JNJ - Sana Biotechnology: Finally Rewarding Investors But Not Sufficiently Derisked

2024-01-11 15:25:32 ET

Summary

- Sana Biotechnology, Inc. raised $600m in one of the largest-ever biotech IPOs.

- The company's share price had deteriorated from $25, to <$3, as its in vivo and ex-vivo allogeneic therapies made slow progress or were discarded.

- Sana now has two therapies in Phase 1 studies - targets are primarily oncology indications, although a new study in autoimmune was recently initiated.

- This week, shares have been rising after management spoke about the possibility of targeting diabetes with a new candidate, and promised several data readouts at the JPMorgan conference.

- The upside will be welcome for beleaguered Sana Biotechnology shareholders, although this may be a false dawn. The reality may be that Sana's therapies have not spent enough time in the clinic yet.

Investment Overview - Sana's Desire To Be A Pioneer In Allogeneic Cell Therapy

Sana Biotechnology, Inc. ( SANA ) completed one of the largest biotech IPO's of all time back in February 2021, raising close to $600m via the issuance of ~23.5m shares priced at $25 per share. Prior to that, the company raised ~$700m from a "who's who" of biotech VC's, including Arch Venture Partners, Baillie Gifford, Bezos Expeditions, and Flagship Pioneering.

At the time of its IPO, Sana had no clinical stage assets, but in 2024 the company will oversee four clinical programs, treating seven different diseases, and involving three different therapies. Each therapy is a product of Sana's "hypoimmune" technology platform, which the company presents as a solution to the problems that prevent "autologous" cell therapies treating a wider pool of patients. Consider this statement from the company's Q3 2023 quarterly report / 10Q submission :

Frequently in disease, cells are damaged or missing entirely, and an effective therapy needs to replace the entire cell, an approach referred to as cell therapy or ex vivo cell engineering.

A successful therapeutic requires an ability to manufacture cells at scale that engraft, function, and have the necessary persistence in the body. Of these requirements, long-term persistence related to overcoming immunologic rejection of another person’s cells has been the most challenging, which has led many to focus on autologous, or a patient’s own, cells as the therapeutic source.

However, autologous therapies require a complex process of harvesting cells from the patients, manipulating them outside the body, and returning them to the patient. Products using this approach have had to manage significant challenges such as scalability, product variability, product quality, cost, patient accessibility, and limits on number of cell types that are amenable to this approach

This is undoubtedly true - several autologous cell therapies have been approved - Gilead Sciences' ( GILD ) Yescarta and Tecartus earned >$1bn of revenues between them in 2022, while Bristol-Myers Squibb's ( BMY ) Abecma and Breyanzi earned >$500m, and Legend Biotech ( LEGN ) / Johnson & Johnson's ( JNJ ) Carvykti earned $152m in Q3 2023 alone.

All of these therapies are approved to treat types of hematological cancer and although they are performing reasonably well in the market place, the market continues to harbor doubts about the long-term safety and durability profile of these types of therapy, their cost effectiveness, the risk / reward profile, and their scalability, given the tough treatment regime and reliance on using a patient's own cells, and lack of long-term data.

Sana's solution to this problem is discussed as follows in its latest 10Q submission :

Rather than using autologous cells to overcome immune rejection, we have invested in creating hypoimmune-modified cells that can “hide” from the patient’s immune system.

We are striving to make therapies that use pluripotent stem cells with our hypoimmune genetic modifications as the starting material, which we then differentiate into a specific cell type, such as a pancreatic islet cell, before treating the patient.

Additionally, there are cell types for which effective differentiation protocols from a stem cell have not yet been developed, such as T cells. For these cell types, instead of starting from a pluripotent stem cell, we can use allogeneic, fully-differentiated cells sourced from a donor as the starting material to which we then apply our hypoimmune genetic modifications.

