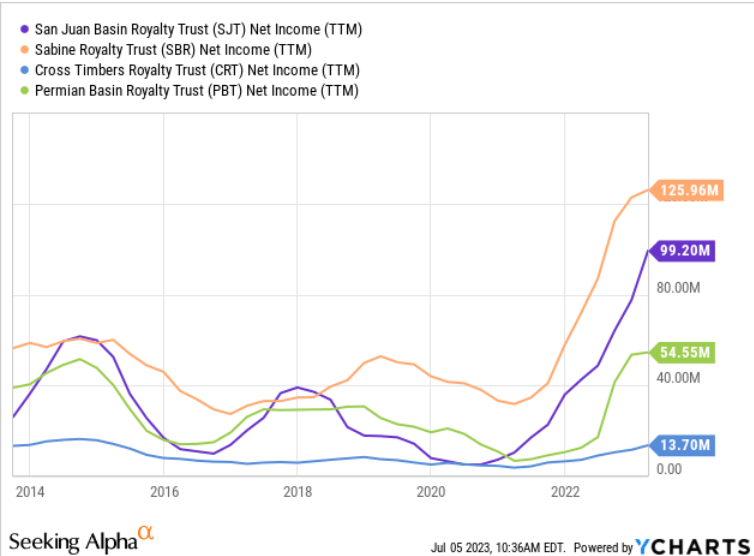

Moreover, SJT is a trust that experiences significant fluctuations in income. While the oil and gas industry has always carried the risk of volatile commodity prices and royal trusts' incomes are tied to these prices, it is important to highlight that SJT has exhibited the highest level of income volatility among its peers over the past decade. This can be seen in Figure 4, where Sabine Royalty Trust ( SBR ) recorded the highest net income of $126 million in TTM among the peers, while displaying much lower volatility compared to SJT.

Figure 4

{kind=link}

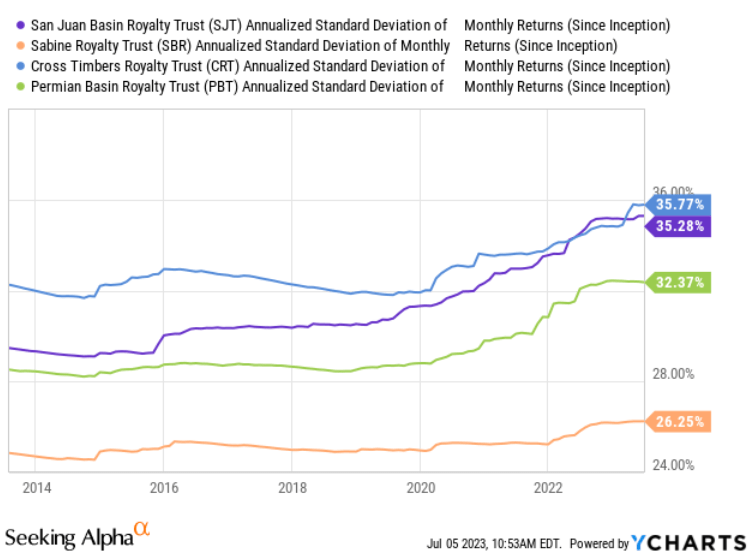

Ultimately, it is interesting to know that SJT has the highest likelihood of falling within its peer groups. Figure 5 illustrates that San Juan Basin and Cross Timbers’ ( CRT ) monthly returns could potentially decrease by more than 35%, whereas Sabin Royalty's return has the lowest potential drop of 26%.

Figure 5

{kind=link}

Ultimately, I have conducted an investigation into SJT's value at risk (VaR) and compared it with its peer group. VaR is a financial metric used to estimate investment risk and indicates the potential loss that could occur within a specific time period. In simpler terms, SJT has a 26.4% VaR, indicating the maximum probability of loss over a month. This is lower than CRT's 28.4%, but significantly higher than Permian Basin's 19.8% and Sabin Royalty's 18.8%. Consequently, this straightforward metric highlights that SJT exhibits greater volatility compared to most of its peers (see Figure 6).

Figure 6 -

YCharts

Conclusion

It is expected that natural gas prices will remain low by the end of 2023, in spite of a slight increase in summer months, due to the high inventory levels compared to 2022. Furthermore, considering the Trust’s plan of allocation of $4.4 million for capital expenditures, it is likely that their distributions will decrease further by year-end. Additionally, when comparing SJT with similar peers, it becomes evident that San Juan Basin Trust has exhibited almost the highest volatility in various performance metrics over the past five to ten years, which makes the Trust less reliable for me. Consequently, I have reached the conclusion that investing in the Trust is not advisable and would recommend a sell rating.

As always, I value your opinions and insights regarding my assessment.

For further details see:

San Juan Basin Royalty Trust: Sell On Natural Gas Prices Plummeting And Production Declining