There are many advantages to the use of non-autologous cells - cell condition, availability, speed, convenience, and cost for example, but also a major drawback - how to ensure a patient's immune system does not reject the new cells, leading to potential deadly complications for the patients, such as graft versus host disease ("GvHD"), cytokine release syndrome ("CRS"), or neurotoxicity ("NTX")?

Sana's Stock Soaring After Torrid Few Years

While Sana's ambition may be a noble one, and one that has attracted plenty of funding - allowing the company to record net losses of $(285m), $(356m), $(270m) in the years 2020, 2021, and 2022, and $(195m) across the first nine months of 2023, with $205m invested in R&D - a lack of tangible progress has seen the Seattle-based biotech's share price fall <$3, most recently in November last year - a loss of nearly 90%.

Nevertheless, Sana stock has been soaring over the past couple of days, reaching a high of >$7 by close of business yesterday, although the current traded price is closer to $6 per share, giving the company a market cap valuation of ~$1.25bn.

First of all, the company was able to announce on January 5th that the Food and Drug Agency ("FDA") had cleared its new drug application for candidate SC262 to initiate a clinical study in the treatment of relapsed or refractory B-cell malignancies, initially in patients who have received prior CD19-directed CAR T therapy. In a press release the company discusses SC262 as follows:

Engineered CAR T cell therapies for B-cell malignancies use binders to target proteins expressed on the surface of B cells. One such protein, CD19, has been the target of all approved autologous CAR T therapies for B-cell lymphoma and B-cell acute lymphoblastic leukemia to date. Unfortunately, incomplete responses or relapses occur in approximately 60% of CD19 CAR T-treated patients.

CD22, which is also a B-cell surface protein, has emerged as an alternative to address failure to achieve durable complete responses with CD19-directed CAR T therapy. SC262 expresses the same CAR, including the same CD22 binder, used in CD22-directed CAR T therapies tested in multiple academic clinical trials. To date, these trials have shown durable complete responses in a substantial number of patients in the relapse setting following treatment with a CD19-directed CAR T therapy.

Sana's lead drug, SC291, is in fact directed against CD19, and it is currently the subject of two different Phase 1 clinical studies, the first, ARDENT, involving the indications of Non-Hodgkin's Lymphoma ("NHL"), and Chronic Lymphocytic Leukemia ("CLL"), and the second, GLEAM, the autoimmune conditions lupus nephritis, extrarenal systemic lupus erythematosus (" SLE"), and AAV.

The fact that Sana is looking at autoimmune conditions as well as oncological ones will likely have pleased the market, as the patient populations are generally larger than in oncology. For example, Sana speculates that the Lupus market extends to >230k patients, and SLE to >200k patients. The Phase 1 GLEAM study has only recently been initiated, but Sana has promised data from the study in 2024 - giving investors hope that positive results will increase the market's valuation of the company.

Back to Sana's newest clinical candidate, SC262. The company's first study will be in b-cell malignancies, in patients who have failed a prior CD19 therapy, which will represent a patient population of ~12k by 2027, management estimates. The correlation between CD22 and its efficacy in treating CD19 failures has already been established in prior studies, narrowing the development risks marginally.

Another major reason for the run up in Sana stock this week is a response to a presentation given by management this week, at this year's JPMorgan ( JPM ) Healthcare Conference - a flagship event in the biotech and Pharma calendar - about the potential of its new candidate to target not only autoimmune conditions, but also, potentially, Type 1 diabetes.

Sana Touts Potential Of New Drug Candidate In Diabetes

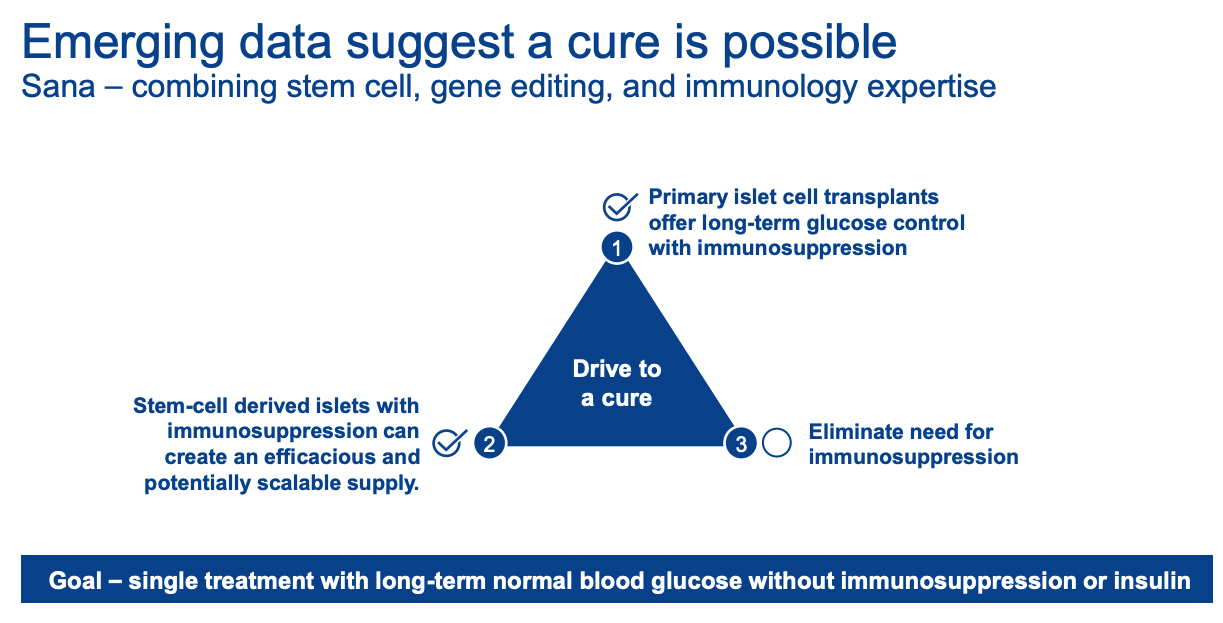

Sana estimates that Type 1 diabetes is an ~8m patient market, and although there are a variety of available therapies for the condition, none offer the type of permanent cure that Sana believes it can develop over time in this field, as shown below, in a slide from Sana's latest investor presentation .

{kind=link}

Sana has been able to show the "survival and function of allogeneic hypoimmune pancreatic islet cells in a diabetic non-human primate for 6 months, without immunosuppression," in a preclinical study.

Clearly, this represents only the beginning of a long development journey which will now move into the clinic, but the tantalizing prospect of a "one and done" permanent cure for diabetes clearly has the market excited.

Sana Biotechnology - The Buy, Sell and Hold Cases Considered

Sana is a biotech that went public via a mega-money IPO, and one which has made some bold promises about what it may be able to achieve in the field of cell therapy with a solution that is allogeneic, not autologous. The main challenge here is overcoming the immunosuppression problem, i.e., making sure that the cells that are custom-engineered for patients using Sana's hypoimmune technology are not rejected by the patient's immune system.

Developing an approvable and marketable allogeneic cell therapy is a problem that no other company has come close to solving yet, although plenty are trying, including Adicet Bio ( ACET ), Adaptimmune ( ADAP ), Allogene ( ALLO ), AlloVir ( ALVR ), Atara Biotherapeutics ( ATRA ), BioCardia ( BCDA ), Beam Therapeutics ( BEAM ), Caribou Biosciences ( CRBU ), CRISPR Therapeutics ( CRSP ), Fate Therapeutics ( FATE ), Gracell Biotechnologies ( GRCL ), Nkarta ( NKTX ), Poseida Therapeutics ( PSTX ), and other besides.

Incredibly, all of these companies' share prices are down >65% over a 5-year period (or since listing), which speaks to the fears the market clearly has around whether the approach can succeed, or whether artificially introducing engineered foreign cells into a patients' body is an approach that is destined to fail.

With only 2 candidates in clinical studies - the first in a Phase 1 study in NHL and CLL, and a Phase 1, which has only just begun, in autoimmune, and the second that will target NHL (CD19 failures), in many ways it is hard to justify Sana's present valuation in excess of $1.3bn, although conversely, shortly after its IPO Sana was worth <4x as much, purely because at that time, investors and the market were confident the company had winning technology.

That has not proven the case, and Sana has had to pull out some of its programs, such as its in-vivo CAR T therapy, abandoned last year as the company sought to make staff cuts in order to control expenses better. The in-vivo program would have been responsible for a substantial chunk of the company's post-IPO valuation.

On the plus side, this year Sana is promising data readouts from both SC291 and SC262 in oncology, and from SC291 in autoimmune. If any of these sets are positive, it may give the share price fresh upside impetus. Further down the line, Sana will hope to move its Type 1 diabetes candidate into clinical studies, and if it does that in the next 12 months, there is another potentially value-enhancing catalyst occurring in 2024 for investor to look forward to.

I think the key factor dictating whether Sana technology is a "buy," "sell," or "hold" after recent events, and at current price, remains the technology itself, and whether data due this year will provide any solid "proof of concept."

Management has been banging the drum for its hypoimmune technology, and opening it up to entire new fields of research - and markets - in the form of autoimmune disease and Type 1 diabetes, although a cynic might suggest that its attention is being drawn to other markets due to a lack of progress in oncology.

In fairness, in the ARDENT study, SC291 generated a partial response in 3 of 4 evaluable patients, with 2 ongoing complete responses, which is encouraging, although as ever with cell therapies, it is the longer term data that provides the most validation, plus the safety profile. There is apparently no prospect of Sana securing an approval in any indication for 2-3 years, at least.

Although Sana has not yet run into any major safety issues, the delicate nature of cell therapy and risk to patients means clinical holds imposed by the FDA on studies in the U.S., and by authorities overseas, are common and can delay development by years.

To summarize my take on Sana, it seems clear that the company means business in 2024. Management will be aware of the heavy spending on R&D across the past few years, and also of its dwindling cash reserves , which stood at $269m as of Q3, suggesting the funding runway could be exhausted in 2025 at current rate of burn.

As such, Sana Biotechnology, Inc. will be under pressure this year to deliver some signs of tangible progress towards the goal of delivering a commercial, allogeneic cell therapy - perhaps the world's first. Management has begun the year by suggesting its pre-clinical data shows it may be able to successfully treat diabetes, and by talking up its move into autoimmune. These are worthy accomplishments, but now the company needs to deliver the clinical data to support its claims, and that starts with oncology.

Last year, I gave "buy" recommendations to several cell therapy companies I believed were on the verge of a significant breakthrough, some in the allogeneic space, some testing autoimmune therapies, but ultimately these companies share prices performed poorly due to a lack of conclusive data and genuinely compelling progress.

Do I feel differently about Sana Biotechnology in 2024? Personally, I believe Sana has not yet collected a sufficient amount of clinical data for a full judgement to be made, which is why I will give the company a "hold" recommendation. I actually believe that like 2023, 2024 may not be cell therapy's year. I am certainly not giving up hope it can eventually succeed, but I am not confident it will provide investors with much in the way of breakthrough progress this year - perhaps 2025 is a more realistic target.

Sana has definite potential, but the upsurge on a potential route to diabetes treatment may be overblown, and progress in the "bread and butter" oncology indications may be the best indicator of what Sana is, or isn't capable of as a company going forward at the present time.

If I were an investor I'd be prepared to hold my Sana Biotechnology, Inc. shares and wait for more data. However, at the current price, I would not want to make a buy so early in the clinical study journey, and I would regard this as perhaps one the higher share price peaks we are likely to see in 2024.

For further details see:

Sana Biotechnology: Finally Rewarding Investors, But Not Sufficiently Derisked